HOT OFF THE TAPE: Business Transformation in the Digital Age – Insight into Practice from an Expert’s Perspective

It was a great pleasure being invited as guest to the brand new podcast format POLEDIFY. With Poledify, Felix Gehm offers insights into the routines, mindsets and habits of experts and thought leaders from a wide range of disciplines.

Jochen Werne is Chief Development Officer and Chief Visionary Officer of Prosegur Germany. Prosegur Group is one of the leading security service providers worldwide with over 175,000 employees on five continents. Jochen Werne is, among other things, a member of the Learning Systems Platform, which advises the German government on artificial intelligence, and of the Royal Institute of International Affairs Chatham House, one of the most important think tanks in the world. Jochen was listed as one of the AI experts in Germany by Focus magazine. He is also an author, keynote speaker, internationally awarded NGO founder and specialist in business development and transformation, and international diplomacy. In 2020, the Tyto Tech Power List named him one of the 50 most influential people in the tech scene in Germany.

Topics of this episode:

What does digital transformation mean for “traditional” business sectors? How Prosegur plans to master digital transformation How not to be deterred by big challenges The most important characteristics of a leader in the face of such challenges

Links and other things from the episode: The interview between Bill Gates and Warren Buffet: shorturl.at/mGPYZ Books: Utopias for Realists by Rutger Bregman Mordern Monopolies by Alex Moazed and Nicholas L. Johnson Here you can find Jochen Werne and everything about Prosegur: Jochen Werne LinkedIn: https://www.linkedin.com/in/jochenwerne/ Jochen Werne Website: http://jochenwerne.com/ Prosegur LinkedIn: https://www.linkedin.com/company/prosegur/ Prosegur website: https://www.prosegur.com/en/jobs Platform Learning Systems: https://www.plattform-lernende-systeme.de/home-en.html

Questions, criticism, suggestions or anything else? Write to me! Instagram: https://www.instagram.com/poledify/ Twitter: https://twitter.com/ThisIsFelixGehm or simply send an email to poledify@gmail.com Where does the fine music (intro & outro) come from? The fine music in the intro and outro is produced by pads. Behind the artist name is Patrick, who has finally decided to record all his little songs. You can find it all here: YouTube: bit.ly/33TOFcN Instagram: https://bit.ly/2XWFDIm Soundcloud: https://bit.ly/3oYQA8k

It is an honour to be able to support this forward-looking Data Literacy Charter, initiated by the Stifterverband, as a first signatory together with the most competent representatives from politics, education, business and science.

Jochen Werne

DATA LITERACY CHARTA

Find all original information in German > HERE / please find below a translation for English speaking audience – created with DeepL.com

The Data Literacy Charter, initiated by the Stifterverband in January 2021 and supported by numerous professional societies, formulates a common understanding of data literacy and its importance for educational processes. The charter is in line with the Federal Government’s data strategy and with the Berlin Declaration on the Digital Society.

Author and authors: Katharina Schüller, Henning Koch, Florian Rampelt

SUMMARY Data literacy encompasses the data skills that are important for all people in a world shaped by digitalisation. It is an indispensable part of general education.

With the Data Literacy Charter, the signatories express the common understanding of data literacy in the sense of comprehensive data literacy and its importance in educational processes. This understanding is in line with the Federal Government’s data strategy and with the Berlin Declaration on the Digital Society.

Data literacy includes the skills to collect, manage, evaluate and apply data in a critical way. If data is to support decision-making processes, it needs competent answers to four fundamental questions:

What do I want to do with data? Data and data analysis are not an end in themselves, but serve a concrete application in the real world. What can I do with data? Data sources and their quality as well as the state of technical and methodological developments open up possibilities and set limits. What am I allowed to do with data? All legal rules of data use (e.g. data protection, copyrights and licensing issues) must always be considered. What should I do with data? Because data is a valuable resource, a normative claim derives from it to use it for the benefit of individuals and society. The supporters of the Charter see data literacy as a central competence of all people in the 21st century. It is the key to systematically transforming data into knowledge.

Data literacy enables people, businesses and scientific institutions, as well as governmental or civil society organisations,

to actively participate in the opportunities offered by data use; deal confidently and responsibly with their own and other people’s data; to use new drivers and technologies such as Big Data, Artificial Intelligence or Internet of Things to meet individual needs, address societal challenges and solve global problems. Data literacy strengthens judgement, self-determination and a sense of responsibility and promotes the social and economic participation of all of us in a world shaped by digitalisation.

GUIDING PRINCIPLES Five principles characterise the importance and role of data literacy as a key competence of the 21st century.

Data literacy must be accessible to all. Data literacy serves to promote maturity in a modern digitalised world and is therefore important for all people – not only for specialists. The aim of teaching data literacy is to ensure that each individual and our society as a whole deal with data in a conscious and ethically sound manner. Data literacy enables successful and sustainable action that is based on evidence and that takes appropriate account of uncertainty and change in our living environment. We are therefore committed to ensuring that data literacy is taught broadly and can be acquired by all people.

Data literacy must be taught throughout life in all areas of education. Data literacy must be anchored in all formal and non-formal education sectors and thus established as part of general education. To do this, we must continuously teach learners how data relates to their respective lifeworlds: Data are digital images of real phenomena, objects and processes – this applies to all fields of application. How to collect or procure, evaluate, apply and interpret data appropriately for the respective application must be systematically learned and practised. The basic concept of data literacy and its sub-areas therefore applies across the board, even if the level of competence imparted varies depending on the educational sector and level. In concrete terms, this requires the inclusion of data literacy in the curricula and educational standards of schools, in the curricula of degree programmes and in teacher training programmes. Learners should not only be addressed as passive consumers of data. Rather, we want to enable them to actively shape data-related knowledge and decision-making. In order to make lifelong learning of data literacy possible, data literacy programmes for extracurricular and vocational training are also needed. We advocate developing and promoting these, for example, together with adult education centres or public libraries.

Data literacy must be taught as a transdisciplinary competence from three perspectives. Data literacy involves three perspectives: the application-related (“What is to be done?”), the technical-methodical (“How is it to be done?”) and the social-cultural (“What is it to be done for?”). We therefore want to ensure that data literacy is taught from a trans- and interdisciplinary approach. This includes ● the application-oriented perspective (for example, applications from the natural and engineering sciences, economics, medicine, psychology, sociology, linguistics, media studies and many more), the technical-methodological perspective (for example, from the perspective of statistics, mathematics, computer science and information science), the socio-cultural perspective (for example, reflection on legal, ethnological, ethical, philosophical as well as inequality aspects) ● as well as the perspective of teaching (for example on the part of subject didactics and educational science).

Data literacy must systematically cover the entire process of knowledge and decision-making with data. Data literacy ensures that answers to real problems are found with the help of data in a structured and qualitative way. Data literacy therefore includes the following areas of competence: ● Using and protecting data (ability and motivation to responsibly acquire, analyse, share and obtain appropriate data and information in the context of the task at hand). Classify data and information derived from it (ability and motivation to contextualise and interpret data and information and to critically question learning systems, such as AI applications). ● Act in a data-supported manner (open-minded attitude towards data in the sense of a data culture including insight into the role of data for evidence-based action, ability to handle data with confidence including effective communication of data-based decisions).

Data literacy must comprise knowledge, skills and values for a conscious and ethically sound handling of data. Data literacy comprises three competence dimensions that must be mapped in all three competence areas. Each competence area is characterised by ● specific knowledge (dimension “Knowledge”), ● the skills and abilities to apply this knowledge (dimension “Skills”) and ● by the willingness to do so, i.e. the corresponding value attitude (dimension “Values”). Data ethics is a central component of a key competence and is reflected in all sub-areas of data literacy. This means that when data is collected, managed, evaluated and used in a critical way, ethical aspects play an important role throughout. Data ethics and values contribute significantly to ensuring that not only the right means are used to solve problems with the help of data, but above all that the right goals are pursued: Data should make a sustainable positive contribution to society and therefore be used responsibly, context-sensitively and with a view to possible future consequences.

The signatories of the Data Literacy Charter will take measures to disseminate this understanding of data literacy and to further strengthen the associated competences. They call on other actors to do the same in their sphere of influence.

The initial signatories Institutions & Initiatives (in alphabetical order)

Bund Katholischer Unternehmer e.V. (BKU)

Deutsche Arbeitsgemeinschaft Statistik (DAGStat) mit ihren 14 Mitgliedsgesellschaften und dem Statistischen Bundesamt Destatis

Deutscher Volkshochschul-Verband (DVV)

Deutsche Statistische Gesellschaft (DStatG)

Digitalrat der Bundesregierung

Europäisches Wirtschaftsforum e.V. – EWiF Deutschland

Federation of European National Statistical Societies (FENStatS) mit ihren 27 Mitgliedsgesellschaften und der Europäischen Zentralbank

FernUniversität in Hagen

FOM Hochschule für Oekonomie & Management

Hochschulforum Digitalisierung

Initiative for Applied Artificial Intelligence by UnternehmerTUM

Institute of Electrical and Electronics Engineers (IEEE), European Office

International Association for Statistical Education (IASE)

KI Bundesverband e.V.

KI-Campus – Die Lernplattform für Künstliche Intelligenz

Partnership in Statistics for the Development in the 21st Century (PARIS21) / OECD

RWI – Leibniz-Institut für Wirtschaftsforschung

Stifterverband

Technische Universität Dortmund

Weltethos-Institut | An-Institut der Universität Tübingen

Individuals (in alphabetical order)

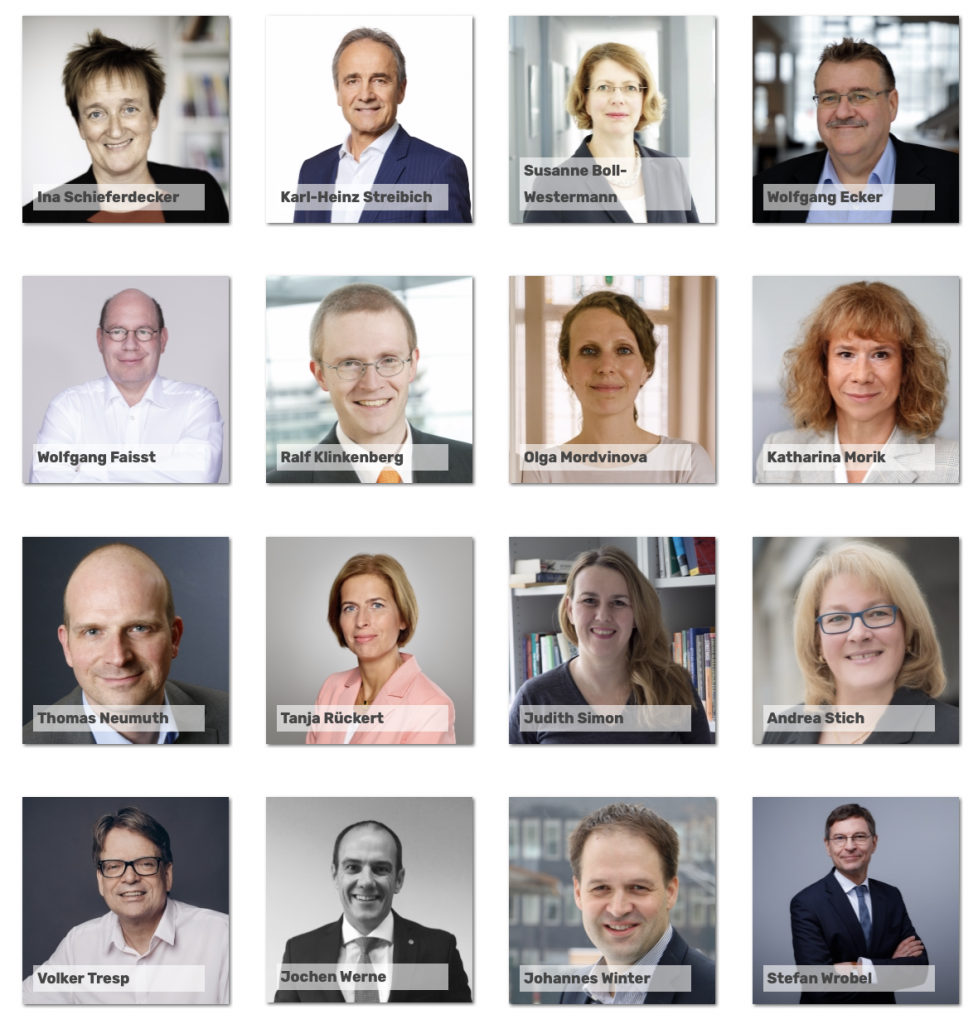

Regina Ammicht Quinn, Dorothee Bär, Thomas K. Bauer, Manfred Bayer, Jörg Bienert, Felicitas Birkner, Vanessa Cann, Thomas M. Deserno, Roman Dumitrescu, Johanna Ebeling, Florian Ertz, Andrea Frank, Gerd Gigerenzer, Jessica Heesen, Ulrich Hemel, Norbert Henze, Burghard Hermeier, Wolfgang Heubisch, Oliver Janoschka, Johannes Jütting, Claudia Kirch, Volker Knittel, Henning Koch, Ralf Klinkenberg, Annegret Kramp-Karrenbauer, Alexander Knoth, Beate M. Kreiner, Sebastian Kuhn, Monique Lehky Hagen, Andreas Lenz, Andreas Liebl, Anna Masser, Volker Meyer-Guckel, Antje Michel, Ralf Münnich, Dominic Orr, Ada Pellert, Martin Rabanus, Walter J. Radermacher, Philipp Ramin, Florian Rampelt, Richard K. Frhr. v. Rheinbaben, Peter Rost, Philipp Schlunder, Harald Schöning, Katharina Schüller, Rainer Schwabe, Andrea Stich, Sascha Stowasser, Renata Suter, Georges-Simon Ulrich, Daniel Vorgrimler, Jochen Werne, Johannes Winter

The hallmark of an open society is that it promotes the unleashing of people’s critical faculties, and the Data Literacy Charter, in this best sense, promotes the much-needed creation of data literacy for all areas of our digital society

“The severe pandemic brought pain and hardship to all our lives and many of our efforts to support international understanding through international diplomacy had to step back to the important goal of not putting lives in danger. Who could understand this better than seafarers.

But now there is light at the end of the tunnel…dawn on the horizon. And even if we cannot all meet on the same boat and on the same ocean yet, we want to announce a very special challenge with GOST’s 2021 Expedition UNITED OCEANS – of course in compliance with all COVID-related regulations.

In June, GOST members from around the world will meet on different oceans with different yachts for Expedition UNITED OCEANS. While this time the current of the salt water will unite us, we celebrate the freedom of the seas and the friendship that knows no boundaries.”

Jochen Werne Co-Founder Global Offshore Sailing Team

Video cut from different Global Offshore Sailing Team expeditions. Voice: John F. Kennedy. Speech at the Admirals Cup Dinner 1962. Video prepared with Splice. ————-

“EXPEDITION UNITED OCEANS”

Del 29 de Mayo al 5 de Junio de 2021.

“Una grave pandemia nos ha traído dolor y dificultades a nuestra existencia. Muchos de nuestros esfuerzos para apoyar un acercamiento internacional a través de la diplomacia, se han visto frenados, en un esfuerzo de no poner en peligro vidas humanas. No obstante, en estos momentos en que se aprecia una luz al final del túnel, así como un nuevo amanecer en el horizonte, y aunque aún todavía no podemos reunirnos todos en el océano, queremos anunciar un nuevo y especial desafío de Global Offshore Sailing Team GOST para este año 2021; se trata de la realización de la EXPEDICIÓN UNITED OCEANS, cumpliendo, por supuesto, con todas las regulaciones y protocolos relacionadas con el COVID19. En estas mismas fechas, los miembros de GOST de todo el mundo se reunirán en diferentes océanos con diferentes yates, que navegarán apoyando la “Expedition United Oceans”. Esta vez y simbólicamente, serán las corrientes oceánicas las que nos una para celebrar la libertad de los mares y la amistad que no conoce de fronteras”.

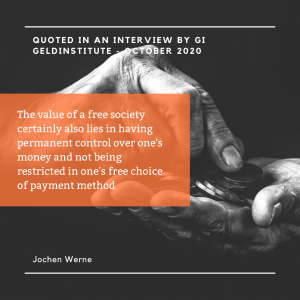

Does cash have a future? An article by Dunja Koelwel, editor in chief of gi Geldinstitute | 20.10.2020 – 13:02

Please follow this LINK for the original source in German. Translation made by DeepL.com

Cashless payment is on the advance worldwide, only the Germans hang on to cash. gi Geldinstitute therefore wanted to know from Ralf-Christoph Arnoldt (Bundesverband der Deutschen Volksbanken und Raiffeisenbanken BVR), Jochen Werne (Prosegur Germany), Dr. Harald Olschok (BDSW) and Leif Wienecke (Solarisbank) Does cash still have a future?

Signs such as “Cash only” should be a thing of the past in Germany, according to the digital association Bitkom. Wherever customers can pay, at least one digital payment option that can be used throughout Europe should be offered on a mandatory basis, according to the “Bitkom theses on freedom of choice in payment”.

“Cash shows itself to be an anchor of trust in uncertain times. With increasing concern about the corona virus, the amount of physical cash in circulation in the USA, for example, has risen,” says Jochen Werne, member of the management of Prosegur Cash Services Germany. gi geldinstitute therefore asked: What is the current situation regarding ‘war on cash’?

Since the Corona crisis, more and more people have been paying with cards or smartphones instead of with coins or notes. Is this a trend that is slowly eliminating cash? What is your perception?

Ralf-Christoph Arnoldt: Indeed, in recent months we have seen gains in card payments, especially in payments with Girocard. In the first half of 2020, transaction figures have increased by 20.7 percent compared to the same period last year. However, cash still plays an important role in everyday life in Germany, even if this love is eroding.

According to the Eurohandelsinstitut (EHI), the share of cash in turnover in 2019 was still 45.5 percent. Cash offers some advantages from the customer’s point of view. Paying with cash is convenient for the customer, anonymous, immediately final. Cash is freedom for customers. Regulators and business circles involved in the cash circle should accept this as a fact and not force them to change it.

Dr. Harald Olschok: Without doubt, a new phase of “war on cash” began during the Corona crisis. 75 percent of the member companies of the BDGW expect sales next year to be up to 20 percent lower than in the past. We assume that the proportion of cash payments in the retail sector will fall from around 48 percent at the beginning of 2020 to well below 40 percent. However, the crisis has also shown that Germans continue to have great confidence in cash as a secure means of payment and store of value. According to a survey by YouGov, Germans also cannot imagine living in a cashless society.

Leif Wienecke: Since the Corona crisis, we have seen an acceleration of many trend developments, some of which were already foreseeable before. This also includes contactless payment. This customer behaviour, which is relatively new in Germany, fits in well with corona-related hygiene measures. Basically, it can be said that, in addition to hygiene considerations, end customers are primarily looking for speed when choosing a means of payment. This is where digital and contactless payment methods come into play. Over the next few years, we will see a further decline in cash payments and an increasing use of digital payment methods such as mobile wallets.

Jochen Werne: What is important to people when it comes to their money – the “fruits of their labour”? Certainly its unlimited availability. If they can have confidence that they can get their money at any time, people choose the payment option that is most convenient for each individual. Some prefer to pay by smartphone, while for others it’s “only cash is true”. It is fundamental that we as consumers are free to decide from which means of payment we can freely choose. Freedom of choice is the key word.

A “per cash” argument often made is that technology is vulnerable and that in a crisis the value of security is always the highest good. This is why many people have been hoarding cash at the beginning of the lockdown. Do you believe that this money will now come back into circulation? And what do you think about the technological error potential of digital payment options?

Ralf-Christoph Arnoldt: The fact that cash was hoarded at the beginning of the lockdown was more due to the fact that people thought the cash supply could be endangered because of the Corona crisis. But that quickly proved to be incorrect. In the meantime, the hoardings have been continuously disbanded. We can see this, among other things, in the fact that the payout volumes at ATMs are still about 25 percent below the pre-corona level. If you want to compare the security of cash with card payments or digital payment options, you don’t get very far. If cash is stolen, for example, it is gone for good. If a payment card is stolen, the bank is usually liable.

Jochen Werne: It is undeniable that cash is seen by many as an anchor of trust in uncertain times. Electronic payment methods always risk a loss of trust due to technical failures. One of the last of these incidents was not long ago: during the pre-Christmas business on 23 December 2019, of all days, EC card payments were not accepted at many terminals. Many consumers who rely solely on digital payments have probably already had similar experiences of lesser consequence. Such situations can be observed time and again at the cash desks in department shops and supermarkets – for example, when the NFC chip on a card or simply the card reader does not work. Soon the eyes of the people standing around in the shopping queue turn to the payer, impatient and interested, trying to find out the name on the card of the supposedly insolvent unlucky person. Nevertheless, modern technologies are becoming more and more stable over time and a balance will be established between the various payment methods. Just as the “hoarded” will be returned to consumption or investment after the crisis. A cycle that, soberly, has always existed historically.

It became apparent that banks would no longer be able to offer free cash withdrawals from ATMs in the long term. This affects in particular people on low incomes, the elderly and, in general, all those who do not have access to digital forms of payment. Which solution do you think makes the most sense?

Leif Wienecke: Indeed, an accelerated dismantling of bank branches has been observed in recent months, but also before. The cost-benefit ratios seem to be out of proportion. Many end customers, especially older people, are suffering as a result. At the same time, however, one can also read about the creative solutions that savings banks, for example, are using to offer customers in rural areas the service they are used to (e.g. branch on wheels, transfer bus). I believe that other companies will fill the gap left by the banks. For some years now, supermarkets and petrol stations, for example, have been offering free “withdrawal” of cash. This trend to integrate banking services into the context of everyday life is known as contextual banking. The end customer wants to have access to cash or transactions wherever he or she is. As Solarisbank, we see the future in banking here.

Jochen Werne: Making an individual’s assets available as cash causes costs, just as paying with a card costs consumers money. The latest evaluation of 294 account models of 125 credit institutions in Germany by Stiftung Warentest shows that 55 models already charge fees for payment with the Girocard. It is the task of the institutions not only to manage their customers’ money, but also to meet the customer’s wish to make these assets available to them again in the form of cash or book money. The current practice of offering cash or accounts without fees and cross-subsidising them in return is a German phenomenon. The former head of BaFin, Dr. Elke König, already raised the question critically more than five years ago at the “Bank of the Future” event.

Today’s pressure on margins at banks now demands this adjustment. It is undisputed that, according to the German Bundesbank, ATMs are the most popular source of cash, accounting for 84 per cent of all cash withdrawals. Their number has risen by a good 18 per cent in Germany in recent years. On average, there is one ATM per 1,415 inhabitants. ATMs are therefore of enormous social and economic importance. It is not surprising that the area of “cash supply” is expressly listed as a “critical service” in Section 7 of the Critical Service Ordinance of the Federal Office for Information Security (BSI-KritisV), as a “service for the supply of the general public (…), the failure or impairment of which would lead to considerable supply bottlenecks or to threats to public security”. The fact that banks have to provide cash and cards to their customers, but are generally not able to do so profitably without charging is a long-term problem and needs to be improved. However, there is room for debate as to whether charges are the right way forward for consumers.

For US economics professor Kenneth Rogoff, the abolition of large banknotes is a first step. According to Rogoff, cash is synonymous with crime and the shadow economy – and in this respect it is a threat to the general public. Is cash really more “crime-sensitive” than digital payment methods?

Dr. Harald Olschok: As a “learned” Freiburg economist, I am always appalled by the populist and simplistic theses of the former chief economist of the IMF. It is much worse than you suggest. For Rogoff, “there is no question that cash plays a vital role in criminal activities, including drug trafficking, organised crime, extortion, corruption of authorities, trafficking in human beings and money laundering. (Der Fluch des Geldes, Munich 2016, p. 11). Oh yes, and undeclared work and illegal immigration are also owed to cash. Unfortunately, it has also been heard in the euro area. The 500 euro banknote has already been abolished. At the heart of the Rogoffian theses is the abolition of cash in order to impose negative interest rates. People should not save, but spend their money. This ignores the fact that fraud with non-cash means of payment, such as crypto-currencies, is booming. I expect that these forms of fraud will continue to increase. We must therefore assume the opposite.

Ralf-Christoph Arnoldt: Passing on a USB stick with millions of dollars in crypto-currencies, for example, is as easy as passing on a banknote. Criminals and the black economy are also part of the trend towards digitalisation, unfortunately sometimes even ahead of the investigating authorities.

Leif Wienecke: There is a lot of discussion on this topic and also conflicting studies. The Federal Government’s decision to tighten the reporting requirements for notaries, for example in real estate transactions, underlines Rogoff’s thesis. Nevertheless, I believe that it is not possible to generalise. Certainly, the anonymity of cash brings some advantages for criminals and money laundering can be curbed by switching to more strongly regulated, digital payment procedures.

And what about security? With cash, the problem is counterfeiting, with digital payments, for example, the tapping of identities and data. What is easier to protect?

Ralf-Christoph Arnoldt: I don’t see a big difference. It is always a mutual arms race. New security features for cash require more know-how and greater investment for counterfeiters. It is becoming more difficult, the number of offenders is getting smaller, but the sums that a counterfeiter puts on the market are bigger. The situation is similar for digital payments. As a financial group, we are doing everything we can to stay one step ahead of criminals through new cryptographic procedures, hardened systems and so on. It is not without reason that our experts are already working on cryptographic solutions that will be able to withstand the coming era of quantum computers. The challenge here is to maintain the convenience for the customers.

Jochen Werne: By its very nature, cash is without doubt the most robust payment method. This is regularly demonstrated in extreme scenarios such as disasters, failure of a digital infrastructure due to cyber attacks, natural disasters or technical failure. Cash is not tied to electricity, digital infrastructure, passwords or other technical features. In addition, the introduction of the second series of euro banknotes has enhanced security features and made banknotes more secure and more counterfeit-proof. As the Bundesbank reported at the beginning of the year, the number of counterfeit banknotes has fallen by a further five percent. With digital payment methods, consumers themselves have a responsibility to protect themselves. At the beginning of the Corona crisis, for example, the payment limit for contactless payments, such as in supermarkets, was increased. At first glance, this sounds harmless. But as a result, anyone can use a card – and it does not have to be their own – to pay for higher-priced goods without further security checks, such as by entering a PIN. And as far as data protection is concerned: with every cashless payment, consumers disclose personal information. Data that many companies use commercially.

Dr Harald Olschok: The risk of coming into contact with counterfeit money in Germany is still low. Most counterfeits are easy to detect. The security features of the current Euro series make it difficult for criminals. However, if digital payment methods are attacked, consumers should be aware that they lose much more than just their money.

China wants to take a step in this direction from 2021 onward at the state level as well. The aim is to link the Alipay payment solution with all private and state databases, including those in which cashless payment transactions are stored. The aim is to record and evaluate consumer behaviour. Subsequently, either rewards are offered or sanctions are threatened. Anyone who accumulates too much debt or fails to pay it back is no longer allowed to use express trains or planes in China. Although such a development is completely out of the question in European democracies in the foreseeable future, do you also expect consumer behaviour to play a much greater role in credit rating in the future?

Jochen Werne: Harvard history professor Niall Ferguson coined the term “new cold war” over a year ago. This “Cold War” is mainly about one technology leadership in artificial intelligence and takes place between the United States and China. Technologies are not good or bad, but how and for what purpose they are used by us humans, determines the outcome. Just because something is now technically possible, it does not necessarily make sense for a society. It is a great value of liberal democracies that these issues are discussed, that privacy is protected and that the state cannot act on its own authority.

On the question of creditworthiness, it can be said that the better a credit institution knows the borrower, the better a risk assessment can be made in order to quantify credit default risks. When assessing creditworthiness, the institution is required to use all relevant and available data for the decision. Today, it is technically possible to enrich the data provided by the future borrower with information about him/her from the Internet and social media and to round off the data with the help of AI algorithms and peer group comparisons. However, there is a high risk that private personal data may be processed here if inadvertently and the protection of privacy may be violated. This must be prevented. However, it remains to be seen how this will be dealt with in the future.

Leif Wienecke: First and foremost, it is a matter of making sensible use of the many possibilities of generated data to create added value. Companies such as banks primarily face the challenge of preparing their customers’ data in a meaningful way and integrating it for new applications. The ecosystems of the “GAFAs” or Alipay are “data first” companies which are integrated into the everyday life of their users. In principle, they only make decisions based on data and empirical findings. The above description from China, however, does not go hand in hand with our understanding of data or consumer protection, so we do not see this coming either.

On the other hand, it is of course essential to pursue data-driven innovation. Even the credit rating system that exists today can certainly be extended via relevant, contextual data points, in the interests of consumers and credit institutions. The topic of “social scoring”, i.e. the use of customer data from social networks, is controversial in Germany and is discussed above all in the context of consumer protection. This is correct, because the consumer should not only have to give his consent for such scoring, but should also be able to understand the algorithm and complain in case of discrimination.

Recently, initiatives have been heard repeatedly to make a CBDC (Central Bank Digital Currency) accessible to all citizens and not to limit an e-euro to institutional participants in the financial markets. What do you think about this?

Leif Wienecke: The CBDC issue is still in its infancy and has many facets. It is mostly about increasing the efficiency of payment transactions. End customers also benefit from this. In principle, innovation processes and initiatives to transform the financial industry are to be seen as positive. As with all topics with a European or international scope, it is important to create a uniform regulatory framework. Precisely because the introduction of a digital central bank currency for the public would not be accompanied by a change in the existing monetary system. At Solarisbank, we have been dealing with the block chain and crypto currency industry for over two years. Last year, we founded the subsidiary Solaris Digital Assets to realise our vision of the broad use of digital assets.

Ralf-Christoph Arnoldt: Unfortunately, very different things are mixed up here. Firstly, there is the technology on which most crypto currencies are based: the block chain. It is highly interesting because rights (to money, benefits from contracts, etc.) can be transferred securely and traceably. This technology has its use cases and will increase in importance. To issue a currency based on this digital solution is certainly forward-looking but not without risks. The speed with which sums of money can be transferred would in itself increase the speed at which money circulates to an extent at which we lack economic experience. Questions also remain to be answered about the security of the currency and who is responsible for the counter-value. It is therefore to be welcomed that we are dealing with this issue at an early stage so that we can learn with manageable and calculated risk.

The concept of the euro, on the other hand, suggests a digital currency as a means of payment. In my view, it is still too early for that. Not only because the overall economic effects can only be estimated to a limited extent at present, but also because this technology is geared to the security and distribution of data, not to transaction efficiency. The number of transactions is technically limited. There are concepts such as the Lightning technology to circumvent this and allow more transactions. However, the latter again functions as an intermediary according to principles similar to those of traditional payment transactions. Transactions are executed and then “booked” in the block chain – similar to a central bank transfer.

Likewise, too little attention is paid to the ecological aspect. According to estimates, Bitcoin alone consumed around 74 terawatt hours in one month at the end of 2019. By way of comparison, Germany’s total electricity consumption over the same period was around 47 terawatt hours.

And now the crucial question at the end: How do you make cashless payments?

Ralf-Christoph Arnoldt: With the Girocard – as far as possible contactless of course, and with pleasure also by mobile phone.

Leif Wienecke: I use Google Pay with my debit cards from our partners Tomorrow, Vivid Money and Bitwala. Offline I use the corresponding Visa cards. And online I also use PayPal.

Jochen Werne: Of course with cash and cashless.

Dr. Harald Olschok: In food retailing and gastronomy regularly with cash. For larger expenses, including refuelling, with credit cards.

Bei sorgfältiger Betrachtung unserer Vergangenheit stoßen wir auf eine faszinierend und teilweise schizophren anmutende Menschheitsgeschichte von partiellem Wahnsinn und absoluter Brillanz – nicht nur, wenn es um den Einsatz neuer Technologien geht. Werfen wir einen Blick in einige dieser Geschichten.

1961 HAVANNA, KUBA: Die Welt steht am Rande eines nuklearen Holocaust. Eine Realität entstanden durch die Auswirkungen des kalten Kriegs, politischer Doktrinen, harter Grenzen und nicht zuletzt technologischen Fortschritts. Nur Diplomatie und der reine Instinkt für das Wesen der menschlichen Existenz auf beiden Seiten verhinderten das Schlimmste.

Eine Geschichte, die die prekäre Lage der Welt zu jener Zeit besonders gut widerspiegelt findet sich in dem indirekten Angebot Fidel Castro an die Sowjetunion, „das Problem“ zu lösen und die kommunistische Revolution durch den Abschuss von Atomraketen von kubanischem Boden, zum Sieg zu tragen. Sein Kampfgefährte Che Guevara ging sogar noch einen Schritt weiter, indem er sagte: „Wir sagen, dass wir den Weg der Befreiung beschreiten müssen, auch wenn er Millionen von Atomkriegsopfern kosten kann. Im Kampf auf Leben und Tod zwischen zwei Systemen können wir an nichts anderes denken als an den endgültigen Sieg des Sozialismus oder seinen Untergang als Folge des nuklearen Sieges der imperialistischen Aggression.” 1962 antwortete der ehemalige Erste Sekretär der Kommunistischen Partei der Sowjetunion, Nikita Chruschtschow, in einem Brief an Fidel Castro, dass er mit der Idee nicht einverstanden sei, weil sie unweigerlich zu einem thermonuklearen Krieg führen würde und dass es doch noch eine Welt bräuchte, in die die Revolution getragen werden könnte.

1961 NEW YORK, USA: Im selben Jahr ratifizieren 12 Nationen einen Vertrag zur gemeinsamen Verwaltung eines ganzen Kontinents. Ein Kontinent, der größer ist als die Vereinigten Staaten. Ein Kontinent, der 90% der Süßwasserreserven der Welt beheimatet und für das Klima unseres Planeten von außerordentlicher Bedeutung ist: die Antarktis. Es ist das Jahr, in dem einer der ermutigendsten Verträge der Menschheit unterzeichnet wurde – der Antarktis-Vertrag.

OPEN-SOURCE-KONZEPT: Der Vertrag – beinhaltet mehrere Kapitel zur ausschliesslich friedlichen und wissenschaftlichen Nutzung der Antarktis. Damit einhergehend regelt der Vertrag auch die gemeinschaftliche Nutzung aller Forschungsergebnisse und Daten. Ein Konzept, das für die damalige Zeit revolutionär erschien und das für die Findung von Lösungen für die großen Herausforderungen unserer Zeit – wie Klimawandel oder die effektive Bekämpfung einer Pandemie – von entscheidender Bedeutung sind.

2020 PLANET ERDE. In der Geschichte haben wir oft die positiven wie auch die negativen Auswirkungen auf die Gesellschaft unterschätzt, die von revolutionären Technologien ausgehen. Doch kann Technologie selbst nicht mit den Begriffen gut oder schlecht beurteilt werden. Vielmehr muss beurteilt werden, wie die Gesellschaft diese nutzt. Heute stehen wir wieder am Rande einer solchen gesellschaftlichen Herausforderung.

Wir leben in einer global vernetzten Welt. Technologischer Fortschritt hat Daten zu einer der wichtigsten Ressourcen gemacht. Der Mitbegründer von Twitter, Evan Williams, erklärte in einem Interview der New York Times 2017 überraschenderweise das Folgende: „Ich dachte, wenn alle Menschen frei sprechen und Informationen und Ideen austauschen können, wird die Welt – automatisch – zu einem besserer Ort. Ich habe mich geirrt“.

Man könnte leicht den Eindruck gewinnen, dass dieses Phänomen neu ist, aber Niall Ferguson, Geschichtsprofessor und Senior Fellow des Hoover Institutes ist davon überzeugt, dass der heutige technologische Fortschritt und seine Auswirkungen auf die Gesellschaft mit der Erfindung des Buchdrucks durch Johannes Gutenberg im 15. Jhdt. vergleichbar sind. Die Druckerpresse hatte viele positive Auswirkungen auf den Fortschritt der Menschheit und katapultierte die Bibel 200 Jahre lang auf den ersten Platz der Buch-Bestsellerliste. Leider machte die gleiche Technik “Malleus Maleficarum”, auch bekannt als der „Hexenhammer“, für dieselbe Zeit zur Nummer 2 auf dieser Liste. Das Buch war die Grundlage für die Hexenjagd und brachte so vielen Unschuldigen den Tod. Sicherlich würde man heute die Inhalte des Buches als „Fake News“ bezeichnen.

GEGENWART & DIE WELT VON MORGEN

Wir alle gestalten heute die Welt von morgen, und unser Streben hat bereits zu viel Gutem geführt. Technologie und menschliche Kreativität haben bspw. dazu beigetragen, die Armutsquote weltweit massiv zu senken. In den letzten 25 Jahren wurden hierbei mehr als eine Milliarde Menschen extremer Armut befreit.

Betrachten wir den Moment so kommt man nicht umhin der aktuellen COVID-19-Pandemie einige Zeilen zu widmen. Es ist eine globale Herausforderung und könnte gleichzeitig die nächste Geschichte des menschlicher Brillanz und Wahnsinns sein. Wir werden dank der KI-basierten Analyseelemente enorme Fortschritte in der medizinischen Forschung und bei den Maßnahmen zur Pandemiebekämpfung erleben. Wir werden aber auch Zeugen einer Rezession werden, die historisch gesehen immer ein Element für Populismus und Nationalismus war. All dies in einem Umfeld von Angst und geschlossenen Grenzen. In diesen Situationen, in denen sich viele von hilflos fühlen, ging Wandel immer von fortschrittlichen Denkern aus, die von ihren Ideen überzeugt waren, von Kant über Ghandi bis zu den Vordenkern der heutigen Zeit.

In unserer offenen Gesellschaft und mit Machine- und Deep Learning Technologien in unseren Händen haben wir die Möglichkeit die Welt zu einem besseren Ort zu machen. Wir können in unseren Berufen viel Neues bewegen, und wir können gegen polarisierende Bewegungen und Ungerechtigkeit in jeder Hinsicht aufstehen und uns Gehör verschaffen. Wir können unsere Kreativität und unseren Intellekt einsetzen, um „den Fortschritt des Denkens” zu verteidigen, der schon immer das Ziel hatte, den Menschen von seiner Angst zu befreien“, genau wie es eines der Ziele des Zeitalters der Aufklärung war.

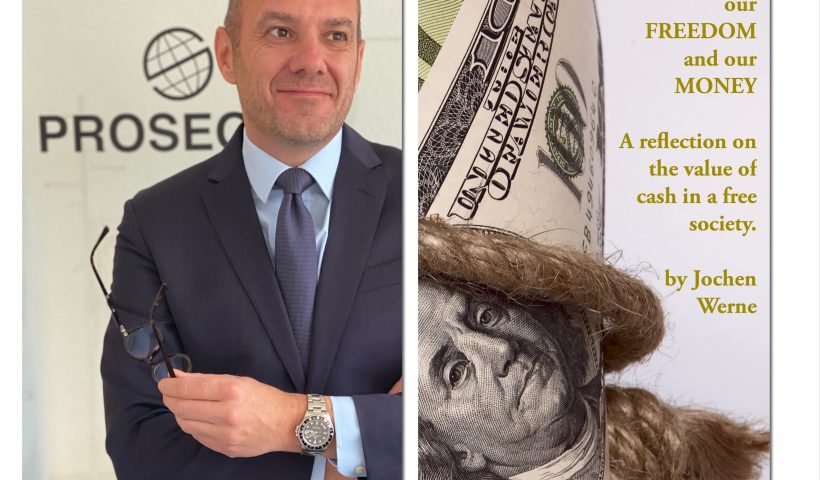

Unlimited availability of our money and its ability to be used as a medium of exchange create certainty and lead to personal freedom. But which payment method is proving to be the most robust in any crisis? A reflection on the value of cash in a free society.

By Jochen Werne, Management Board member, Chief Development & Chief Visionary Officer (CDO/CVO) of Prosegur Cash Services Germany GmbH

In times when our life is being affected significantly by the effects of the situations like the COVID-19 pandemic, we become more aware of the basic needs in our lives. However, the COVID-19 crisis, which hits us globally so hard that we are even prepared to give up some of our civil rights and liberties guaranteed by the constitution, also reveals what certainty means and gives us and what we rely on in order to overcome a crisis and regain our freedom. We live in a world of exponential leaps in technology – and the technological progress has traditionally always resulted in a global improvement in living standards. The international community can be rightly proud of its achievement of reducing the percentage of people who have to live in absolute poverty from 35% to 8% in the last 30 years thanks to global trade. However, it is in times of crisis that we see just how sustainable the goals that have been achieved are. Here prudent and decisive action from political and business leaders is called for. Confidence gained in people and instruments is the greatest asset in times of uncertainty.

Cash: always available

The same applies for payments. While the independent good work over decades of many central banks such as the Deutsche Bundesbank, the European Central Bank and the US Federal Reserve is making itself noticeable in the crisis and the citizens rely on the stability of the euro and US dollar, cash is also showing itself to be an anchor of confidence in uncertain times. With growing concerns due to the coronavirus, in the USA for example the volume of physical cash in circulation has increased. In the week before 25 March this increased by 1.8% to 1.86 trillion dollars in absolute figures. This represents the biggest weekly increase since December 1999, when the fear of the so-called Millennium Bug was the reason for the rise. As we see today, the technological meltdown did not happen. However, 20 years later we are now more aware than ever of the vulnerability of technology and that in times of crisis the value of certainty is always the greatest asset. The increase in demand for cash, including in Germany, at the start of the corona crisis is probably attributable to this legitimate need of citizens for certainty and their great confidence in cash. According to the Bundesbank, the volume on Monday 16 March alone, the first day upon which schools and nurseries were closed, was 0.7 billion euros above the average.

Electronic payment methods, which are essential in so many areas such as online trading for example, repeatedly risk a loss of confidence due to technical failures. One of the most recent of these incidents occurred during of all times the Christmas shopping period on 23 December 2019, when EC card payments were no longer accepted at many terminals. It is a little like the situation described by the Roman poet Ovid: “People are slow to claim confidence in undertakings of magnitude.” Most certainly our savings – the fruit of our labour – are of this magnitude for us. It is for this reason that the availability of our money is so important. If this availability were restricted, we would start to feel that we might no longer be able to access our money, and a bank run would most likely be the result. It is not without reason that the “supply of cash” is expressly defined as a “critical service” in Section 7 of the Regulation on the Identification of Critical Infrastructures (BSI-Kritisverordnung – BSI-KritisV) of the Federal Office for Information Security (BSI). That is to say a “service to supply the general public […], the loss or impairment of which would result in significant supply shortages or risks to public security.”

Certainty in uncertain times

In the COVID-19 crisis, anxiety about health and the economic consequences of any crisis dominate our daily life. While fear is clearly caused by an external threat, anxiety is indeterminate. As the Greek stoic philosopher Epictetus wrote in his Enchiridion of stoic morals: “People are not disturbed by things, but by the view they take of them.” It was therefore also absolutely consistent that the World Health Organization (WHO), the European Central Bank, the Bundesbank and the Robert Koch Institute have been stressing repeatedly in the corona crisis that there is no documented case that would suggest there would be an increased virus risk due to the use of cash as opposed to card payment. They refer here to corresponding scientific studies and underline repeatedly that no information on such a risk has been documented.

Freedom established by the constitution

John Stuart Mill, one of the most successful liberal thinkers of the 19th century, defined freedom as the “first and strongest desire of human nature.” Accordingly, all governmental and social action must be directed towards granting the individual free development, while his freedom, as Mill formulates it in a principle known as the “principle of freedom,” may be limited under one condition: to protect himself or another person. Now, during a serious crisis, all citizens are forgoing some of their fundamental constitutional rights of freedom. This massive intervention is certainly consistent with Mills’ theory in this time of corona. In his novel The House of the Dead, Fyodor Mikhailovich Dostoevsky describes his own experiences of life in a Siberian prison camp and writes the subsequently oft-quoted sentence: “Money is coined liberty,” whereby he describes the vital relevance of a free exchange of goods in an environment where people are deprived of freedom – with cash in the form of coins. Although not in the same way as Dostoevsky, we are also living in a time of extreme change: on a social, economic and political level. We are living in a time when, due to exponential technological developments, whole industries and business models are changing radically and countries are competing for supremacy in areas such as Artificial Intelligence (AI). It is a time in which transformation is the new norm and an agile corporate culture has to be the key to success. It is currently the case in many traditional industries that “anything that can be digitised, will be digitised.” And inevitably this also raises the question of whether this is also the case for the first “instant payment” solution, one of the earliest and longest-lasting achievements of human civilisation – for our cash? Our current free choice of payment method is certainly good, as long as we can choose freely as consumers the payment method appropriate for the respective situation. Discussions about the possible restriction of the freedom of choice of citizens regularly prompt intellectuals to issue warnings. For example, the poet Hans Magnus Enzensberger is of the opinion regarding the issue of “restriction”: “Those who abolish cash, abolish freedom.” This opinion is also shared by Carl-Ludwig Thiele, a former member of the Executive Board of the Deutsche Bundesbank: “Abolishing cash would hurt consumer sovereignty — the free choice of citizens about their payment instruments […] Government agencies do not have the right to tell citizens how they should pay.“

Technological vulnerability, fall-back option and data protection

Particularly in extreme scenarios such as disasters, failures of a digital infrastructure due to cyber attacks, natural events or simply due to technical failure, it is made clear that cash, by its nature, is currently the most robust payment method. The fact that the contactless payment limit has been increased without further ado, for example in supermarkets, at first sounds harmless. However, as a result, anyone can pay for higher-priced goods using a card, and it does not have to be their own card, without any further security checks such as entering a PIN. Everyone has to examine and question critically for themselves the possible consequences of such a payment method. Also not to be disregarded is the issue of data protection. More cashless payments also mean more personal information disclosed by everyone. Data which numerous companies use for commercial purposes. At the latest since the introduction of the EU General Data Protection Regulation (EU GDPR), the sensitivity of the population of Europe with regard to data protection and privacy has been rising gradually. Klaus Müller, Germany’s top consumer protector and Executive Director of the Federation of German Consumer Organisations (vzbv), describes cash as “data protection in practice”. Anyone who pays with cash does not leave any traces to create a consumer profile, purchasing and payment behaviour cannot be manipulated. Cash also helps to protect financial privacy. This was emphasised by Udo Di Fabio, who was a judge of the Federal Constitutional Court for twelve years, at the Cash Symposium 2018 hosted by Deutsche Bundesbank. He explained that every citizen can dispose freely of their money. In his view this freedom would be restricted if financial management were completely digitised.

Smart cash management alleviates the workload of banks

Crises such as the current corona pandemic always bring to light new approaches and act as accelerators of transformation processes that have already been set in motion. With regard to cash-related industries, the banking world has already been in a transformation process for some time. A company such as Prosegur, which, with over 4,000 employees and 31 branches, is a market leader in Germany in the transportation of cash and valuables, is increasingly becoming a full payment-platform provider. Several banks have already taken the path of fully outsourcing their cash management for synergy and cost-saving reasons. Here, cash processes are becoming not only much leaner, but also more cost-effective. This is the case not only for banks, but also for retail customers. With smart machines installed by Prosegur at its customers, cash can be disposed of directly and credited to the customer account on the same day. The smart infrastructure, including dynamic monitoring and forecasting, optimises the logistics and reduces costs in cash logistics. This is the next step towards an efficient, digital and integrated cash management.

Coined Liberty 2.0 and the justification for and rightfulness of cash

In view of the technological progress and the associated social changes, it can be seen that key values from the human perspective are still valid. Based on an intellectual, serious discussion, the relevance to today of the theories of for example Dostoevsky with his experiences in an unfree society is clear: The discussion about the civil rights and liberties of citizens is always very closely related to their ability to use cash freely, to their freedom of choice of payment method and ultimately to the rightfulness of their actions with regards also to effiency and impact. Our open and liberal society is characterised by the fact that we are discussing and most certainly will continue to discuss “Coined Liberty 2.0” at this level.

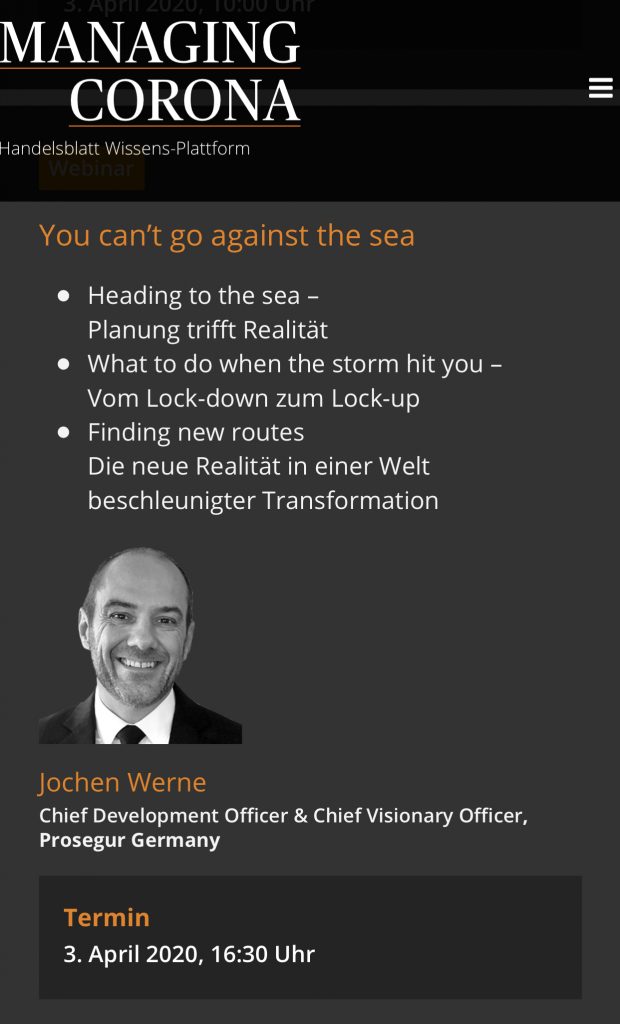

Heading to the sea – Planung trifft Realität What to do when the storm hit you – Vom Lock-down zum Lock-On Finding new routes Die neue Realität in einer Welt beschleunigter Transformation

On Tuesday, November 5, 2019, Managing Director Dr. Stefan Hirschmann and his team from VÖB-Services organised an inspiring BANKENNETZWERK networking event “Digitisation and digital competence in banks” with an auditorium of 70 banking professionals.

Bankennetzwerk am 5.10.2019

im Holiday in Düsseldorf

Digitalisierung und Digitalkompetenz

Foto und Copyright

Bernd Schaller

Kiefernstr. 18

40233 Düsseldorf

www.schallerfoto.de

info@schallerfoto.de

00491776769111

Learning from history is crucial to understand the current societal changes triggered by technological progress. It‘s the basis to be able to make smart strategic decisions in a fundamentally changing business environment.

Some examples in the keynote referring to Professor Niall Ferguson‘s inspiring book „The Square and the Tower“. Enjoy some of his insights here

Bankennetzwerk am 5.10.2019

im Holiday in Düsseldorf

Digitalisierung und Digitalkompetenz

Foto und Copyright

Bernd Schaller

Kiefernstr. 18

40233 Düsseldorf

www.schallerfoto.de

info@schallerfoto.de

00491776769111

The Digital Summit (previously the National IT Summit) and the work that takes place between the summit meetings form the central platform for cooperation between government, business, academia and society as we shape the digital transformation. We can make best use of the opportunities of digitisation for business and society if all the stakeholders work together on this.

The National IT Summit was renamed the Digital Summit in 2017. This was to take account of the fact that digitalisation comprises not only telecommunications technology, but the process of digital change in its entirety – from the cultural and creative industries to Industrie 4.0.

The Digital Summit aims to help Germany to take advantage of the great opportunities offered by artificial intelligence whilst correctly assessing the risks and helping to ensure that human beings stay at the heart of a technically and legally secure and ethically responsible use of AI.

The Digital Summit looks at the key fields of action within the digital transformation across ten topic-based platforms. The platforms and their focus groups are made up of representatives from business, academia and society who, between summit meetings, work together to develop projects, events and initiatives designed to drive digitalisation in business and society forward. The Summit will serve to present the results of the work that has been done in the past, to highlight new trends and discuss digital challenges and policy approaches.

Looking forward moderating the Panel Discussion on “Digital Platforms for new AI-based Services”

Video Stream of Jochen Werne’s keynote at the launch ceremony of the Vietnam Germany Innovation Network (VGI Network).

“It was a great inspiration to meet so many committed people in just one day, ambitious and authentically personally committed, striving for strong intercultural relations between Vietnam and Germany, with the aim of bringing visible benefits to the people of both nations”.

The Data Literacy Charter, initiated by the Stifterverband in January 2021 and supported by numerous professional societies, formulates a common understanding of data literacy and its importance for educational processes. The charter is in line with the Federal Government’s data strategy and with the Berlin Declaration on the Digital Society.

The Data Literacy Charter, initiated by the Stifterverband in January 2021 and supported by numerous professional societies, formulates a common understanding of data literacy and its importance for educational processes. The charter is in line with the Federal Government’s data strategy and with the Berlin Declaration on the Digital Society. With the Data Literacy Charter, the signatories express the common understanding of data literacy in the sense of comprehensive data literacy and its importance in educational processes. This understanding is in line with the Federal Government’s data strategy and with the Berlin Declaration on the Digital Society.

With the Data Literacy Charter, the signatories express the common understanding of data literacy in the sense of comprehensive data literacy and its importance in educational processes. This understanding is in line with the Federal Government’s data strategy and with the Berlin Declaration on the Digital Society.