Does cash have a future? An article by Dunja Koelwel, editor in chief of gi Geldinstitute | 20.10.2020 – 13:02

Please follow this LINK for the original source in German. Translation made by DeepL.com

Cashless payment is on the advance worldwide, only the Germans hang on to cash. gi Geldinstitute therefore wanted to know from Ralf-Christoph Arnoldt (Bundesverband der Deutschen Volksbanken und Raiffeisenbanken BVR), Jochen Werne (Prosegur Germany), Dr. Harald Olschok (BDSW) and Leif Wienecke (Solarisbank) Does cash still have a future?

Signs such as “Cash only” should be a thing of the past in Germany, according to the digital association Bitkom. Wherever customers can pay, at least one digital payment option that can be used throughout Europe should be offered on a mandatory basis, according to the “Bitkom theses on freedom of choice in payment”.

“Cash shows itself to be an anchor of trust in uncertain times. With increasing concern about the corona virus, the amount of physical cash in circulation in the USA, for example, has risen,” says Jochen Werne, member of the management of Prosegur Cash Services Germany. gi geldinstitute therefore asked: What is the current situation regarding ‘war on cash’?

Since the Corona crisis, more and more people have been paying with cards or smartphones instead of with coins or notes. Is this a trend that is slowly eliminating cash? What is your perception?

Ralf-Christoph Arnoldt: Indeed, in recent months we have seen gains in card payments, especially in payments with Girocard. In the first half of 2020, transaction figures have increased by 20.7 percent compared to the same period last year. However, cash still plays an important role in everyday life in Germany, even if this love is eroding.

According to the Eurohandelsinstitut (EHI), the share of cash in turnover in 2019 was still 45.5 percent. Cash offers some advantages from the customer’s point of view. Paying with cash is convenient for the customer, anonymous, immediately final. Cash is freedom for customers. Regulators and business circles involved in the cash circle should accept this as a fact and not force them to change it.

Dr. Harald Olschok: Without doubt, a new phase of “war on cash” began during the Corona crisis. 75 percent of the member companies of the BDGW expect sales next year to be up to 20 percent lower than in the past. We assume that the proportion of cash payments in the retail sector will fall from around 48 percent at the beginning of 2020 to well below 40 percent. However, the crisis has also shown that Germans continue to have great confidence in cash as a secure means of payment and store of value. According to a survey by YouGov, Germans also cannot imagine living in a cashless society.

Leif Wienecke: Since the Corona crisis, we have seen an acceleration of many trend developments, some of which were already foreseeable before. This also includes contactless payment. This customer behaviour, which is relatively new in Germany, fits in well with corona-related hygiene measures. Basically, it can be said that, in addition to hygiene considerations, end customers are primarily looking for speed when choosing a means of payment. This is where digital and contactless payment methods come into play. Over the next few years, we will see a further decline in cash payments and an increasing use of digital payment methods such as mobile wallets.

Jochen Werne: What is important to people when it comes to their money – the “fruits of their labour”? Certainly its unlimited availability. If they can have confidence that they can get their money at any time, people choose the payment option that is most convenient for each individual. Some prefer to pay by smartphone, while for others it’s “only cash is true”. It is fundamental that we as consumers are free to decide from which means of payment we can freely choose. Freedom of choice is the key word.

A “per cash” argument often made is that technology is vulnerable and that in a crisis the value of security is always the highest good. This is why many people have been hoarding cash at the beginning of the lockdown. Do you believe that this money will now come back into circulation? And what do you think about the technological error potential of digital payment options?

Ralf-Christoph Arnoldt: The fact that cash was hoarded at the beginning of the lockdown was more due to the fact that people thought the cash supply could be endangered because of the Corona crisis. But that quickly proved to be incorrect. In the meantime, the hoardings have been continuously disbanded. We can see this, among other things, in the fact that the payout volumes at ATMs are still about 25 percent below the pre-corona level. If you want to compare the security of cash with card payments or digital payment options, you don’t get very far. If cash is stolen, for example, it is gone for good. If a payment card is stolen, the bank is usually liable.

Jochen Werne: It is undeniable that cash is seen by many as an anchor of trust in uncertain times. Electronic payment methods always risk a loss of trust due to technical failures. One of the last of these incidents was not long ago: during the pre-Christmas business on 23 December 2019, of all days, EC card payments were not accepted at many terminals. Many consumers who rely solely on digital payments have probably already had similar experiences of lesser consequence. Such situations can be observed time and again at the cash desks in department shops and supermarkets – for example, when the NFC chip on a card or simply the card reader does not work. Soon the eyes of the people standing around in the shopping queue turn to the payer, impatient and interested, trying to find out the name on the card of the supposedly insolvent unlucky person. Nevertheless, modern technologies are becoming more and more stable over time and a balance will be established between the various payment methods. Just as the “hoarded” will be returned to consumption or investment after the crisis. A cycle that, soberly, has always existed historically.

It became apparent that banks would no longer be able to offer free cash withdrawals from ATMs in the long term. This affects in particular people on low incomes, the elderly and, in general, all those who do not have access to digital forms of payment. Which solution do you think makes the most sense?

Leif Wienecke: Indeed, an accelerated dismantling of bank branches has been observed in recent months, but also before. The cost-benefit ratios seem to be out of proportion. Many end customers, especially older people, are suffering as a result. At the same time, however, one can also read about the creative solutions that savings banks, for example, are using to offer customers in rural areas the service they are used to (e.g. branch on wheels, transfer bus). I believe that other companies will fill the gap left by the banks. For some years now, supermarkets and petrol stations, for example, have been offering free “withdrawal” of cash. This trend to integrate banking services into the context of everyday life is known as contextual banking. The end customer wants to have access to cash or transactions wherever he or she is. As Solarisbank, we see the future in banking here.

Jochen Werne: Making an individual’s assets available as cash causes costs, just as paying with a card costs consumers money. The latest evaluation of 294 account models of 125 credit institutions in Germany by Stiftung Warentest shows that 55 models already charge fees for payment with the Girocard. It is the task of the institutions not only to manage their customers’ money, but also to meet the customer’s wish to make these assets available to them again in the form of cash or book money. The current practice of offering cash or accounts without fees and cross-subsidising them in return is a German phenomenon. The former head of BaFin, Dr. Elke König, already raised the question critically more than five years ago at the “Bank of the Future” event.

Today’s pressure on margins at banks now demands this adjustment. It is undisputed that, according to the German Bundesbank, ATMs are the most popular source of cash, accounting for 84 per cent of all cash withdrawals. Their number has risen by a good 18 per cent in Germany in recent years. On average, there is one ATM per 1,415 inhabitants. ATMs are therefore of enormous social and economic importance. It is not surprising that the area of “cash supply” is expressly listed as a “critical service” in Section 7 of the Critical Service Ordinance of the Federal Office for Information Security (BSI-KritisV), as a “service for the supply of the general public (…), the failure or impairment of which would lead to considerable supply bottlenecks or to threats to public security”. The fact that banks have to provide cash and cards to their customers, but are generally not able to do so profitably without charging is a long-term problem and needs to be improved. However, there is room for debate as to whether charges are the right way forward for consumers.

For US economics professor Kenneth Rogoff, the abolition of large banknotes is a first step. According to Rogoff, cash is synonymous with crime and the shadow economy – and in this respect it is a threat to the general public. Is cash really more “crime-sensitive” than digital payment methods?

Dr. Harald Olschok: As a “learned” Freiburg economist, I am always appalled by the populist and simplistic theses of the former chief economist of the IMF. It is much worse than you suggest. For Rogoff, “there is no question that cash plays a vital role in criminal activities, including drug trafficking, organised crime, extortion, corruption of authorities, trafficking in human beings and money laundering. (Der Fluch des Geldes, Munich 2016, p. 11). Oh yes, and undeclared work and illegal immigration are also owed to cash. Unfortunately, it has also been heard in the euro area. The 500 euro banknote has already been abolished. At the heart of the Rogoffian theses is the abolition of cash in order to impose negative interest rates. People should not save, but spend their money. This ignores the fact that fraud with non-cash means of payment, such as crypto-currencies, is booming. I expect that these forms of fraud will continue to increase. We must therefore assume the opposite.

Ralf-Christoph Arnoldt: Passing on a USB stick with millions of dollars in crypto-currencies, for example, is as easy as passing on a banknote. Criminals and the black economy are also part of the trend towards digitalisation, unfortunately sometimes even ahead of the investigating authorities.

Leif Wienecke: There is a lot of discussion on this topic and also conflicting studies. The Federal Government’s decision to tighten the reporting requirements for notaries, for example in real estate transactions, underlines Rogoff’s thesis. Nevertheless, I believe that it is not possible to generalise. Certainly, the anonymity of cash brings some advantages for criminals and money laundering can be curbed by switching to more strongly regulated, digital payment procedures.

And what about security? With cash, the problem is counterfeiting, with digital payments, for example, the tapping of identities and data. What is easier to protect?

Ralf-Christoph Arnoldt: I don’t see a big difference. It is always a mutual arms race. New security features for cash require more know-how and greater investment for counterfeiters. It is becoming more difficult, the number of offenders is getting smaller, but the sums that a counterfeiter puts on the market are bigger. The situation is similar for digital payments. As a financial group, we are doing everything we can to stay one step ahead of criminals through new cryptographic procedures, hardened systems and so on. It is not without reason that our experts are already working on cryptographic solutions that will be able to withstand the coming era of quantum computers. The challenge here is to maintain the convenience for the customers.

Jochen Werne: By its very nature, cash is without doubt the most robust payment method. This is regularly demonstrated in extreme scenarios such as disasters, failure of a digital infrastructure due to cyber attacks, natural disasters or technical failure. Cash is not tied to electricity, digital infrastructure, passwords or other technical features. In addition, the introduction of the second series of euro banknotes has enhanced security features and made banknotes more secure and more counterfeit-proof. As the Bundesbank reported at the beginning of the year, the number of counterfeit banknotes has fallen by a further five percent. With digital payment methods, consumers themselves have a responsibility to protect themselves. At the beginning of the Corona crisis, for example, the payment limit for contactless payments, such as in supermarkets, was increased. At first glance, this sounds harmless. But as a result, anyone can use a card – and it does not have to be their own – to pay for higher-priced goods without further security checks, such as by entering a PIN. And as far as data protection is concerned: with every cashless payment, consumers disclose personal information. Data that many companies use commercially.

Dr Harald Olschok: The risk of coming into contact with counterfeit money in Germany is still low. Most counterfeits are easy to detect. The security features of the current Euro series make it difficult for criminals. However, if digital payment methods are attacked, consumers should be aware that they lose much more than just their money.

China wants to take a step in this direction from 2021 onward at the state level as well. The aim is to link the Alipay payment solution with all private and state databases, including those in which cashless payment transactions are stored. The aim is to record and evaluate consumer behaviour. Subsequently, either rewards are offered or sanctions are threatened. Anyone who accumulates too much debt or fails to pay it back is no longer allowed to use express trains or planes in China. Although such a development is completely out of the question in European democracies in the foreseeable future, do you also expect consumer behaviour to play a much greater role in credit rating in the future?

Jochen Werne: Harvard history professor Niall Ferguson coined the term “new cold war” over a year ago. This “Cold War” is mainly about one technology leadership in artificial intelligence and takes place between the United States and China. Technologies are not good or bad, but how and for what purpose they are used by us humans, determines the outcome. Just because something is now technically possible, it does not necessarily make sense for a society. It is a great value of liberal democracies that these issues are discussed, that privacy is protected and that the state cannot act on its own authority.

On the question of creditworthiness, it can be said that the better a credit institution knows the borrower, the better a risk assessment can be made in order to quantify credit default risks. When assessing creditworthiness, the institution is required to use all relevant and available data for the decision. Today, it is technically possible to enrich the data provided by the future borrower with information about him/her from the Internet and social media and to round off the data with the help of AI algorithms and peer group comparisons. However, there is a high risk that private personal data may be processed here if inadvertently and the protection of privacy may be violated. This must be prevented. However, it remains to be seen how this will be dealt with in the future.

Leif Wienecke: First and foremost, it is a matter of making sensible use of the many possibilities of generated data to create added value. Companies such as banks primarily face the challenge of preparing their customers’ data in a meaningful way and integrating it for new applications. The ecosystems of the “GAFAs” or Alipay are “data first” companies which are integrated into the everyday life of their users. In principle, they only make decisions based on data and empirical findings. The above description from China, however, does not go hand in hand with our understanding of data or consumer protection, so we do not see this coming either.

On the other hand, it is of course essential to pursue data-driven innovation. Even the credit rating system that exists today can certainly be extended via relevant, contextual data points, in the interests of consumers and credit institutions. The topic of “social scoring”, i.e. the use of customer data from social networks, is controversial in Germany and is discussed above all in the context of consumer protection. This is correct, because the consumer should not only have to give his consent for such scoring, but should also be able to understand the algorithm and complain in case of discrimination.

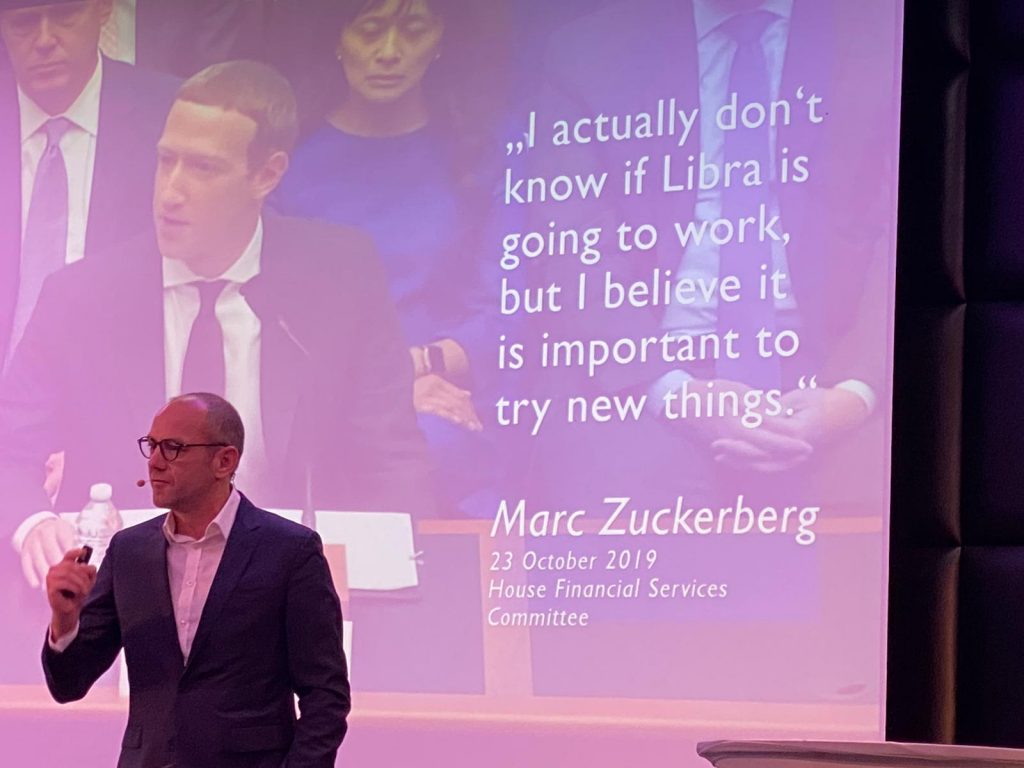

Recently, initiatives have been heard repeatedly to make a CBDC (Central Bank Digital Currency) accessible to all citizens and not to limit an e-euro to institutional participants in the financial markets. What do you think about this?

Leif Wienecke: The CBDC issue is still in its infancy and has many facets. It is mostly about increasing the efficiency of payment transactions. End customers also benefit from this. In principle, innovation processes and initiatives to transform the financial industry are to be seen as positive. As with all topics with a European or international scope, it is important to create a uniform regulatory framework. Precisely because the introduction of a digital central bank currency for the public would not be accompanied by a change in the existing monetary system. At Solarisbank, we have been dealing with the block chain and crypto currency industry for over two years. Last year, we founded the subsidiary Solaris Digital Assets to realise our vision of the broad use of digital assets.

Ralf-Christoph Arnoldt: Unfortunately, very different things are mixed up here. Firstly, there is the technology on which most crypto currencies are based: the block chain. It is highly interesting because rights (to money, benefits from contracts, etc.) can be transferred securely and traceably. This technology has its use cases and will increase in importance. To issue a currency based on this digital solution is certainly forward-looking but not without risks. The speed with which sums of money can be transferred would in itself increase the speed at which money circulates to an extent at which we lack economic experience. Questions also remain to be answered about the security of the currency and who is responsible for the counter-value. It is therefore to be welcomed that we are dealing with this issue at an early stage so that we can learn with manageable and calculated risk.

The concept of the euro, on the other hand, suggests a digital currency as a means of payment. In my view, it is still too early for that. Not only because the overall economic effects can only be estimated to a limited extent at present, but also because this technology is geared to the security and distribution of data, not to transaction efficiency. The number of transactions is technically limited. There are concepts such as the Lightning technology to circumvent this and allow more transactions. However, the latter again functions as an intermediary according to principles similar to those of traditional payment transactions. Transactions are executed and then “booked” in the block chain – similar to a central bank transfer.

Likewise, too little attention is paid to the ecological aspect. According to estimates, Bitcoin alone consumed around 74 terawatt hours in one month at the end of 2019. By way of comparison, Germany’s total electricity consumption over the same period was around 47 terawatt hours.

And now the crucial question at the end: How do you make cashless payments?

Ralf-Christoph Arnoldt: With the Girocard – as far as possible contactless of course, and with pleasure also by mobile phone.

Leif Wienecke: I use Google Pay with my debit cards from our partners Tomorrow, Vivid Money and Bitwala. Offline I use the corresponding Visa cards. And online I also use PayPal.

Jochen Werne: Of course with cash and cashless.

Dr. Harald Olschok: In food retailing and gastronomy regularly with cash. For larger expenses, including refuelling, with credit cards.