SECURITY BRIEFING. The battlefields of the past as a lesson for the protection of crypto assets today.

COLD HISTORY. HOT REALITY is a contribution to The Yearbook 2022 “Treasury and Private Banking”, edited by Roland Eller. The book is a well-known platform for building the bridge from the traditional to the new decentralised financial world.

COLD HISTORY. HOT REALITY by Jochen Werne is a plea for openness to new technologies, embedded in a historical-social security briefing on money, power and the indispensable need to protect assets. The battlefields of the past provide the framework for lessons on protecting crypto assets in our technology-dominated world and help us gain a basic understanding of the opportunities and threats in our new cyber reality.

COLD HISTORY – HOT REALITY was particularly inspired by conversations and articles from the following thought leaders, to whom I am deeply indebted.

Raimundo Castilla – CEO Prosegur Custodia Digitales, Ghislain D’Hoop – Ambassador of Belgium to Austria, Slovakia, Slovenia and Bosnia and Herzegovina, Permanent Representative to the United Nations, Roland Eller – Founder and CEO of Roland Eller Consulting, Niall Ferguson – Milbank Family Senior Fellow at the Hoover Institution at Stanford University, Christoph Impekoven – Co-Founder micobo GmbH, Benon Janos – CFO flatexDEGIRO Bank AG, Lior Lamesh – Founder & CEO of GK8, Bernd Lehmann – Historian, Commander of the German Navy (ret.), Rakesh Sharma – Author, Thomas Vartanian – Author and Counselor, Heath White – CEO Prosegur Germany, Johannes Winter – Managing Director of the Platform „Learning Systems“ – Germany‘s AI-platform

Preview and excerpt from Chapter I of “COLD HISTORY – HOT REALITY”

WHAT IS PAST IS PROLOGUE

Impressive and powerful, the words “What is past is prologue” are chiselled in white marble at the foot of the statue in front of the National Archives in Washington D.C.. The famous quote from William Shakespeare’s “The Tempest” is a haunting reminder to everyone that history provides the context for the present.

We live in a present that is changing at breathtaking speed. This fact concerns us daily, but if we do not take the time for a little history lesson, we are doomed to painfully repeat the mistakes of the past. More than aware of this realisation is the former CEO of tech giant Alphabet, Google’s parent company. He dedicated the following note to the New York Times bestseller, “The Square and the Tower: Networks and Power, from the Freemasons to Facebook”: “Niall Ferguson … brilliantly illuminates the great power struggle between networks and hierarchies that rages around the world today. As a software engineer familiar with the theory and practice of networks, I was deeply impressed by the insights of this book. Silicon Valley needed a history lesson and Ferguson delivered.” Not only is Eric Schmidt impressed, but many of the thoughts in this article are inspired by Niall Ferguson’s illuminating papers and lectures.

The beauty of the past is that everything that has already happened, successes and failures, can always be explained in detail and serve as lessons for future challenges. Successful leaders use this knowledge to develop solutions to the problems of the future and to develop communication strategies to make their visions understood by others.

This article was written at a time when humanity is in the final stages of a global pandemic that is saddling countries with an unprecedented debt burden. At the same time, a “New Cold War” is emerging and an arms race for technological supremacy has begun. With new possibilities, the old equilibrium is shaken and a new, albeit familiar, competition for power and money begins. All this at a time when crypto-blockchain-based monetary systems are rapidly becoming a new reality.

The article, with its historical analogies, aims to give the reader a better understanding of how money, power and security are closely intertwined. This helps to put quite complex issues into perspective and gives a clear view of the dangers and opportunities of our changing reality.

The world and change are not to be feared, but understood.

Jochen Werne

The new YEARBOOK will be available in Spring 2022. Find out more HERE

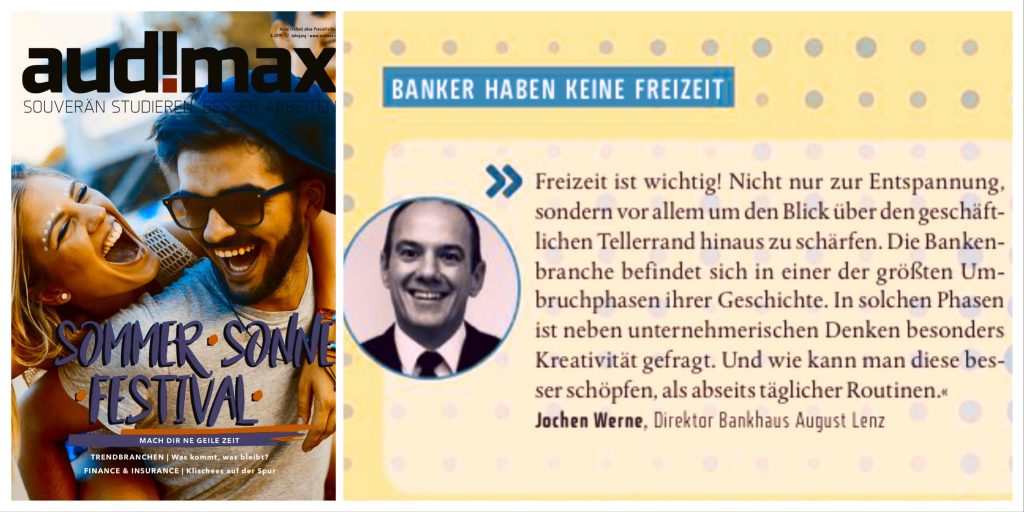

Jochen Werne, Direktor der Bankhaus August Lenz & Co. AG antwortet AudiMax auf die Frage nach dem Klischee, dass Banker keine Freizeit haben. Text: Felix Schmidt / AudiMax

“Freizeit ist wichtig! Nicht nur zur Entspannung, sondern vor allem um den Blick über den Tellerrand hinaus zu schärfen. Die Bankenbranche befindet sich in einer der größten Umbruchphasen ihrer Geschichte. In solchen Phasen ist neben unternehmerischen Denken besonders Kreativität gefragt. Und wie kann man dies besser schöpfen als abseits täglicher Routinen”

There is no lack of buzzwording when it comes to trends in the financial sector: Disruption, FinTech, block chain, crypto. Currently, another term is climbing the zenith of a media hype – platform banking. And not without good reason. “Platform Banking” was voted “Financial Word of the Year” in 2018. Behind this lies the call for banking institutions to open up to third-party providers. Banks and savings banks should not only offer their own services on open platforms, but should also integrate third-party offers and services. Consistently thought through to the end, banks will thus become more intermediaries for all possible services and less providers of their own financial services. The legally necessary prerequisites for such an approach in the strictly regulated financial market have already been set in motion by the adoption of the Payment Services Directive PSD2. Will platform banking become a new hope for the industry, or another risk component in the attempt to lose fewer customers to new technology competitors?

The hype surrounding the topic is understandable: Eight of the ten world’s most valuable companies – Amazon, Google, Microsoft, Apple and Co. – have a platform in their business model. And even more striking: Only one of these companies was already among the top 10 worldwide in 2008. This growth potential, which is the result of the platform expansion, is of course intended by many industries to benefit themselves. The world of finance is also changing rapidly. In recent years, a variety of innovative developments have taken place in the areas of payment transactions and payments. The arrival of third party providers and fintechs has changed the market sustainably and comprehensively. According to a recent whitepaper by Deloitte Consulting, banks will also have to consider a platform strategy in the future: In the future, the customer base will also be able to access products and services from third-party providers in addition to the existing offering. The long-term goal behind this is well known – to retain existing customers, acquire new ones and increase margins.

Platform as recipe for success?

In general, a platform can be seen as a place where supply and demand meet. Economists call such a market – not a new discovery. Due to the digitization of all areas of business and life, geographical boundaries of the marketplaces belong to the past. The result: an almost unlimited number of supply and demand meet on a digital platform – and competition is known to stimulate business. In these business models, the so-called “network effect” ensures that with each new provider on a platform, the incentive for demanders and customers also increases. And in general the more demanders there are on the platform, the more lucrative it becomes for the suppliers. Both sides save enormous search and time efforts and transaction costs are reduced. In short, reflects this the recipe for success behind industry giants such as Amazon, AirBnB, Uber and Co. Nevertheless, there are existing fundamental reservations. The desire of many bank managers to grab a straw in order to grasp a component of hope in a difficult market environment seems understandable. However, blind action is fatal in this situation. Banks must not forget what the emergence of competition in the form of FinTechs has already revealed: frightening weaknesses with regard to their own modern hardware and software solutions, organisation and innovative corporate culture. The fact is that the challenge facing change management is proving to be enormous. And this already now, without having given space to the idea of creating a single platform. The current wave of closing down banking or partnership-based Robo Advisor solutions shows how quickly these carriers of hope can become problems. The commission model behind this, which is always transparent and low priced, is hardly profitable for the banking infrastructure and marginalises the added value that an institution is able to provide for its customers.

The complexity of the changes on all levels, starting with the completely changed, technological possibilities and their effects on the transformation of long-established business models, over the resulting new economic situation of the enterprises are enormous. The difference to the past decades lies in the temporal component. If companies today do not react directly to market changes, they open the way for competitors to their own customers. And this faster than ever before. In such disruptive times, all those involved want an “efficient” change process. However, active, well-considered and vital change management is often criminally neglected. For this one opens door and gate to blind actionism.

The business model of a financial platform is complex, the regulatory framework is strict and the willingness of customers to switch is only slightly visible. For this reason, this business model has so far been too uninteresting for Internet groups. And now, of all things, the banks, often perceived as conservative and unmodern, are to be transformed into digital platforms that can compete with Amazon & Co?

Enormous change management challenge

Banks need a forward-looking and sustainable strategy. That is beyond question. At the latest since the massive “democratization” of the Internet at the end of the 1990s, our lives have been shaped by leaps in technology. In short, the world feels like it is turning faster than ever before. What does this mean for the banks of the 21st century? Anyone who does not understand this exponential dynamic of technical possibilities or does not take them sufficiently into account in his business model can quickly lose touch – with the customers of today and tomorrow. Open banking is both an opportunity and a technological challenge for the banking industry. The European Payment Service Directive 2 – or PSD2 for short – has inevitably made opening up to third parties the focus of the digital strategy.

At the technical level, this is primarily associated with the use of programming interfaces, so-called APIs, which enable both internal and external cost-effective and fast access to data, as well as functions of software applications. What provides the end customer with a cross-product customer experience, means for banks to strategically cooperate with external partners. For FinTechs, cooperation is also advantageous. It creates fast access to customers and their data, as well as to the necessary financial and structural prerequisites.

Anticipating these developments requires a good eye for tomorrow’s customers. After all, customer data is a success driver for future business models. A few years ago, FinTechs began to “poach” their digital offerings among the customer base of traditional institutes. All of this culminated in Robo-Advisors, standardized, computer-controlled asset managers with low fees. It was therefore time for the banks to set sail anew. The plan was to enter into symbioses with FinTechs or “buy” their products directly into their own portfolios. For many large banks, it has become good form to enter into cooperation with small, independent and innovative financial service providers. This is also clearly demonstrated by the current situation of FinTechs. Mergers and co-operation are nothing else than a proof for the fact that the search for sustainable business models is not easy with a fixed idea to solve, not even with the platform strategy. Nevertheless, neither the previous business models nor the product possibilities seem to be mature.

Don’t forget the human factor

The personal relationship, the touchpoint between customer and consultant in the real world, has been increasingly reduced by the acceptance of digital banking. Nevertheless, even if a digital experience is a good thing for a modern bank, consumers continue to appreciate human contact points – especially in economically or politically turbulent times.

The challenge lies in providing the right balance between the digital experience and the traditional, trust based, personal customer relationship.

Jochen Werne

This is precisely the added value that banks can really deliver in this environment today. And this without having to rely on the healing promises of platform banking. Be a guide in the digital jungle and protect customers from ill-considered gut decisions. In addition, it is important to include the customer’s background, apart from monetary issues, in the decision-making process. This usually requires a counterpart. Not a digital one, but a human one. A person of heart and soul who generates trust and can provide a place for personal encounter. Today, it is the customer alone who determines where this is located and what it should look like. The same goes for when this meeting takes place. The modern customer expects the best possible service regardless of space and time, not only in view of the phenomenon of digital gadgets.

At a time of fast pace and constant digital transformation, it is ultimately the Bank’s task to invoke traditional values, ensure humanity and meet the need to be an institution that the client trusts. Perhaps even beyond monetary concerns.