It has been pleasure being guest author for the DIGIPRAKTIKER, Finanz Colloquium Heidelberg.

What role does the human factor play in times of exponential technological progress?

Author: Jochen Werne, Director Business Development, Product Management, Treasury and Payment Services at Bankhaus August Lenz & Co. AG

I. Introduction

The only constant in history was, is and remains change. Gutenberg’s invention of the printing press in 1450 was a milestone on the timeline of human development. Today we still take note of this invention, which was considered an innovation at that time, but we have long lived surrounded by smartphones and cloud applications, in which we can store the most private information and retrieve it from anywhere in the world. Today’s change is being driven by a veritable digital revolution.

Digital change already has fundamental consequences for individuals and their lifestyles, but it is developing its full potential when it comes to interacting with our social environment. In times of smart robotics and maturing systems in relation to artificial intelligence, the question arises again and again what role humans play on the stage of these technologies. Is he …

25. JULY 2019 BY JULIANE WAACK – KEYNOTE BY Jochen Werne

Digital Expert Author Juliane Waack

For the opening keynote of our ec4u virtual conference Digital Thoughts on May 23rd, Jochen Werne, Director Marketing & Authorised Officer at Bankhaus August Lenz, talked about opening up to the digital transformation. It turns out, what we associate with technology and what it actually offers are often two completely different things.

Jochen Werne

„Companies and people need to participate actively in the transformation. We need to move. It’s impossible to be a passive participant in the transformation.“

It has been a great pleasure giving an interview to Bernhard Bomke, about the development of the Robo-Advisor market in Germany, Innovation, Banking and the impact of Artificial Intelligence.

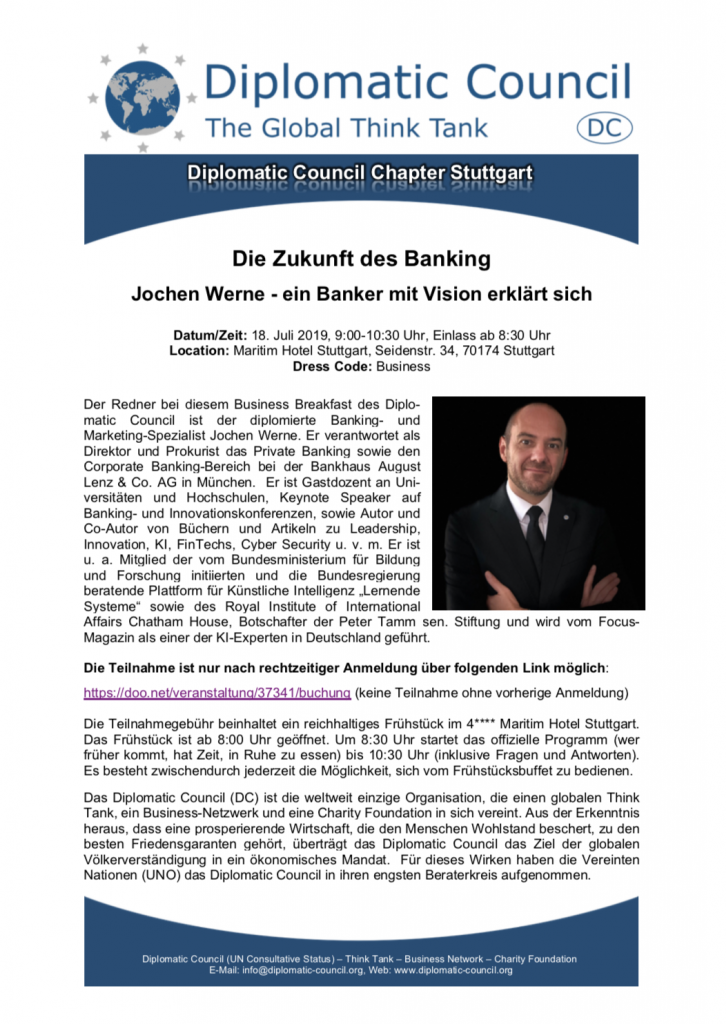

The speaker this morning is Jochen Werne, a graduate banking and marketing specialist. As director and authorized signatory, he is responsible for private banking and corporate banking at Bankhaus August Lenz & Co. AG in Munich. He is guest lecturer at universities and colleges, keynote speaker at banking and innovation conferences, author and co-author of books and articles on leadership, innovation, KI, FinTechs, Cyber Security and much more. He is a member of the platform for artificial intelligence “Learning Systems” initiated by the Federal Ministry of Education and Research and advising the German Federal Government as well as of the Royal Institute of International Affairs Chatham House, ambassador of the Peter Tamm sen. foundation and is listed by Focus-Magazin as one of the AI experts in Germany. He is the founder of the Global Offshore Sailing Team GOST and co-founder of the NGO Mission4Peace, which is dedicated to historical research, building international diplomatic relations and promoting international dialogue.

The participants will also get to know the Diplomatic Council (DC) this morning. It combines a global think tank, a business network and a charity foundation in a unique organization with consultative status at the United Nations. Stephanie Stoerk, Chapter Director DC Stuttgart, explains what distinguishes the Diplomatic Council from all other networks and what advantages it offers its members.

Breakfast is open from 8:30 am. At 9:00 a.m. we start our official program (whoever comes earlier has time to eat in peace), which lasts until 10:30 a.m. (including questions and answers). In between there is always the possibility to eat from the rich breakfast buffet.

PROGRAMM

Der Redner an diesem Morgen ist der diplomierte Banking- und Marketing-Spezialist Jochen Werne. Er verantwortet als Direktor und Prokurist das Private Banking sowie den Corporate Banking Bereich bei der Bankhaus August Lenz & Co. AG in München. Er ist Gastdozent an Universitäten und Hochschulen, Keynote Speaker auf Banking- und Innovationskonferenzen, sowie Autor und Co-Autor von Büchern und Artikeln zu Leadership, Innovation, KI, FinTechs, Cyber Security u. v. m. Er ist u. a. Mitglied der vom Bundesministerium für Bildung und Forschung initiierten und die deutsche Bundesregierung beratende Plattform für Künstliche Intelligenz „Lernende Systeme“ sowie des Royal Institute of International Affairs Chatham House, Botschafter der Peter Tamm sen. Stiftung und wird vom Focus-Magazin als einer der KI-Experten in Deutschland geführt. Er ist Gründer des Global Offshore Sailing Teams GOST und Co-Founder der NGO Mission4Peace, die sich der historischen Forschung, dem Aufbau internationaler, diplomatischer Beziehungen sowie der Förderung eines internationalen Dialogs widmet.

Darüber hinaus lernen die Teilnehmer an diesem Morgen das Diplomatic Council (DC) kennen. Es verknüpft einen globalen Think Tank, ein Business Network und eine Charity Foundation in einer einzigartigen Organisation mit Beraterstatus bei den Vereinten Nationen. Stephanie Stoerk, Chapter Director DC Stuttgart, informiert, was das Diplomatic Council von allen anderen Netzwerken unterscheidet und welche Vorteile sich daraus für die Mitglieder ergeben.Das Frühstück ist ab 8:30 Uhr geöffnet. Um 9:00 Uhr starten wir unser offizielles Programm (wer früher kommt, hat also Zeit, in Ruhe zu essen), das bis 10:30 Uhr andauert (inklusive Fragen und Antworten). Es besteht zwischendurch jederzeit die Möglichkeit, sich vom reichhaltigen Frühstücksbuffet zu versorgen

The speaker this morning is Jochen Werne, a graduate banking and marketing specialist. As director and authorized signatory, he is responsible for private banking and corporate banking at Bankhaus August Lenz & Co. AG in Munich. He is guest lecturer at universities and colleges, keynote speaker at banking and innovation conferences, author and co-author of books and articles on leadership, innovation, KI, FinTechs, Cyber Security and much more. He is a member of the platform for artificial intelligence “Learning Systems” initiated by the Federal Ministry of Education and Research and advising the German Federal Government as well as of the Royal Institute of International Affairs Chatham House, ambassador of the Peter Tamm sen. foundation and is listed by Focus-Magazin as one of the AI experts in Germany. He is the founder of the Global Offshore Sailing Team GOST and co-founder of the NGO Mission4Peace, which is dedicated to historical research, building international diplomatic relations and promoting international dialogue.

The participants will also get to know the Diplomatic Council (DC) this morning. It combines a global think tank, a business network and a charity foundation in a unique organization with consultative status at the United Nations. Stephanie Stoerk, Chapter Director DC Stuttgart, explains what distinguishes the Diplomatic Council from all other networks and what advantages it offers its members.

Breakfast is open from 8:30 am. At 9:00 a.m. we start our official program (whoever comes earlier has time to eat in peace), which lasts until 10:30 a.m. (including questions and answers). In between there is always the possibility to eat from the rich breakfast buffet.

Translated with www.DeepL.com/Translator

PROGRAMM

Der Redner an diesem Morgen ist der diplomierte Banking- und Marketing-Spezialist Jochen Werne. Er verantwortet als Direktor und Prokurist das Private Banking sowie den Corporate Banking Bereich bei der Bankhaus August Lenz & Co. AG in München. Er ist Gastdozent an Universitäten und Hochschulen, Keynote Speaker auf Banking- und Innovationskonferenzen, sowie Autor und Co-Autor von Büchern und Artikeln zu Leadership, Innovation, KI, FinTechs, Cyber Security u. v. m. Er ist u. a. Mitglied der vom Bundesministerium für Bildung und Forschung initiierten und die deutsche Bundesregierung beratende Plattform für Künstliche Intelligenz „Lernende Systeme“ sowie des Royal Institute of International Affairs Chatham House, Botschafter der Peter Tamm sen. Stiftung und wird vom Focus-Magazin als einer der KI-Experten in Deutschland geführt. Er ist Gründer des Global Offshore Sailing Teams GOST und Co-Founder der NGO Mission4Peace, die sich der historischen Forschung, dem Aufbau internationaler, diplomatischer Beziehungen sowie der Förderung eines internationalen Dialogs widmet.

Darüber hinaus lernen die Teilnehmer an diesem Morgen das Diplomatic Council (DC) kennen. Es verknüpft einen globalen Think Tank, ein Business Network und eine Charity Foundation in einer einzigartigen Organisation mit Beraterstatus bei den Vereinten Nationen. Stephanie Stoerk, Chapter Director DC Stuttgart, informiert, was das Diplomatic Council von allen anderen Netzwerken unterscheidet und welche Vorteile sich daraus für die Mitglieder ergeben.

Das Frühstück ist ab 8:30 Uhr geöffnet. Um 9:00 Uhr starten wir unser offizielles Programm (wer früher kommt, hat also Zeit, in Ruhe zu essen), das bis 10:30 Uhr andauert (inklusive Fragen und Antworten). Es besteht zwischendurch jederzeit die Möglichkeit, sich vom reichhaltigen Frühstücksbuffet zu versorgen

Jochen Werne, Director Marketing & Business Development at Bankhaus August Lenz, explains in his keynote address how we can shape the future from the innovations and topics of the past and why digitization must be thought of not only technologically but also culturally.

ec4u Digital Thoughts Conference Keynote

Jochen Werne, Direktor Marketing & Business Development beim Bankhaus August Lenz, erläutert in seiner Keynote, wie wir aus den Innovationen und Themen der Vergangenheit in der Gegenwart die Zukunft gestalten können und warum Digitalisierung nicht nur technologisch, sondern auch kulturell gedacht werden muss.

Artificial intelligence is the new buzz word of the financial industry, says Jochen Werne. In view of the rapid pace of technological development it is becoming a source of hope for the banks – and rightly so, writes the author. After all, banks have an enormous amount of data at their disposal. Despite all the digitalisation and areas of application of AI, Werne sees the chance for a renaissance of consulting as a link between people and the technical world. Red. Bank und Markt

German: Künstliche Intelligenz ist das neue Buzz-Wort der Finanzbranche, sagt Jochen Werne. Angesichts der rasanten technologischen Entwicklung wird sie zum Hoffnungsträger für die Banken – zu Recht, meint der Autor. Schließlich verfügen Banken über einen enormen Datenschatz. Trotz aller Digitalisierung und Einsatzbereiche von KI sieht Werne jedoch die Chance auf eine Renaissance der Beratung als Bindeglied zwischen Mensch und technisierter Welt. Red.

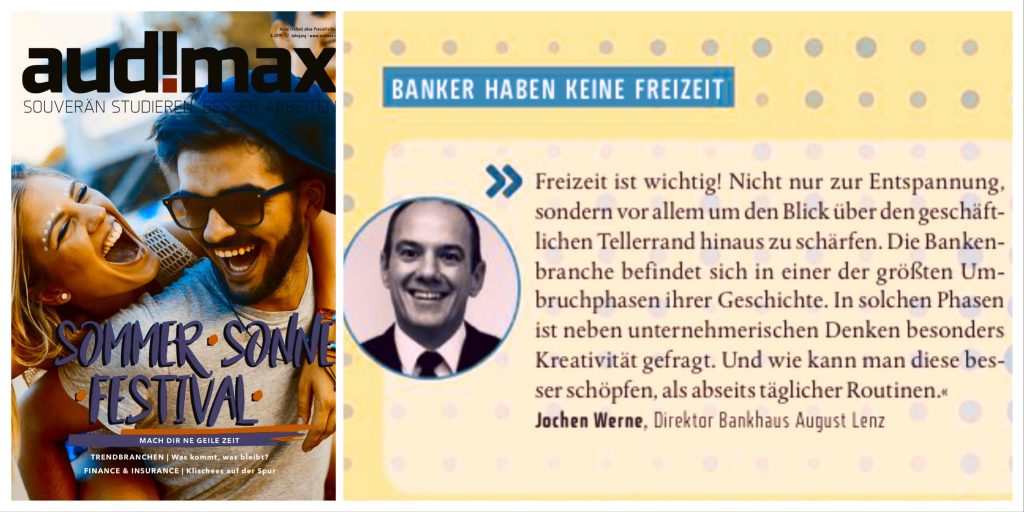

Jochen Werne, Direktor der Bankhaus August Lenz & Co. AG antwortet AudiMax auf die Frage nach dem Klischee, dass Banker keine Freizeit haben. Text: Felix Schmidt / AudiMax

“Freizeit ist wichtig! Nicht nur zur Entspannung, sondern vor allem um den Blick über den Tellerrand hinaus zu schärfen. Die Bankenbranche befindet sich in einer der größten Umbruchphasen ihrer Geschichte. In solchen Phasen ist neben unternehmerischen Denken besonders Kreativität gefragt. Und wie kann man dies besser schöpfen als abseits täglicher Routinen”

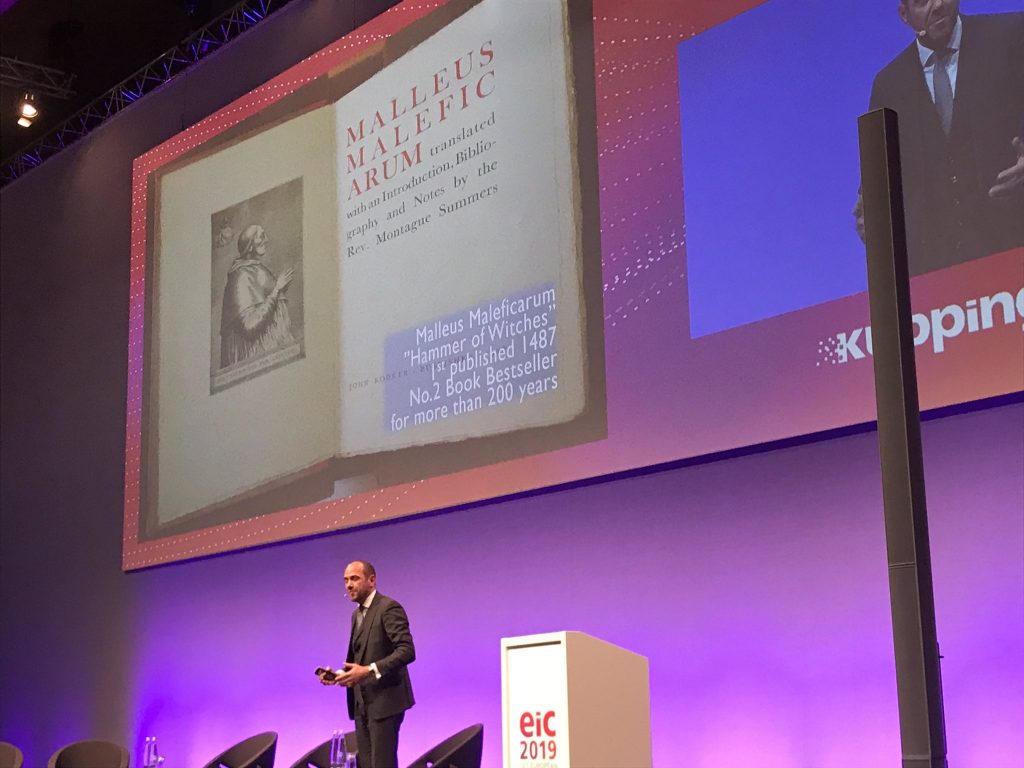

It has been greatly inspiring giving a keynote on the impacts of AI on business and society and to discuss with some of the 800 thought leaders, leading vendors, analysts, visionaries and executives at the highly recognised Kuppinger Cole European Identity & Cloud Conference 2019.