“It has been a great pleasure and honour that author Maurizio Abbati has mentioned Expedition Antarctic Blanc in his new book as a successful example how public awareness for important environmental topics can be raised.”

Jochen Werne, Expedition Leader

This book, based on authoritative sources and reports, links environmental communication to different fields of competence: environment, sustainability, journalism, mass media, architecture, design, art, green and circular economy, public administration, big event management and legal language. The manual offers a new, scientifically based perspective, and adopts a theoretical-practical approach, providing readers with qualified best practices, case studies and 22 exclusive interviews with professionals. A fluent style of writing leads the readers through specific details, enriching their knowledge without being boring. As such it is an excellent preparatory and interdisciplinary academic tool intended for university students, scholars, professionals, and anyone who would like to know more on the matter.

Yacht Club de Monaco – Pre-Expedition Press Conference

Various case-studies and best practices help the reader to increase his Eco-awareness, making him involved in the main topic: Eco-communication

Interviews stimulate curiosity and allow the reader to investigate Eco-communication issues from different points of view

Numerous social and web links make the manual an original “platform” constantly open to dialogue

Various case-studies and best practices help the reader to increase his Eco-awareness, making him involved in the main topic: Eco-communication

Interviews stimulate curiosity and allow the reader to investigate Eco-communication issues from different points of view

Numerous social and web links make the manual an original “platform” constantly open to dialogue

It has been a great pleasure not only to give a speech at the plenary meeting for the Wirtschaftsjunioren Hamburg, but also to discuss in-depth the impact of AI on our society with a highly engaged auditorium.

Together with the Wirtschaftsjunioren / (c) WJ Hamburg

After the meeting the Wirtschaftsjunioren summarised the evening on Facebook as follows:

“At yesterday’s plenary meeting of the Education Committee, we combined the exciting topic of artificial intelligence with the beautiful (junior) life. Our keynote speaker Jochen Werne, Director Business Development & Marketing at Bankhaus Lenz, lecturer and author, gave a vivid presentation on the opportunities, dangers and challenges of AI for companies and society. How does it feel to pass on your activated smartphone to the person sitting next to you? What does a folded leaf have to do with the moon and AI?

Jochen Werne / (c) WJ Hamburg

We had SALT AND PEPPER as a guest for the further practical testing of AI. In a VR environment, we were able to build future production facilities using the BoxPlan product. The innovative Startup Smunch, the online canteen for happy teams, provided us with very real, delicious food. In the lounge-like atmosphere of the Ruby Hans Workspaces we found a great setting for stimulating conversations and networking.

Smunch / (c) WJ Hamburg

Ruby Hans Workspaces / (c) WJ Hamburg

Smunch Dinner / (c) WJ Hamburg

We would like to thank all guests and cooperation partners for a successful junior evening: Private Family Banker, Exclusive Agent Bankhaus August Lenz & Co. PUBLIC LIMITED COMPANY, SALT AND PEPPER technology and management consulting, software development, Smunch.co And remember, on 26.05.2019 is the European election, Step Up For Europe (see group photo 😉 )”

Wirtschaftsjunioren Hamburg – Engagement for Europe / (c) WJ HamburgProf. Dr. Peter Scholz (HSBA) & Sven O. Müller (7orcas) / (c) WJ Hamburg

Thank you very much to the Wirtschaftsjunioren Hamburg and Alexander Köhne for the highly appreciated invitation.

Original published in German in the Handelsblatt KI-Summit “KI-Business Guide”. Translation performed by DeepL.com

“Google, how are my stocks doing and what to do?” AI in the financial sector – the next big thing? by Jochen Werne, Bankhaus August Lenz

AI is making its way into every industry, but banks, insurance companies and FinTechs in particular are seeing a renaissance for their data-based business models in disruptive times. Jochen Werne, director and head of the innovation team at Munich-based private bank Bankhaus August Lenz, explains the role that the human factor will play in banking and consulting in the future.

Google, Apple, Facebook and Amazon (GAFA) have long seen artificial intelligence as the technology of the future. Banks and insurance companies also see the potential in machine and deep learning approaches to be a relevant player in the future in an increasingly technology-driven market environment. After “FinTech”, “Blockchain” and “Crypto-currencies”, “AI” is the new buzzword of the industry. From the AI-optimized chatbot to highly complex, self-learning, investment algorithms – the omnipresence of the term suggests that the integration of Artificial Intelligence into one’s own business model seems to be virtually necessary for survival. But is that really the case, where do we stand and which factors cannot be replaced by technology?

What becomes possible in times of exponential technologies is de facto nothing less than a revolution. The financial industry holds a vast amount of valuable and already processed data. Not only do they reflect our daily and extremely private life, from buying tickets for the subway via apps to the preference of our garments – but they reflect also the payment flows of entire companies and industries, and therefor our entire economy. Maturing AI systems not only make it easier to prepare and process this data, they also make it much cheaper, faster and more targeted. AI will not only enable banks to make their services more customer centric, it will also transform most areas of the financial industry – from asset management to business operations and money laundering prevention to marketing.

Data protection has top priority

Every major technological leap has historically been accompanied by a positive and an abusively usable development. TIME magazine recently published an article by Apple CEO Tim Cook entitled “It’s time for action on privacy. We all deserve control over our digital life”. Every electronic transaction generates customer-specific data. These structured data sets, which have been collected for many years, are now becoming the most valuable raw material. It’s important to create meaningful use-cases especially when it comes to the enrichment of existing structured data sets with external, possibly unstructured data. However, this is exactly where the risk lies. If sensitive data falls into the wrong hands and is deliberately misused, cyber attacks can cause considerable damage to individuals and groups. Trust is and remains therefore one of the most important assets of a credit institution or financial service provider. Consequently, the protection of customer data in a digital banking world has absolute priority today more than ever before. When using AI technology, it is therefore essential to use private and sensitive data in the interests of the customer. And this is where not only IT and cyber security departments of banks come into play, but also politics: their primary task must be to find meaningful solutions for handling the effects of the use of AI on society, the economy and thus on our lifes and the work of tomorrow. And this without endangering the competitiveness of our own country. The fact that this topic is taken seriously is evident not only in national initiatives such as the German Platform for Artificial Intelligence “Lernende Systeme”, but also, for example, in the European Artificial Intelligence shoulder-to-shoulder approach, which is being pushed forward at full speed by France and Germany.

The ideal model for private customer business: Connection of AI and human-based advise

In order to advance the acceptance of AI in the financial sector, it is important that existing digital tools are even better adapted to customer needs. The successful symbiosis between people and digital technology is indispensable. With the help of online financial forums, banking apps, vlogs and digital industry comparisons, private individuals can now achieve basically the same level of knowledge as financial professionals, but what is usually lacking is the successful filtering of the “information overload” and the consideration of the behavioral finance problem.

A realistic model for the successful transformation of the financial sector is therefore quite simple: streamline business models and processes, use data efficiently and always place the needs of customers at the centre of all activities. Taking advantage from technological progress always comes with successful deployment scenarios. Consequently, the technological revolution associated with the use of AI systems can only succeed if it is accepted by society – meaning, by us humans.

It’s greatly inspiring and an honour being part of this unique platform which is concentrating knowledge and illustrating perspectives in the field of artificial intelligence and self learning systems

The Plattform Lernende Systeme brings together expertise from science, industry and society for fostering Germany‘s position as an international technology leader. It understands itself as a forum for exchange and cooperation.

Designing self-learning systems for the benefit of society is the goal pursued by the Plattform Lernende Systeme which was launched by the Federal Ministry of Education and Research (BMBF) in 2017 at the suggestion of acatech. The members of the platform are organized into Working Groups and a Steering Committee which consolidate the current state of knowledge about self-learning systems and Artificial Intelligence. They point out developments in industry and society, analyse the skills which will be needed in the future and use real application scenarios to demonstrate the benefit of self-learning systems. A Managing Office at acatech coordinates the work of the platform.

Concept and aims of the platform

Self-learning systems are increasingly becoming a driving force behind digitalisation in business and society. They are based on Artificial Intelligence technologies and methods that are currently developing at a rapid pace in terms of performance. Self-learning systems are machines, robots and software systems that learn from data and use it to autonomously complete tasks that have been described in an abstract fashion – all without specific programming for each step.

Self-learning systems are becoming increasingly commonplace supporting people in their work and everyday lives. For example, they can be used to develop autonomous traffic systems, improve medical diagnostics and assist emergency services in disaster zones. They can help improve quality of life in many different respects, but are also fundamentally changing how humans and machines interact.

Self-learning systems have immense economic potential. As digitalisation takes hold, they are already helping companies in certain sectors to create entirely new business models based on data usage and are radically changing conventional value creation chains. This is opening up opportunities for new businesses, but can also represent a threat to established market leaders should they fail to react quickly enough.

Developing and introducing self-learning systems calls for special core skills, which need to be carefully nurtured to secure Germany’s pioneering role in this field. Using self-learning systems also raises numerous social, legal, ethical and security questions – with regard to data protection and liability, but also responsibility and transparency. To tackle these issues, we need to engage in broad-based dialogues as early as possible.

Plattform Lernende Systeme brings together leading experts in self-learning systems and Artificial Intelligence from science, industry, politics and civic organisations. In specialised focus groups, they discuss the opportunities, challenges and parameters for developing self-learning systems and using them responsibly. They derive scenarios, recommendations, design options and road maps from the results.

AI thought leaders met on the 21st and 22nd at the #HBAISummit not only to discuss the latest developments in machine and deep learning programming but especially real use-cases, trends in the start-up scene, the role of Germany and Europe in the AI race and the impact of AI on our society. Read more here

It has been a great pleasure discussing and being inspired by a highly engaged auditorium during two sessions:

There is no lack of buzzwording when it comes to trends in the financial sector: Disruption, FinTech, block chain, crypto. Currently, another term is climbing the zenith of a media hype – platform banking. And not without good reason. “Platform Banking” was voted “Financial Word of the Year” in 2018. Behind this lies the call for banking institutions to open up to third-party providers. Banks and savings banks should not only offer their own services on open platforms, but should also integrate third-party offers and services. Consistently thought through to the end, banks will thus become more intermediaries for all possible services and less providers of their own financial services. The legally necessary prerequisites for such an approach in the strictly regulated financial market have already been set in motion by the adoption of the Payment Services Directive PSD2. Will platform banking become a new hope for the industry, or another risk component in the attempt to lose fewer customers to new technology competitors?

The hype surrounding the topic is understandable: Eight of the ten world’s most valuable companies – Amazon, Google, Microsoft, Apple and Co. – have a platform in their business model. And even more striking: Only one of these companies was already among the top 10 worldwide in 2008. This growth potential, which is the result of the platform expansion, is of course intended by many industries to benefit themselves. The world of finance is also changing rapidly. In recent years, a variety of innovative developments have taken place in the areas of payment transactions and payments. The arrival of third party providers and fintechs has changed the market sustainably and comprehensively. According to a recent whitepaper by Deloitte Consulting, banks will also have to consider a platform strategy in the future: In the future, the customer base will also be able to access products and services from third-party providers in addition to the existing offering. The long-term goal behind this is well known – to retain existing customers, acquire new ones and increase margins.

Platform as recipe for success?

In general, a platform can be seen as a place where supply and demand meet. Economists call such a market – not a new discovery. Due to the digitization of all areas of business and life, geographical boundaries of the marketplaces belong to the past. The result: an almost unlimited number of supply and demand meet on a digital platform – and competition is known to stimulate business. In these business models, the so-called “network effect” ensures that with each new provider on a platform, the incentive for demanders and customers also increases. And in general the more demanders there are on the platform, the more lucrative it becomes for the suppliers. Both sides save enormous search and time efforts and transaction costs are reduced. In short, reflects this the recipe for success behind industry giants such as Amazon, AirBnB, Uber and Co. Nevertheless, there are existing fundamental reservations. The desire of many bank managers to grab a straw in order to grasp a component of hope in a difficult market environment seems understandable. However, blind action is fatal in this situation. Banks must not forget what the emergence of competition in the form of FinTechs has already revealed: frightening weaknesses with regard to their own modern hardware and software solutions, organisation and innovative corporate culture. The fact is that the challenge facing change management is proving to be enormous. And this already now, without having given space to the idea of creating a single platform. The current wave of closing down banking or partnership-based Robo Advisor solutions shows how quickly these carriers of hope can become problems. The commission model behind this, which is always transparent and low priced, is hardly profitable for the banking infrastructure and marginalises the added value that an institution is able to provide for its customers.

The complexity of the changes on all levels, starting with the completely changed, technological possibilities and their effects on the transformation of long-established business models, over the resulting new economic situation of the enterprises are enormous. The difference to the past decades lies in the temporal component. If companies today do not react directly to market changes, they open the way for competitors to their own customers. And this faster than ever before. In such disruptive times, all those involved want an “efficient” change process. However, active, well-considered and vital change management is often criminally neglected. For this one opens door and gate to blind actionism.

The business model of a financial platform is complex, the regulatory framework is strict and the willingness of customers to switch is only slightly visible. For this reason, this business model has so far been too uninteresting for Internet groups. And now, of all things, the banks, often perceived as conservative and unmodern, are to be transformed into digital platforms that can compete with Amazon & Co?

Enormous change management challenge

Banks need a forward-looking and sustainable strategy. That is beyond question. At the latest since the massive “democratization” of the Internet at the end of the 1990s, our lives have been shaped by leaps in technology. In short, the world feels like it is turning faster than ever before. What does this mean for the banks of the 21st century? Anyone who does not understand this exponential dynamic of technical possibilities or does not take them sufficiently into account in his business model can quickly lose touch – with the customers of today and tomorrow. Open banking is both an opportunity and a technological challenge for the banking industry. The European Payment Service Directive 2 – or PSD2 for short – has inevitably made opening up to third parties the focus of the digital strategy.

At the technical level, this is primarily associated with the use of programming interfaces, so-called APIs, which enable both internal and external cost-effective and fast access to data, as well as functions of software applications. What provides the end customer with a cross-product customer experience, means for banks to strategically cooperate with external partners. For FinTechs, cooperation is also advantageous. It creates fast access to customers and their data, as well as to the necessary financial and structural prerequisites.

Anticipating these developments requires a good eye for tomorrow’s customers. After all, customer data is a success driver for future business models. A few years ago, FinTechs began to “poach” their digital offerings among the customer base of traditional institutes. All of this culminated in Robo-Advisors, standardized, computer-controlled asset managers with low fees. It was therefore time for the banks to set sail anew. The plan was to enter into symbioses with FinTechs or “buy” their products directly into their own portfolios. For many large banks, it has become good form to enter into cooperation with small, independent and innovative financial service providers. This is also clearly demonstrated by the current situation of FinTechs. Mergers and co-operation are nothing else than a proof for the fact that the search for sustainable business models is not easy with a fixed idea to solve, not even with the platform strategy. Nevertheless, neither the previous business models nor the product possibilities seem to be mature.

Don’t forget the human factor

The personal relationship, the touchpoint between customer and consultant in the real world, has been increasingly reduced by the acceptance of digital banking. Nevertheless, even if a digital experience is a good thing for a modern bank, consumers continue to appreciate human contact points – especially in economically or politically turbulent times.

The challenge lies in providing the right balance between the digital experience and the traditional, trust based, personal customer relationship.

Jochen Werne

This is precisely the added value that banks can really deliver in this environment today. And this without having to rely on the healing promises of platform banking. Be a guide in the digital jungle and protect customers from ill-considered gut decisions. In addition, it is important to include the customer’s background, apart from monetary issues, in the decision-making process. This usually requires a counterpart. Not a digital one, but a human one. A person of heart and soul who generates trust and can provide a place for personal encounter. Today, it is the customer alone who determines where this is located and what it should look like. The same goes for when this meeting takes place. The modern customer expects the best possible service regardless of space and time, not only in view of the phenomenon of digital gadgets.

At a time of fast pace and constant digital transformation, it is ultimately the Bank’s task to invoke traditional values, ensure humanity and meet the need to be an institution that the client trusts. Perhaps even beyond monetary concerns.

It’s a great pleasure having the chance to meet international experts and supporting the Summit as Speaker on AI in Finance and with an evening fireside chat about leadership, transformation and the sea.

Fireside Chat in der Future Lounge about Leadership in times of transformation

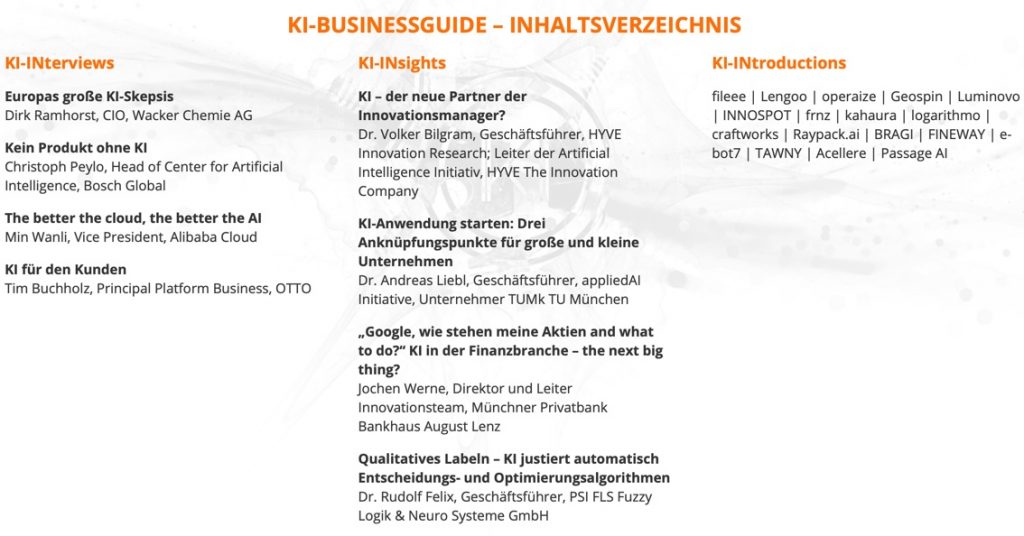

KI-INsights Businessguide

Read interviews and articles from experts in the KI-Businessguide published by the Handelsblatt for the Summit and free to download on this website

It was a pleasure supporting the publication with reflection on AI developments in the Financial Industry called: “Google, how are my stocks doing and what to do?” AI in the financial sector – the next big thing?

AI in Finance Session in the Handelsblatt KI-SUMMIT

by JOCHEN WERNE, April 4, 2018 – Original published in DER BANK-BLOG – Translated by DeepL

FinTechs offer innovative digital services, at a speed that traditional banks have difficulties to compete. What phases do these new technologies go through when they are introduced and what can banks learn from it?

Until recently, there were no alternatives to traditional banking – then FinTechs came along. In many cases, they claim nothing less for themselves than to have triggered a revolution in the financial sector. And there is no doubt that FinTechs, with their special offers and concept of initially approaching the problem from the customer’s point of view, free of regulatory and organisational considerations, are hitting the nerve of time. In addition, they show the pain points, i.e. the wishes of financial customers that have not yet been optimally satisfied. These are exactly the demands that have to be met in times of disruptive innovation.

The question of where this change should begin, with which project or projects is the decisive management question. It can be said in advance that this question cannot be answered in general, as too many components of the environment, orientation and corporate governance structure of the respective institution have to be taken into account.

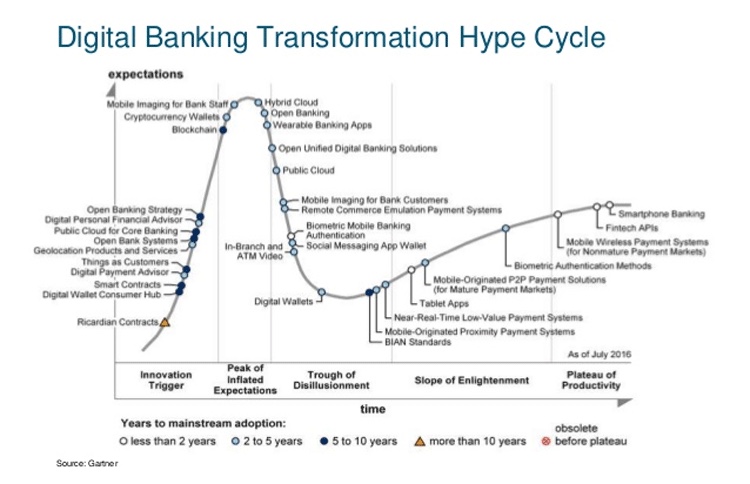

A look at Gartner’s Hype Cycle for Digital Banking Transformation can help the pre-strategy decision-making process. It looks at most future issues and arranges them along a curve that shows which phases of public attention a new technology goes through when it is introduced.

By means of a technological trigger, a specialist audience and other third parties begin to increase the level of awareness of an innovation or even just an idea for an innovation (on the rise). Expectations rise disproportionately and some time later they reach the peak of exaggerated expectations (at the peak). Since the creation of expectations progresses much faster than their fulfilment, a first disappointment is inevitable (sliding into the through). Then, in the so-called “path of enlightenment”, a realistic examination of the technology begins, in which lower media interest and productive deployment scenarios emerge (climbing the slope), which then lead to a plateau of productivity (entering the plateau) – if the technical innovation turns out to be relevant.

Der Gartner Digital Banking Transformation Hype Cycle 2016

Gartner categorized in 2016 Digital Banking Transformation topics as follows:

On the Rise – Ricardian Contracts, Digital Wallet Consumer Hub, Smart Contracts, Digital Payment Advisor, Things as Customers, Geolocation Products and Services, Open Bank Systems, Public Cloud for Core Banking, Digital Personal Financial Advisor, Open Banking Strategy At the Peak – Blockchain, Cryptocurrency Wallets, Mobile Imaging for Bank Staff, Hybrid Cloud, Open Banking Wearable Banking Apps Sliding Into the Trough – Open Unified Digital Banking Solutions, Public Cloud, Mobile Imaging for Bank Customers, Remote Commerce Emulation Payment Systems, Biometric Mobile Banking Authentication, Social Messaging App Wallet, In-Branch and ATM Video, Digital Wallets, BIAN Standards, Mobile-Originated Proximity Payment Systems, Near-Real-Time Low-Value Payment Systems Climbing the Slope – Tablet Apps, Mobile-Originated P2P Payment Solutions (for Mature Payment Markets), Biometric Authentication Methods Entering the Plateau – Mobile Wireless Payment Systems (for Nonmature Payment Markets), FinTech APIs, Smartphone Banking

REMARK by the author: compare the 2018 situation in the Gartner study available HERE

Conclusions for incumbent banks

The listed topics should be familiar to every member of the management and the responsible managers in the area of strategic corporate development, as they can become key value drivers for the future orientation of your institute. The entrepreneur Brett King expressed it even more radically in his 2016 book “Augmented: Life in a smart world”:

“If you’re a bank, this is the year you start redesigning every single product in your wheelhouse.”

Brett King

Transparent fee structures and the simplest possible access to the banking system are basic requirements for customers. Whether FinTechs can offer sustainable business models in the long term remains to be seen. They, too, cannot escape the pressure on margins and changing customer demands. FinTechs make it easier for their customers to access the banking sector and can thus counteract the dissatisfaction of traditional bank customers in the service sector. They offer services where traditional banks often do not yet act flexibly enough. Established financial service providers are thus forced to rethink, adapt or further develop their business models. Those who escape this change will have to contend with major competitive disadvantages in the future.

About the author: Jochen Werne and the Munich based private bank August Lenz on-boarded five FinTechs within just one year. FinTech Finance wrote about the transformation "A bank becomes driver of innovation in digitalisation"

Chapter 5: Transformation of an analogue private bank into an innovation driver Reflection on change, technological progress and human behaviour in disruptive times The article analyses and discusses the changes, challenges, decision paths and implementation practices of Bankhaus August Lenz in the years 2014 to 2016. In addition, the author would like to provide executives and managers entrusted with the transformation of their institution with practical arguments that may help them to cope better with daily challenges in change management practice. As a traditional private bank with a European parent, the task was not only to complete the transition away from a fully analog bank, but also to adapt the Group’s strategy for the German market with the budget adapted to the size of the institution. The most important internal customer was also integrated into the change: the Family Banker®, which is at the heart of the philosophy and is responsible for customer contact. This human contact and personal contact is the guarantee for the indispensable relationship of trust between customer and bank. The author examines issues such as coopetition, agile project management approaches and cooperation with FinTechs. In addition, topics such as value proposition, behavioral finance, the need to concentrate on core issues, the importance of personal consulting in the digital age and exchange in an international working environment as well as communication are treated as essential success factors. The paper does not claim to be perceived as a scientific work, but focuses on the practical implementation of the core problem of a market participant in a disruptive market – the question of how to restructure and realign companies in order to continue to play a role as a market player in the future.