It was indeed a great pleasure contributing in co-authorship Dr. Johannes Winter & Jochen Werne to the Henry Stewart Publications and we are pleased to not only the present the article, but also give everyone the opportunity to download and read the full chapter here:

The Cambridge Dictionary defines the point of no return as the stage at which it is no longer possible to stop what you are doing, and when its effects cannot now be avoided or prevented. Exponential advances in technology have led to a global race for dominance in politically, militarily and economically strategic technologies such as 5G, artificial intelligence (AI) and digital platforms.

A reversal of this status quo is hardly conceivable. Based on this assumption, this paper looks to the future, adding the lessons of recent years — the years when the point of no return was passed. In addition, the paper uses practical examples from different industries to show how digital transformation can be successfully undergone and provides six key questions that every company should ask itself in the digital age.

The article includes key learnings and/or best practise examples from e.g. acatech – Deutsche Akademie der Technikwissenschaften Plattform Lernende Systeme – Germany’s AI Platform Prosegur Tesla Waymo Google Amazon relayr Ada Health Fiege Logistik Westphalia DataLab Satya Nadella Microsoft TikTok Facebook

About this whitepaper This paper was prepared by the Work/Qualification, Human-Machine Interaction working group of the Learning Systems Platform. As one of a total of seven working groups, it examines the potentials and challenges arising from the use of artificial intelligence in the world of work and life. The focus is on questions of transformation and the development of humane working conditions. In addition, it focuses on the requirements and options for qualification and lifelong learning as well as starting points for the design of human-machine interaction and the division of labour between man and technology.

Original published in German. Translation made by Deepl.com

Authors: Prof. Dr.-Ing. Sascha Stowasser, Institut für angewandte Arbeitswissenschaft (ifaa) (Projektleitung) Oliver Suchy, Deutscher Gewerkschaftsbund (DGB) (Projektleitung) Dr. Norbert Huchler, Institut für Sozialwissenschaftliche Forschung e. V. (ISF-München) Dr. Nadine Müller, Vereinte Dienstleistungsgewerkschaft (ver.di) Dr.-Ing. Matthias Peissner, Fraunhofer-Institut für Arbeitswirtschaft und Organisation (IAO) Andrea Stich, Infineon Technologies AG Dr. Hans-Jörg Vögel, BMW Group Jochen Werne, Prosegur Cash Services Germany GmbH Authors with guest status: Timo Henkelmann, Elabo GmbH Dr.-Ing. habil. Dipl.-Tech. Math. Thorsten Schindler, ABB AG Corporate Research Center Germany Maike Scholz, Deutsche Telekom AG Coordination: Sebastian Terstegen, Institut für angewandte Arbeitswissenschaft (ifaa) / Dr. Andreas Heindl, Geschäftsstelle der Plattform Lernende Systeme / Alexander Mihatsch, Geschäftsstelle der Plattform Lernende Systeme

The introduction of artificial intelligence (AI) in companies offers opportunities and potential both for employees, for example in the form of relief through AI systems, and for companies, for example in the form of improvements in work processes or the implementation of new business models. At the same time, the challenges in the use of AI systems must – and can – be addressed and possible negative accompanying implications dealt with. The change in the companies can only be mastered together. All in all, it is a matter of shaping a new relationship between people and technology, in which people and AI systems work together productively and the respective strengths are emphasised. Change management is a decisive factor for the successful introduction of AI systems as well as the human-centred design of AI deployment in companies. Good change management promotes the acceptance of AI systems among employees, so that the potential of new technologies can be used jointly for all those involved, further innovation steps can be facilitated and both employees and their representatives can be made the shapers of technological change.

The participation of employees and their representatives makes a significant contribution to the best possible design of AI systems and the interface between man and machine – especially in terms of efficient, productive work organisation that promotes health and learning. Early and process-oriented participation of employees and co-determination representatives is therefore an important component for the human-centred design and acceptance of AI systems in companies.

The introduction of artificial intelligence has some special features which also have an impact on change management as well as on the participation of employees including the processes of co-determination in the company. The authors of the working group Work/Qualification, Human-Machine-Interaction pursue with this white paper the goal to sensitize for the requirements of change management in Artificial Intelligence and to give orientation for the practical implementation of the introduction of AI systems in the different phases of the change process:

Phase 1 – Objectives and impact assessment: In the change processes for the introduction of AI systems, the objective and purpose of the applications should be defined from the outset with the employees and their representatives and information on the functioning of the AI system should be provided. On this basis, the potential of the AI systems and the possible consequences for the company, the organisation and the employees can then be assessed. A decisive factor for the success of a change process is the involvement of the employees and the mobilisation for the use of new technologies (chapter 2.1).

Phase 2 – Planning and design: In a second step, the design of the AI systems themselves is the main focus. This is primarily concerned with the design of the interface between man and AI system along criteria for the humane and productive implementation of man-machine interaction in the working environment. Of particular importance here are questions of transparency and explainability, of the processing and use of data and of analysis possibilities by AI systems (including employee analysis) as well as the creation of stress profiles and the consideration of employment development (Chapter 2.2).

Phase 3 – Preparation and implementation: The AI systems must also be integrated in a suitable way into existing or new work processes and possibly changed organisational structures. This means preparing employees for new tasks at an early stage and initiating the necessary qualification measures. It is also important to design new task and activity profiles for employees and to adapt the work organisation to a changed relationship between man and machine. A helpful instrument in the introduction of AI systems are pilot projects and expert phases in which experience can be gathered before a comprehensive introduction and possible need for adaptation with regard to AI systems, qualification requirements or work organisation can be identified (Chapter 2.3).

Phase 4 – Evaluation and adaptation: After the introduction of the AI systems, a continuous review and evaluation of the AI deployment should take place in order to ensure possible adaptations with regard to the design of the applications, the organisation of work or the further qualification of the employees. In addition, the regular evaluation of AI deployment can make use of the experience of the employees and initiate further innovation processes – both with regard to the further improvement of (work) processes and with regard to new products and business models – together with the employees as designers of change (Chapter 2.4).

These practice-oriented requirements are aimed at all stakeholders involved in change processes and are intended to provide orientation for the successful introduction of AI systems in companies. In addition, these requirements should also inspire the further development of existing regulations – for example in legislation, social partnership or standardisation – and thus enable an employment-oriented, flexible, self-determined and autonomous work with AI systems and promote the acceptance of AI systems.

Bei sorgfältiger Betrachtung unserer Vergangenheit stoßen wir auf eine faszinierend und teilweise schizophren anmutende Menschheitsgeschichte von partiellem Wahnsinn und absoluter Brillanz – nicht nur, wenn es um den Einsatz neuer Technologien geht. Werfen wir einen Blick in einige dieser Geschichten.

1961 HAVANNA, KUBA: Die Welt steht am Rande eines nuklearen Holocaust. Eine Realität entstanden durch die Auswirkungen des kalten Kriegs, politischer Doktrinen, harter Grenzen und nicht zuletzt technologischen Fortschritts. Nur Diplomatie und der reine Instinkt für das Wesen der menschlichen Existenz auf beiden Seiten verhinderten das Schlimmste.

Eine Geschichte, die die prekäre Lage der Welt zu jener Zeit besonders gut widerspiegelt findet sich in dem indirekten Angebot Fidel Castro an die Sowjetunion, „das Problem“ zu lösen und die kommunistische Revolution durch den Abschuss von Atomraketen von kubanischem Boden, zum Sieg zu tragen. Sein Kampfgefährte Che Guevara ging sogar noch einen Schritt weiter, indem er sagte: „Wir sagen, dass wir den Weg der Befreiung beschreiten müssen, auch wenn er Millionen von Atomkriegsopfern kosten kann. Im Kampf auf Leben und Tod zwischen zwei Systemen können wir an nichts anderes denken als an den endgültigen Sieg des Sozialismus oder seinen Untergang als Folge des nuklearen Sieges der imperialistischen Aggression.” 1962 antwortete der ehemalige Erste Sekretär der Kommunistischen Partei der Sowjetunion, Nikita Chruschtschow, in einem Brief an Fidel Castro, dass er mit der Idee nicht einverstanden sei, weil sie unweigerlich zu einem thermonuklearen Krieg führen würde und dass es doch noch eine Welt bräuchte, in die die Revolution getragen werden könnte.

1961 NEW YORK, USA: Im selben Jahr ratifizieren 12 Nationen einen Vertrag zur gemeinsamen Verwaltung eines ganzen Kontinents. Ein Kontinent, der größer ist als die Vereinigten Staaten. Ein Kontinent, der 90% der Süßwasserreserven der Welt beheimatet und für das Klima unseres Planeten von außerordentlicher Bedeutung ist: die Antarktis. Es ist das Jahr, in dem einer der ermutigendsten Verträge der Menschheit unterzeichnet wurde – der Antarktis-Vertrag.

OPEN-SOURCE-KONZEPT: Der Vertrag – beinhaltet mehrere Kapitel zur ausschliesslich friedlichen und wissenschaftlichen Nutzung der Antarktis. Damit einhergehend regelt der Vertrag auch die gemeinschaftliche Nutzung aller Forschungsergebnisse und Daten. Ein Konzept, das für die damalige Zeit revolutionär erschien und das für die Findung von Lösungen für die großen Herausforderungen unserer Zeit – wie Klimawandel oder die effektive Bekämpfung einer Pandemie – von entscheidender Bedeutung sind.

2020 PLANET ERDE. In der Geschichte haben wir oft die positiven wie auch die negativen Auswirkungen auf die Gesellschaft unterschätzt, die von revolutionären Technologien ausgehen. Doch kann Technologie selbst nicht mit den Begriffen gut oder schlecht beurteilt werden. Vielmehr muss beurteilt werden, wie die Gesellschaft diese nutzt. Heute stehen wir wieder am Rande einer solchen gesellschaftlichen Herausforderung.

Wir leben in einer global vernetzten Welt. Technologischer Fortschritt hat Daten zu einer der wichtigsten Ressourcen gemacht. Der Mitbegründer von Twitter, Evan Williams, erklärte in einem Interview der New York Times 2017 überraschenderweise das Folgende: „Ich dachte, wenn alle Menschen frei sprechen und Informationen und Ideen austauschen können, wird die Welt – automatisch – zu einem besserer Ort. Ich habe mich geirrt“.

Man könnte leicht den Eindruck gewinnen, dass dieses Phänomen neu ist, aber Niall Ferguson, Geschichtsprofessor und Senior Fellow des Hoover Institutes ist davon überzeugt, dass der heutige technologische Fortschritt und seine Auswirkungen auf die Gesellschaft mit der Erfindung des Buchdrucks durch Johannes Gutenberg im 15. Jhdt. vergleichbar sind. Die Druckerpresse hatte viele positive Auswirkungen auf den Fortschritt der Menschheit und katapultierte die Bibel 200 Jahre lang auf den ersten Platz der Buch-Bestsellerliste. Leider machte die gleiche Technik “Malleus Maleficarum”, auch bekannt als der „Hexenhammer“, für dieselbe Zeit zur Nummer 2 auf dieser Liste. Das Buch war die Grundlage für die Hexenjagd und brachte so vielen Unschuldigen den Tod. Sicherlich würde man heute die Inhalte des Buches als „Fake News“ bezeichnen.

GEGENWART & DIE WELT VON MORGEN

Wir alle gestalten heute die Welt von morgen, und unser Streben hat bereits zu viel Gutem geführt. Technologie und menschliche Kreativität haben bspw. dazu beigetragen, die Armutsquote weltweit massiv zu senken. In den letzten 25 Jahren wurden hierbei mehr als eine Milliarde Menschen extremer Armut befreit.

Betrachten wir den Moment so kommt man nicht umhin der aktuellen COVID-19-Pandemie einige Zeilen zu widmen. Es ist eine globale Herausforderung und könnte gleichzeitig die nächste Geschichte des menschlicher Brillanz und Wahnsinns sein. Wir werden dank der KI-basierten Analyseelemente enorme Fortschritte in der medizinischen Forschung und bei den Maßnahmen zur Pandemiebekämpfung erleben. Wir werden aber auch Zeugen einer Rezession werden, die historisch gesehen immer ein Element für Populismus und Nationalismus war. All dies in einem Umfeld von Angst und geschlossenen Grenzen. In diesen Situationen, in denen sich viele von hilflos fühlen, ging Wandel immer von fortschrittlichen Denkern aus, die von ihren Ideen überzeugt waren, von Kant über Ghandi bis zu den Vordenkern der heutigen Zeit.

In unserer offenen Gesellschaft und mit Machine- und Deep Learning Technologien in unseren Händen haben wir die Möglichkeit die Welt zu einem besseren Ort zu machen. Wir können in unseren Berufen viel Neues bewegen, und wir können gegen polarisierende Bewegungen und Ungerechtigkeit in jeder Hinsicht aufstehen und uns Gehör verschaffen. Wir können unsere Kreativität und unseren Intellekt einsetzen, um „den Fortschritt des Denkens” zu verteidigen, der schon immer das Ziel hatte, den Menschen von seiner Angst zu befreien“, genau wie es eines der Ziele des Zeitalters der Aufklärung war.

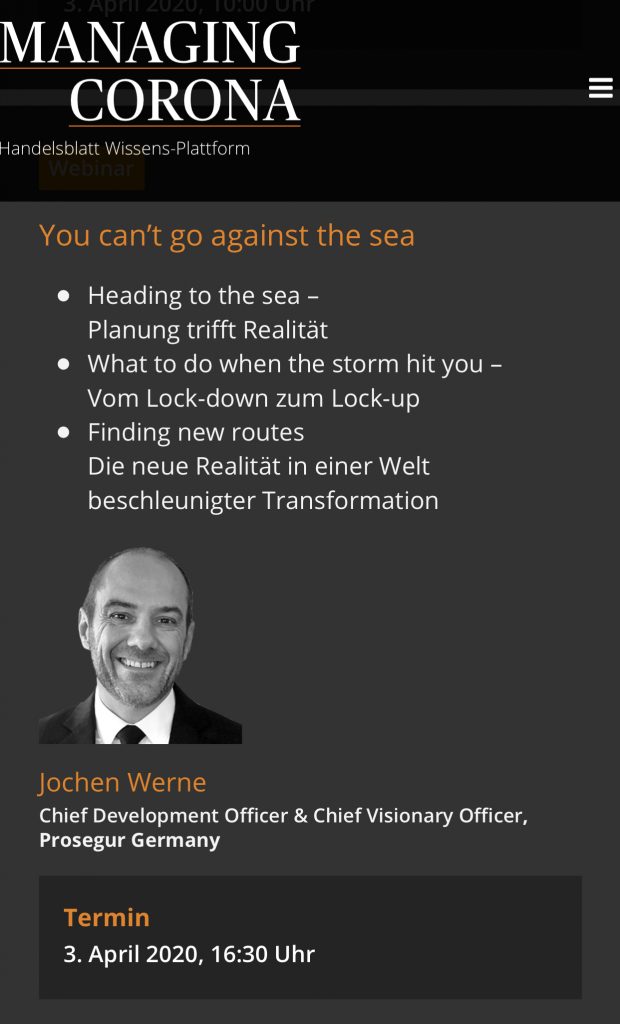

Heading to the sea – Planung trifft Realität What to do when the storm hit you – Vom Lock-down zum Lock-On Finding new routes Die neue Realität in einer Welt beschleunigter Transformation

Natalie Turner, Host of disruptive LIVE and Jochen Werne, CDO/CVO of Prosegur Cash Services, Germany in a lively discussion about the different aspects of change in companies and society. The interview touches aspects of fear and consciousness by giving examples reaching from Shakespeare to the Age of Enlightenment and our modern times of exponential technologies and artificial intelligence.

On Tuesday, November 5, 2019, Managing Director Dr. Stefan Hirschmann and his team from VÖB-Services organised an inspiring BANKENNETZWERK networking event “Digitisation and digital competence in banks” with an auditorium of 70 banking professionals.

Bankennetzwerk am 5.10.2019

im Holiday in Düsseldorf

Digitalisierung und Digitalkompetenz

Foto und Copyright

Bernd Schaller

Kiefernstr. 18

40233 Düsseldorf

www.schallerfoto.de

info@schallerfoto.de

00491776769111

Learning from history is crucial to understand the current societal changes triggered by technological progress. It‘s the basis to be able to make smart strategic decisions in a fundamentally changing business environment.

Some examples in the keynote referring to Professor Niall Ferguson‘s inspiring book „The Square and the Tower“. Enjoy some of his insights here

Bankennetzwerk am 5.10.2019

im Holiday in Düsseldorf

Digitalisierung und Digitalkompetenz

Foto und Copyright

Bernd Schaller

Kiefernstr. 18

40233 Düsseldorf

www.schallerfoto.de

info@schallerfoto.de

00491776769111

A crypto currency challenges technology, regulation and humans.

Author: Jochen Werne

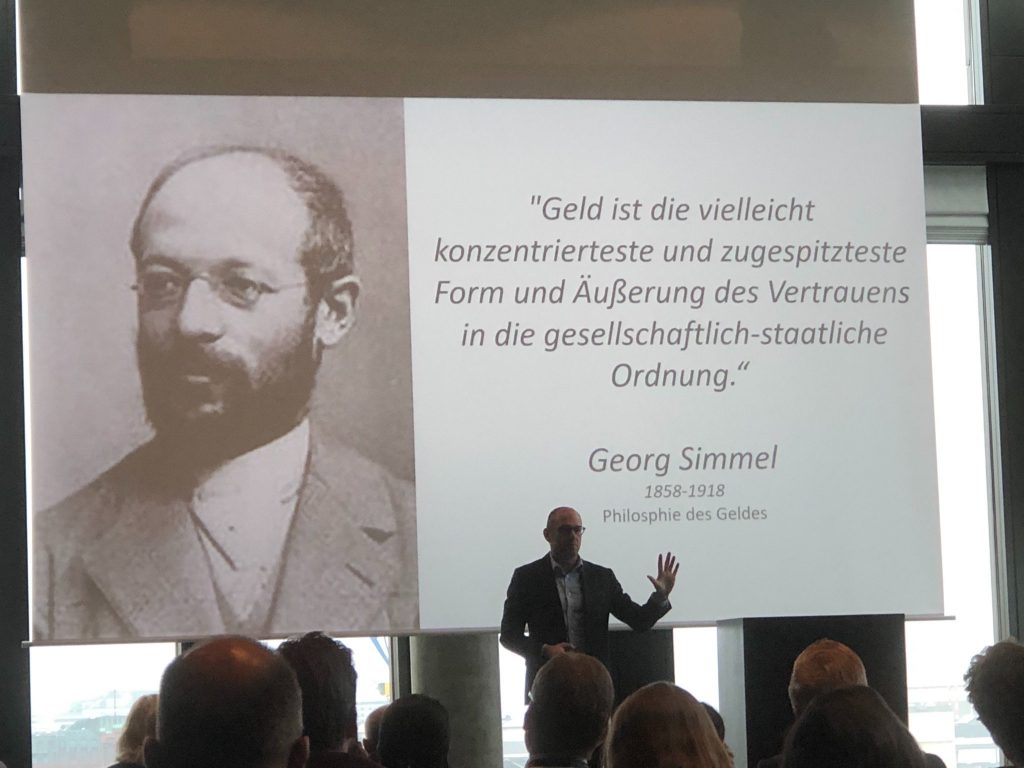

“Money is perhaps the most concentrated and acute form and expression of trust in the social-state order.”

Georg Simmel

In this clarity, the German philosopher and sociologist Georg Simmel, born in 1858, formulated the value of a currency in his work “Philosophy of Money”. This clear and comprehensible insight also provides a simple basis for understanding why, for example, states rely on the independence of their central banks. And just as simply the question arises, which order do you trust when it comes to crypto currency?

Almost 4,000 of these currencies now exist worldwide. After Bitcoin, Ether, XRP, Litecoin and Co., Libra now wants to establish itself as a future heavyweight in the market – and with a noble goal. Libra is to become the cashless payment option “for mankind” and make international payment easier.

Libra Coin – the currency of the future?

No crypto currency received comparable media attention, triggered only by the announcement of the project. And the emotionality and toughness with which the discussion is already being conducted shows how seriously the topic is being taken. It’s about reputation, influence, control, responsibility and only in the last instance about technology. Central banks and government bodies are sceptical about the “currency of the future” on a broad basis, even though the advancing globalization could argue for a single currency in the long run. A currency that supports a consistent free exchange of goods and services. Also under discussion is whether Libra Coin could be the means of payment for the approximately 1.7 billion people who have no access to banking services and whether the familiarity and the large target group of Facebook, combined with the announced low transaction costs, could make it possible to reach billions of people worldwide.

Challenges at all levels

Technically, not all hurdles have been cleared yet: In order to make a stable coin possible, it is necessary to find the right technology. It is precisely this stability that is supposed to distinguish Libra Coin from other crypto currencies and thus also make it suitable for skeptical end consumers. Members such as Mastercard, Paypal or Ebay should also provide the Libra Association with their names and brand promises additional confidence for the end consumer. But already today the alliance is not as stable as the founding members had hoped and the exits of Mastercard, Visa and Paypal weakens the consortium.

The Libra Association has repeatedly emphasized that it wants to comply with all regulatory aspects, but there are voices at the political and banking levels that are extremely sceptical about the project. The new payment system raises many questions in monetary and legal terms. Central banks and supervisors want to keep an eye on the influence of the potentially new currency and usually share the view that whoever acts like a bank must be treated like a bank. In other words, comprehensive requirements must be met and regulations observed – especially at the international level. This is difficult because current regulations are designed for the classical financial system, with which the Libra system has largely no points of contact. The aim is to keep total regulatory influence and not to allow any possible loopholes.

Despite its American origin, the Libra Coin is to be administered from Geneva by the Libra Association. The idea here is to be regulated by the Swiss Financial Market Supervisory Authority FINMA. Although Facebook has paid a lot of attention to the underlying technology, the legal issues still need to be clarified. Especially with regard to money laundering, consumer protection and possible misuse of the currency for illegal activities. Within the Association, there will be no special treatment for the founder Facebook, but equal voting rights for all members.

Acceptance and European values

With regard to Germany, it can be said that its citizens are within the international average as far as their affinity for digital is concerned. However, a historical-cutlurell caution can certainly be observed with regard to the topic of money, which certainly explains the well-known love of cash. A more pronounced European awareness of data protection with the General Data Protection Regulation (GDPR) makes many people, especially in Germany, sceptical about the subject. The fact that Libra was launched by Facebook is hardly a confidence booster after the Cambridge Analytica scandal. The fear of the transparent customer meets with security concerns about one’s own savings. Every German knows the quote: “Friendship ends with money” and thus new things are always put test. Culturally different in Sweden, where sometimes it’s only possible to pay by card. The same in China, where WeChat Pay and Alipay are no longer just a trend.

As always, changes are taking place step by step. It remains to be seen whether Libra Coin in its current form has future prospects. In any case, any change can only work if it is accepted and used by the end consumer despite all skepticism.

And this stands and falls – also in the digital world – with what Georg Simmel already put in the centre in terms of money in the 19th century: CONFIDENCE.

A more in-depth look at money and value can be found in the article “Coined Liberty 2.0“.

Following the keynote on “Libra in Retail?” at the Payment Summit 2019 in Hamburg, the article “Libra and the Dilemma of Trust” has been published to give participants further insides on the topic.

The “cobra effect” is a prime example of failed incentive structures. Good governance in banks and savings banks must serve stability and flexibility at the same time. Compliance with four principles is indispensable.

Well-intentioned is not well done yet. Science calls this the cobra effect. It goes back to an event when India was still a British colony. In order to control a cobra plague, a British governor placed a bounty on every snake that he killed. With the result that enterprising Indians began to breed cobras to collect the bounty. When the governor learned of this practice, he had the program stopped and the breeders released the snakes. Result: The problem had multiplied.

The Kobra effect is regarded as a prime example of failed incentive structures – and thus of failed governance. This word, derived from the French “governance” for government, is often used today, and with its almost inflationary mention, the blur surrounding it is also growing.

So let us recall: governance refers to the structures and forms of governance that exist in a society. This refers to the interaction between the state, the private sector and interest groups. The aim is to improve the management of an organisation or a political or social unit in order to achieve better results.

Stability as an objective of governance

However, it has become common practice to use governance primarily when it is not a question of state structures. For example, the term plays an important role in practically all companies that deal with the public in the form of customers or stakeholders. As a result of the blurred use of the term, case studies from politics are often used today to explain economic frameworks.

Undoubtedly, there are many parallels between the governance of states and the governance of private companies, in their structure and processes and thus also in their form of governance. The decisive factor for both is first and foremost stability and thus the ability to cope with major crises. For states, the core of stability is the constitution, which enables leadership during the crisis and at the same time serves as the basis for a way out of the crisis. A current example of this is the national crisis in Austria. The government has failed; until the next elections a transitional government of experts will lead the country and thus guarantee stability. Around this core, however, a state structure must also have a certain flexibility in order to be able to react to developments.

Stability plus flexibility

And this is where the differences to the private sector begin. States are not in competition with the private sector and generally continue to exist even after crises, even if in extreme cases the political system and its fundamental form of governance may change. The situation is different for companies. Of course, they also need a stable core. But they must be extremely flexible and adapt to market situations in order to survive in the long term. Their stability is based on the flexibility of the process organisation. When it comes to flexibility, smaller companies often have an advantage over large, difficult-to-maneuver corporations. We see this in the financial services industry with the example of FinTechs and InsurTechs. However, these relatively small companies often lack the stability they need to survive when consolidating.

Let’s take the example of the banking industry: It faces clear challenges – digitization, new competing business models, exponential technology leaps and ever shorter product cycles with lower margins and increasing regulation. Sustainable answers and the resulting strategies will only be found by those houses that are stable in themselves on the one hand, but are also capable of a degree of flexibility that has never been demanded of them in history on the other.

Four principles of good governance

But how does a company obtain the necessary stability? There are four principles for good, i.e. successful, governance, which must always be present:

Accountability: There must be an organization that is controllable and controlled. Accountability: The company as a whole and each individual employee are accountable for their actions. Openness: Only when employees, customers and stakeholders understand what is happening is transparency actually lived out. Fairness: Ethical conduct is one of the foundations for long-term value creation.

Governance must be lived

In order to achieve a satisfactory situation for both sides, the four principles of governance are indispensable. However, it is not enough to lay them down in statutes; they must also be lived by each individual.

In addition, the current major transformation issues, which not only the banks but also the entire economy have seized, should be seen as an opportunity for companies with a consolidated governance structure and remind us of a statement by the Roman philosopher Seneca, who said: “Only the tree that has been constantly exposed to gusts of wind is firm and strong, because in battle its roots are consolidated and strengthened”.

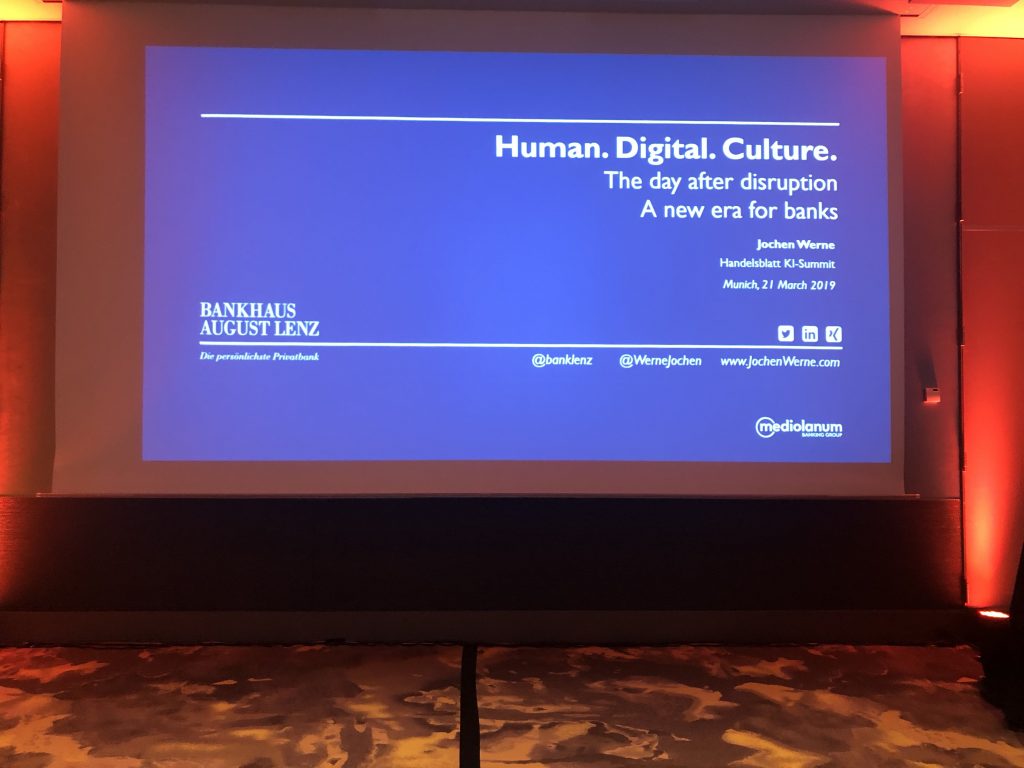

Jochen Werne is full-time Director & Authorized Officer for Bankhaus August Lenz & Co. AG of the Mediolanum Banking Group and is responsible for Business Development, Marketing, Product Management, Treasury & B2B Payment Services. In addition, he is involved in the development of non-profit organizations and a member of the Learning Systems Platform of the Federal Ministry of Education and Research.

The initiative www.wegofive.net addresses the question of how a unit of man and machine can be created in the working world of tomorrow and how algorithms can be seamlessly integrated into the organization in order to supplement the capabilities of employees.

In this first, introductory part of our interview Jochen gives us an insight into what has changed for him in the last decades – and he finds out that “Hamburg is probably the most beautiful city in Germany” 😉

As an independent interim manager, profile and team coach, Sascha Adam supports people, decision-makers and companies in actively shaping digital change.

More at www.wegofive.net/mission/about or www.sascha-adam.net.

Many thanks to the coast by east Hamburg in the Hafencity Hamburg for the permission to film here. A very recommendable location with obliging service, extraordinary menu and good drinks. Apropos, the background noises also give you the feeling of sitting directly with us 😉

German original

Jochen Werne ist hauptberuflich Director & Authorized Officer für das Bankhaus August Lenz & Co. AG der Mediolanum Banking Group und verantwortet dort die Bereiche Business Development, Marketing, Product Management, Treasury & B2B Payment Services. Darüberhinaus ist er am Aufbau gemeinnütziger Organisationen beteiligt und Mitglied der Plattform Lernende Systeme des Bundesministerium für Bildung und Forschung. Die Initiative www.wegofive.net geht der Frage nach wie in der Arbeitswelt von morgen eine Einheit aus Mensch & Maschine geschaffen werden kann und sich Algorithmen nahtlos in die Organisation integrieren, um die Fähigkeiten der Mitarbeiter zu ergänzen. In diesem ersten, einleitenden Teil unseres Interviews gibt uns Jochen einen Einblick was sich in den letzten Jahrzehnten für ihn verändert hat – und stellen fest, dass “Hamburg die wahrscheinlich schönste Stadt in Deutschland ist” 😉 Sascha Adam unterstützt als selbstständiger Interimsmanager, Profile- und Team-Coach Menschen, Entscheider und Unternehmen dabei den digitalen Wandel aktiv zu gestalten. Mehr unter www.wegofive.net/mission/about oder www.sascha-adam.net. Ganz herzlichen Dank an das coast by east Hamburg in der Hafencity Hamburg für die Genehmigung hier filmen zu dürfen. Eine sehr zu empfehlende Location mit zuvorkommender Bedienung, außergewöhnlicher Speisekarte und guten Drinks. Apropos, die Hintergrundgeräusche geben einem auch gleich das Gefühl direkt bei uns zu sitzen 😉

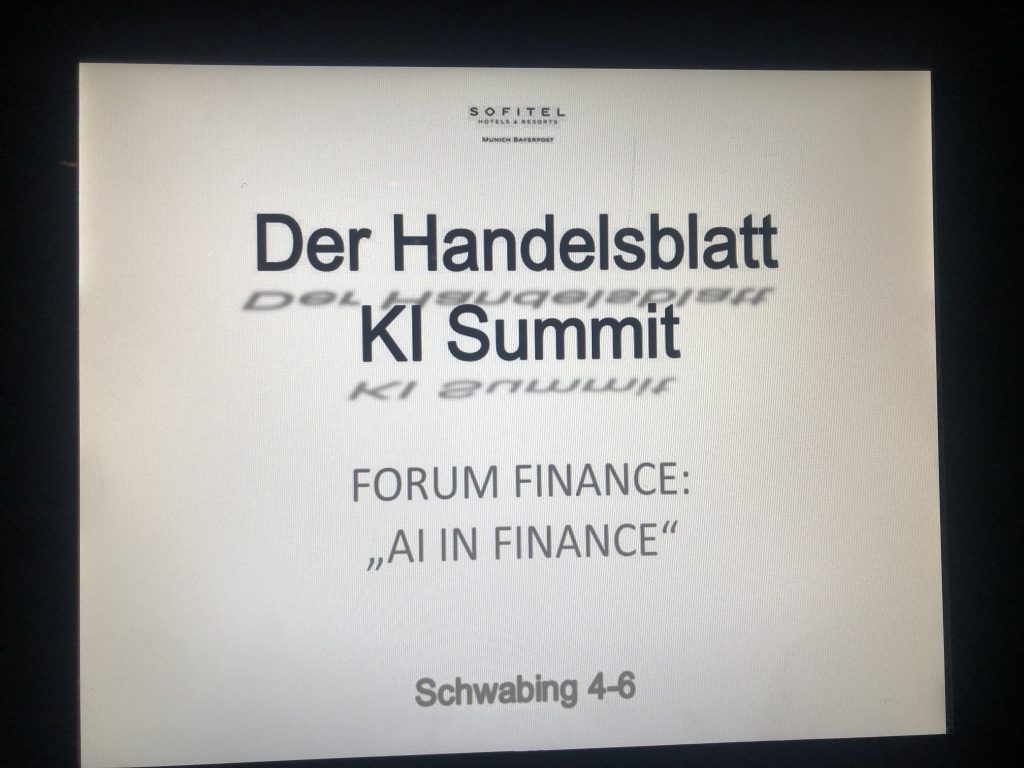

AI thought leaders met on the 21st and 22nd at the #HBAISummit not only to discuss the latest developments in machine and deep learning programming but especially real use-cases, trends in the start-up scene, the role of Germany and Europe in the AI race and the impact of AI on our society. Read more here

It has been a great pleasure discussing and being inspired by a highly engaged auditorium during two sessions: