28 February 2021 published in the current issue of the magazine gi Geldinstitute

For the trade magazine gi Geldinstitute, leading experts answered Stefanie Walter’s questions on the topic of “Process Mining at Banks”. Jochen Werne – Prosegur Germany, Gerrit von der Hardt – TARGO Dienstleistungs, Sebastian Hennerici – Aareal Bank AG, Gerrit Meier – Hanseatic Bank GmbH & Co KG, Thorsten Briest – PSD Bank Braunschweig eG, Christian Meusel – Berliner Volksbank eG, André H. Burger – Synpulse Management Consulting

Professional know-how and the right feeling for changing customer needs are essential factors in being able to innovatively develop needs-based solutions for our customers.

The entire roundtable talk in the current print edition or soon online at www.Geldinstitute.de

The Tyto Tech 500 Power List is an objective, data-based survey of various technology sectors in Germany, France and the UK. The study is the first of its kind to measure who has what influence in the tech sector on the basis of various key figures from the online and offline world.

It is a special pleasure to be ranked #35 (Jochen Werne / Prosegur) in the just published Top50-List 2020 of the most influential Germans

DIE 50 EINFLUSSREICHSTEN DEUTSCHEN DER TECH-SZENE

Die Tyto Tech 500 Power List ist eine objektive, datengestützte Untersuchung verschiedener Technologie-Bereiche in Deutschland, Frankreich und dem Vereinigten Königreich. Die Studie ist die erste ihrer Art, die auf Basis verschiedenster Kennzahlen aus der Online- und Offline-Welt misst, wer welchen Einfluss im Tech-Bereich hat.

Es ist eine besondere Freude in der soeben veröffentlichten Top50-Liste 2020 der einflussreichsten Deutschen den Rang #35 (Jochen Werne / Prosegur) zu belegen und dies neben Persönlichkeiten wie (nach Ranking): Sascha Dolling, Jens Pöppelmann, Oliver von Wersch, Sven Bornemann, Sven Stuehmeier, Carol Starr, Bastian Krüger, Norman Wagner, Miriam Thome, Maike Abel, Nico Winkelhaus, Naren Shaam, Robert Jacobi, Ramin Niroumand, Claudia Kemfert, Mallikarjun Rao, Matthias Reinwarth, Ben Shaw, Tessa Niemann, Maren Wulf, Miriam Wohlfarth, Karin Libowitzky, Afseneh Afsaei, Dr. Oliver Vesper, Tim Sievers, Milos Rusic, Felix Falk, Markus Forster, Martin Schmid, Alen Nazarian, Hartmut Giesen, Peter Altmaier, Murat Vurucu, Chris Bartz, Eduard Singer, Alexander Schott, Ritavan ~, Joachim Hensch, Tim Höttges, Dr. Jan Kemper, Andreas Schierenbeck, Hans-Dieter Kettwig, Jost Backhaus, Jens Spahn, Paul Gauselmann und Frank Puscher

1st published in the German newspaper Handelsblatt on January 8, 2020 – translated by DeepL.com. Photos: Pixabay

Looking at the world sometimes gives the impression that things seem to be much better outside Europe. Examples? The world’s largest airport, Beijing-Daxing, goes into operation after four years of construction, while at BER, construction continues after 13 years. The coffee house chain Luckin Coffee, valued at $4.5 billion, will replace Starbucks as No. 1 in the Chinese market by the end of the year, two years after its foundation. Digital platform companies such as Apple, Amazon, Alphabet, Tencent & Co. have left the traditional commodity and industrial groups behind in terms of value.

What made these American and Asian companies so big? Absolute willingness to implement at high speed, massive state and private investments, sometimes industrial policy intervention, huge, scalable domestic markets and a just-do-it mentality favour economic and technological development alongside a number of other factors.

Is Europe, on the other hand, in a downward spiral? Is the continent now losing the much-discussed second half of digitisation, which is mainly about the digitisation of industry, now that the B2C race seems to be lost?

The recent history can also be told in a different way. The financial crisis of 2008/2009 has shown how valuable Europe’s and especially Germany’s strong industrial core is. A highly specialised, excellent SME sector and the leading groups from mechanical, plant and vehicle engineering to the pharmaceutical and chemical industries are anchors of stability. With Industry 4.0, the vision for the future of value creation comes from Germany, and there is a worldwide competition for its widespread introduction.

The strength lies in product innovation, especially in complex products such as machine tools, medical devices, vehicles or building services engineering. Germany also has world market leaders in engineering and in production and automation technology. Despite all the negative predictions, Germany has further expanded its strength in networked physical platforms with the integration of IoT, data and services in industrial environments and has secured a very good starting position. The German research landscape also holds an internationally good position in areas critical to success such as semantic technologies, machine learning and the digital modelling of products and users. And let’s not forget that the companies in the country have produced outstanding software products for the fast, reliable and scalable processing of big data and the integration of business processes.

While Germany wants to consolidate its pioneering position as the world’s supplier, the USA is relying on its expertise as a global networker and China is relying on short decision-making paths, capital intensity and a large domestic market in which it can scale quickly. In this situation, it is important that we concentrate on our strengths and resolutely tackle the digitization of industry and SMEs. However, this requires a much faster entry into the emerging B2B platform markets.

In Europe, we stand for a liberal value system, both economically and politically, which, as in the past, has proven to be the decisive differentiating factor in the medium and long term. The debate on the use of data is conducted in Europe in good tradition at an extremely high level and this in the good understanding that digitisation is not coming over us, but is made by people and is intended to serve them.

It is therefore the right moment to take a decisive step towards the future and to open up Europe’s path. To do this, we need a large, homogeneous domestic market that will make us almost competitive with the USA and China. We also need substantial investment in digital infrastructure and cybersecurity, as well as training and further education. Both competitive regions currently have the power to set standards in digitization as well. The goal of the European Union to create a single digital internal market is laudable, but final implementation is still pending. This implementation, however, is the important and very concrete next step in order to be able to achieve the competition-relevant scaling effects and to be able to play a competitive role in data-based business model innovations.

The second half is running and nothing is lost.

About the authors

Jochen Werne (48) is a member of the Executive Board and Chief Development Officer of Prosegur Cash Services GmbH, as well as a member of the Artificial Intelligence Learning Systems Platform and the Royal Institute of International Affairs, Chatham House.

LinkedIn: https://www.linkedin.com/in/jochen-werne-2292507a/

Twitter: @WerneJochen

E-mail: jw@JochenWerne.com

Dr. Johannes Winter (42) heads the office of the Learning Systems Platform and the technology department at the German Academy of Science and Engineering (acatech).

LinkedIn: https://www.linkedin.com/in/johannes-winter-13048629/

Twitter: @jw4null

e-mail: winter@acatech.de

On Tuesday, November 5, 2019, Managing Director Dr. Stefan Hirschmann and his team from VÖB-Services organised an inspiring BANKENNETZWERK networking event “Digitisation and digital competence in banks” with an auditorium of 70 banking professionals.

Bankennetzwerk am 5.10.2019

im Holiday in Düsseldorf

Digitalisierung und Digitalkompetenz

Foto und Copyright

Bernd Schaller

Kiefernstr. 18

40233 Düsseldorf

www.schallerfoto.de

info@schallerfoto.de

00491776769111

Learning from history is crucial to understand the current societal changes triggered by technological progress. It‘s the basis to be able to make smart strategic decisions in a fundamentally changing business environment.

Some examples in the keynote referring to Professor Niall Ferguson‘s inspiring book „The Square and the Tower“. Enjoy some of his insights here

Bankennetzwerk am 5.10.2019

im Holiday in Düsseldorf

Digitalisierung und Digitalkompetenz

Foto und Copyright

Bernd Schaller

Kiefernstr. 18

40233 Düsseldorf

www.schallerfoto.de

info@schallerfoto.de

00491776769111

The Digital Summit (previously the National IT Summit) and the work that takes place between the summit meetings form the central platform for cooperation between government, business, academia and society as we shape the digital transformation. We can make best use of the opportunities of digitisation for business and society if all the stakeholders work together on this.

The National IT Summit was renamed the Digital Summit in 2017. This was to take account of the fact that digitalisation comprises not only telecommunications technology, but the process of digital change in its entirety – from the cultural and creative industries to Industrie 4.0.

The Digital Summit aims to help Germany to take advantage of the great opportunities offered by artificial intelligence whilst correctly assessing the risks and helping to ensure that human beings stay at the heart of a technically and legally secure and ethically responsible use of AI.

The Digital Summit looks at the key fields of action within the digital transformation across ten topic-based platforms. The platforms and their focus groups are made up of representatives from business, academia and society who, between summit meetings, work together to develop projects, events and initiatives designed to drive digitalisation in business and society forward. The Summit will serve to present the results of the work that has been done in the past, to highlight new trends and discuss digital challenges and policy approaches.

Looking forward moderating the Panel Discussion on “Digital Platforms for new AI-based Services”

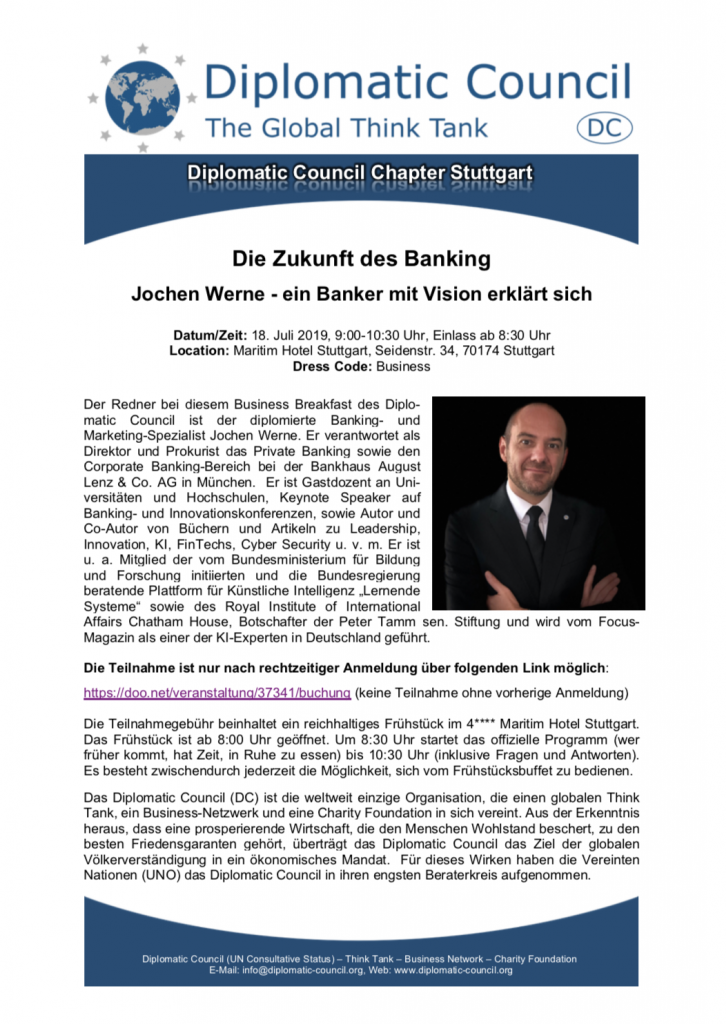

The speaker this morning is Jochen Werne, a graduate banking and marketing specialist. As director and authorized signatory, he is responsible for private banking and corporate banking at Bankhaus August Lenz & Co. AG in Munich. He is guest lecturer at universities and colleges, keynote speaker at banking and innovation conferences, author and co-author of books and articles on leadership, innovation, KI, FinTechs, Cyber Security and much more. He is a member of the platform for artificial intelligence “Learning Systems” initiated by the Federal Ministry of Education and Research and advising the German Federal Government as well as of the Royal Institute of International Affairs Chatham House, ambassador of the Peter Tamm sen. foundation and is listed by Focus-Magazin as one of the AI experts in Germany. He is the founder of the Global Offshore Sailing Team GOST and co-founder of the NGO Mission4Peace, which is dedicated to historical research, building international diplomatic relations and promoting international dialogue.

The participants will also get to know the Diplomatic Council (DC) this morning. It combines a global think tank, a business network and a charity foundation in a unique organization with consultative status at the United Nations. Stephanie Stoerk, Chapter Director DC Stuttgart, explains what distinguishes the Diplomatic Council from all other networks and what advantages it offers its members.

Breakfast is open from 8:30 am. At 9:00 a.m. we start our official program (whoever comes earlier has time to eat in peace), which lasts until 10:30 a.m. (including questions and answers). In between there is always the possibility to eat from the rich breakfast buffet.

PROGRAMM

Der Redner an diesem Morgen ist der diplomierte Banking- und Marketing-Spezialist Jochen Werne. Er verantwortet als Direktor und Prokurist das Private Banking sowie den Corporate Banking Bereich bei der Bankhaus August Lenz & Co. AG in München. Er ist Gastdozent an Universitäten und Hochschulen, Keynote Speaker auf Banking- und Innovationskonferenzen, sowie Autor und Co-Autor von Büchern und Artikeln zu Leadership, Innovation, KI, FinTechs, Cyber Security u. v. m. Er ist u. a. Mitglied der vom Bundesministerium für Bildung und Forschung initiierten und die deutsche Bundesregierung beratende Plattform für Künstliche Intelligenz „Lernende Systeme“ sowie des Royal Institute of International Affairs Chatham House, Botschafter der Peter Tamm sen. Stiftung und wird vom Focus-Magazin als einer der KI-Experten in Deutschland geführt. Er ist Gründer des Global Offshore Sailing Teams GOST und Co-Founder der NGO Mission4Peace, die sich der historischen Forschung, dem Aufbau internationaler, diplomatischer Beziehungen sowie der Förderung eines internationalen Dialogs widmet.

Darüber hinaus lernen die Teilnehmer an diesem Morgen das Diplomatic Council (DC) kennen. Es verknüpft einen globalen Think Tank, ein Business Network und eine Charity Foundation in einer einzigartigen Organisation mit Beraterstatus bei den Vereinten Nationen. Stephanie Stoerk, Chapter Director DC Stuttgart, informiert, was das Diplomatic Council von allen anderen Netzwerken unterscheidet und welche Vorteile sich daraus für die Mitglieder ergeben.Das Frühstück ist ab 8:30 Uhr geöffnet. Um 9:00 Uhr starten wir unser offizielles Programm (wer früher kommt, hat also Zeit, in Ruhe zu essen), das bis 10:30 Uhr andauert (inklusive Fragen und Antworten). Es besteht zwischendurch jederzeit die Möglichkeit, sich vom reichhaltigen Frühstücksbuffet zu versorgen

Also in the second part of our interview we do not go directly into the technical aspects of the introduction of artificial intelligence.

Based on the question “How do you get all this under one roof?” we get a look at Jochen’s personal insights and points of view and at how each individual can counter the increasing autonomisation and the change of the working world and society through algorithms with a corresponding attitude.

Jochen Werne is full-time Director & Authorized Officer for Bankhaus August Lenz & Co. AG of the Mediolanum Banking Group and is responsible for Business Development, Marketing, Product Management, Treasury & B2B Payment Services. In addition, he is involved in the development of non-profit organizations and a member of the Learning Systems Platform of the Federal Ministry of Education and Research.

The initiative www.wegofive.net addresses the question of how a unit of man and machine can be created in the working world of tomorrow and how algorithms can be seamlessly integrated into the organization in order to supplement the capabilities of employees.

As an independent interim manager, profile and team coach, Sascha Adam supports people, decision-makers and companies in actively shaping digital change.

More at www.wegofive.net/mission/about or www.sascha-adam.net.

Many thanks to the coast by east Hamburg in the Hafencity Hamburg for the permission to film here. A very recommendable location with obliging service, extraordinary menu and good drinks. Apropos, the background noises also give you the feeling of sitting directly with us 😉

Ein Banker mit einer (KI-)Mission / Teil 2: “Das neue Jetzt – Jeder kann etwas bewegen”

Auch in dem zweiten Teil unseres Interviews gehen wir nicht direkt auf die technischen Aspekte der Einführung von künstlicher Intelligenz ein. Ausgehend von der Frage “Wie bekommst Du das alles unter einen Hut?” bekommen wir einen Blick auf die persönlichen Erkenntnisse und Sichtweisen von Jochen und darauf wie jeder Einzelne mit einer entsprechenden Haltung der zunehmenden Autonomisierung und dem Wandel der Arbeitswelt und der Gesellschaft durch Algorithmen begegnen kann.

Jochen Werne ist hauptberuflich Director & Authorized Officer für das Bankhaus August Lenz & Co. AG der Mediolanum Banking Group und verantwortet dort die Bereiche Business Development, Marketing, Product Management, Treasury & B2B Payment Services. Darüberhinaus ist er am Aufbau gemeinnütziger Organisationen beteiligt und Mitglied der Plattform Lernende Systeme des Bundesministerium für Bildung und Forschung. Die Initiative www.wegofive.net geht der Frage nach wie in der Arbeitswelt von morgen eine Einheit aus Mensch & Maschine geschaffen werden kann und sich Algorithmen nahtlos in die Organisation integrieren, um die Fähigkeiten der Mitarbeiter zu ergänzen.

Sascha Adam unterstützt als selbstständiger Interimsmanager, Profile- und Team-Coach Menschen, Entscheider und Unternehmen dabei den digitalen Wandel aktiv zu gestalten.

Mehr unter www.wegofive.net/mission/about oder www.sascha-adam.net

Ganz herzlichen Dank an das coast by east Hamburg in der Hafencity Hamburg für die Genehmigung hier filmen zu dürfen. Eine sehr zu empfehlende Location mit zuvorkommender Bedienung, außergewöhnlicher Speisekarte und guten Drinks. Apropos, die Hintergrundgeräusche geben einem auch gleich das Gefühl direkt bei uns zu sitzen 😉

There is no lack of buzzwording when it comes to trends in the financial sector: Disruption, FinTech, block chain, crypto. Currently, another term is climbing the zenith of a media hype – platform banking. And not without good reason. “Platform Banking” was voted “Financial Word of the Year” in 2018. Behind this lies the call for banking institutions to open up to third-party providers. Banks and savings banks should not only offer their own services on open platforms, but should also integrate third-party offers and services. Consistently thought through to the end, banks will thus become more intermediaries for all possible services and less providers of their own financial services. The legally necessary prerequisites for such an approach in the strictly regulated financial market have already been set in motion by the adoption of the Payment Services Directive PSD2. Will platform banking become a new hope for the industry, or another risk component in the attempt to lose fewer customers to new technology competitors?

The hype surrounding the topic is understandable: Eight of the ten world’s most valuable companies – Amazon, Google, Microsoft, Apple and Co. – have a platform in their business model. And even more striking: Only one of these companies was already among the top 10 worldwide in 2008. This growth potential, which is the result of the platform expansion, is of course intended by many industries to benefit themselves. The world of finance is also changing rapidly. In recent years, a variety of innovative developments have taken place in the areas of payment transactions and payments. The arrival of third party providers and fintechs has changed the market sustainably and comprehensively. According to a recent whitepaper by Deloitte Consulting, banks will also have to consider a platform strategy in the future: In the future, the customer base will also be able to access products and services from third-party providers in addition to the existing offering. The long-term goal behind this is well known – to retain existing customers, acquire new ones and increase margins.

Platform as recipe for success?

In general, a platform can be seen as a place where supply and demand meet. Economists call such a market – not a new discovery. Due to the digitization of all areas of business and life, geographical boundaries of the marketplaces belong to the past. The result: an almost unlimited number of supply and demand meet on a digital platform – and competition is known to stimulate business. In these business models, the so-called “network effect” ensures that with each new provider on a platform, the incentive for demanders and customers also increases. And in general the more demanders there are on the platform, the more lucrative it becomes for the suppliers. Both sides save enormous search and time efforts and transaction costs are reduced. In short, reflects this the recipe for success behind industry giants such as Amazon, AirBnB, Uber and Co. Nevertheless, there are existing fundamental reservations. The desire of many bank managers to grab a straw in order to grasp a component of hope in a difficult market environment seems understandable. However, blind action is fatal in this situation. Banks must not forget what the emergence of competition in the form of FinTechs has already revealed: frightening weaknesses with regard to their own modern hardware and software solutions, organisation and innovative corporate culture. The fact is that the challenge facing change management is proving to be enormous. And this already now, without having given space to the idea of creating a single platform. The current wave of closing down banking or partnership-based Robo Advisor solutions shows how quickly these carriers of hope can become problems. The commission model behind this, which is always transparent and low priced, is hardly profitable for the banking infrastructure and marginalises the added value that an institution is able to provide for its customers.

The complexity of the changes on all levels, starting with the completely changed, technological possibilities and their effects on the transformation of long-established business models, over the resulting new economic situation of the enterprises are enormous. The difference to the past decades lies in the temporal component. If companies today do not react directly to market changes, they open the way for competitors to their own customers. And this faster than ever before. In such disruptive times, all those involved want an “efficient” change process. However, active, well-considered and vital change management is often criminally neglected. For this one opens door and gate to blind actionism.

The business model of a financial platform is complex, the regulatory framework is strict and the willingness of customers to switch is only slightly visible. For this reason, this business model has so far been too uninteresting for Internet groups. And now, of all things, the banks, often perceived as conservative and unmodern, are to be transformed into digital platforms that can compete with Amazon & Co?

Enormous change management challenge

Banks need a forward-looking and sustainable strategy. That is beyond question. At the latest since the massive “democratization” of the Internet at the end of the 1990s, our lives have been shaped by leaps in technology. In short, the world feels like it is turning faster than ever before. What does this mean for the banks of the 21st century? Anyone who does not understand this exponential dynamic of technical possibilities or does not take them sufficiently into account in his business model can quickly lose touch – with the customers of today and tomorrow. Open banking is both an opportunity and a technological challenge for the banking industry. The European Payment Service Directive 2 – or PSD2 for short – has inevitably made opening up to third parties the focus of the digital strategy.

At the technical level, this is primarily associated with the use of programming interfaces, so-called APIs, which enable both internal and external cost-effective and fast access to data, as well as functions of software applications. What provides the end customer with a cross-product customer experience, means for banks to strategically cooperate with external partners. For FinTechs, cooperation is also advantageous. It creates fast access to customers and their data, as well as to the necessary financial and structural prerequisites.

Anticipating these developments requires a good eye for tomorrow’s customers. After all, customer data is a success driver for future business models. A few years ago, FinTechs began to “poach” their digital offerings among the customer base of traditional institutes. All of this culminated in Robo-Advisors, standardized, computer-controlled asset managers with low fees. It was therefore time for the banks to set sail anew. The plan was to enter into symbioses with FinTechs or “buy” their products directly into their own portfolios. For many large banks, it has become good form to enter into cooperation with small, independent and innovative financial service providers. This is also clearly demonstrated by the current situation of FinTechs. Mergers and co-operation are nothing else than a proof for the fact that the search for sustainable business models is not easy with a fixed idea to solve, not even with the platform strategy. Nevertheless, neither the previous business models nor the product possibilities seem to be mature.

Don’t forget the human factor

The personal relationship, the touchpoint between customer and consultant in the real world, has been increasingly reduced by the acceptance of digital banking. Nevertheless, even if a digital experience is a good thing for a modern bank, consumers continue to appreciate human contact points – especially in economically or politically turbulent times.

The challenge lies in providing the right balance between the digital experience and the traditional, trust based, personal customer relationship.

Jochen Werne

This is precisely the added value that banks can really deliver in this environment today. And this without having to rely on the healing promises of platform banking. Be a guide in the digital jungle and protect customers from ill-considered gut decisions. In addition, it is important to include the customer’s background, apart from monetary issues, in the decision-making process. This usually requires a counterpart. Not a digital one, but a human one. A person of heart and soul who generates trust and can provide a place for personal encounter. Today, it is the customer alone who determines where this is located and what it should look like. The same goes for when this meeting takes place. The modern customer expects the best possible service regardless of space and time, not only in view of the phenomenon of digital gadgets.

At a time of fast pace and constant digital transformation, it is ultimately the Bank’s task to invoke traditional values, ensure humanity and meet the need to be an institution that the client trusts. Perhaps even beyond monetary concerns.

“An analogy for business leaders in the financial industry that compares the challenging times of today’s technological enterprise transformation with the changes during the time of the industrial revolution when steam ships ended the centuries-long era of sailing ships.”

In 1971, the BBC began broadcasting a series on the history of James Onedin, who, as captain and later as shipowner, lived through the stormy times of industrialisation and the conversion of the entire industry from sailing to steam navigation. The series, which takes place in Victorian England in the second half of the 19th century, describes in a special way the subtleties of the interplay of a changing market. New technologies, new skills of market participants, increased conflict potential between entrepreneurs and managers and reorientation in an environment of shrinking margins – special challenges for those who tried to continue their business as before: with sailing ships.

The documentation shows impressively how highly hierarchical organisations like the Royal Navy react and often struggle in times of major technological changes

The captain is responsible for bringing his ship, crew and cargo safely and within a specified time and financial framework to the port of destination. But what if the ship is no longer able to do this and the competition suddenly moves across the blue oceans with completely different ships? What if the shipowner does not have the capacity to trust the new technologies or simply does not have the financial resources to re-equip his fleet? And what about the crew? Does the crew has the necessary skills to sail on the new ships?

Many captains of banks and financial institutions seem to have this scenario all too present. E.g. due to declining customer traffic in bank branches, the high costs for a broad branch network are hardly to be paid today. Germany as a financial centre is “overbanked”, interest rates in the basement – the conditions in Germany for successful banking have never been as challenging as they are now. To this end, customers are continuing to drive change in the industry with their changing demands on digital tools.

Outwaiting a problem or tackling it

The complexity of economic changes has been enormous in every epoch, the difference to current upheavals lies in the temporal component. If companies do not react immediate to market changes today, they might loose their customers faster than ever before. In such disruptive times, all those involved want an “efficient” change process. The only problem is that the term “change” is so omnipresent that it is often perceived as stress and overload. As a result, many levels of management fall into one of the following situations: either they try to sit out the situation and leave change to their successors, or they push many, often less effective measures in an attack of blind actionism. Active, thoughtful and vital change management is often neglected.

More entrepreneurial thinking

Processes of change require both superiors and employees. If the existing situation cannot be improved or adapted at any vertical level, it must be questioned. Concluding, this means for all those involved that situations must always be reflected and corrective measures initiated at an early stage.

Understanding the corporate culture is vital for a successful transformation

In many companies, however, this need for action, which has a high potential for conflict, is often insufficiently communicated. In some places there is a lack of interest for employee issues, a lack of error and conflict culture and a minimal willingness to change. If banks neglect these issues, change processes threaten to fail on a broad basis. This means that managers in a disruptive environment have a natural need for action. The implementation of new strategies, systems and structures and early adaptation to changing market situations are vital factors for survival. A well-known quote by former US President Wodrow Wilson (1913-1921) is particularly valid for today’s highly competitive financial sector: “If you want to make enemies, try to change something.”

Those companies that create the change will share the large financial services market with the new market players and use instruments that did not exist in the classic banking of the past.

Just like James Onedin, who for the longest time was an advocate of classic sailing ships, finally added a modern steamship to his fleet. And to facilitate the change for himself personally, he named the ship after someone he loved.

Author: Angelika Breinich-Schilly interviewed Jochen Werne, Director Marketing, Business Development, Treasury & Payment Services at Bankhaus August Lenz.

Banks need to do a lot to keep pace in an increasingly digital world. In an interview with Springer Professional, Jochen Werne from Bankhaus August Lenz talks about the challenges they have to face and the right strategies.

(c) Bankhaus August Lenz

Springer Professional: Mr. Werne, what do you see as the most important driver of change in banks that is being invoked everywhere? Is it just the ongoing digitalization or do you see other reasons that require a strategic change process of the institutes?

Jochen Werne: The industry is undergoing what is probably a historic upheaval. We live in times of exponential technologies and in addition to the cost-side necessity of digitizing a large part of the processes of the institutes, the rapid change in customer expectations associated with technology, poses great challenges to an industry which is not known for being greatly agile. This disruption will eclipse many things and later perhaps be judged as revolutionary as the invention of the steam engine. In recent weeks, this has hardly made anything as clear as the rise of the online payment processor Wirecard. Wirecard was not only able to outperform Commerzbank in the DAX in September. Founded in 1999, the company has already overtaken Deutsche Bank in terms of market capitalization. In addition to the ongoing digitalization, there are also other current challenges: The low interest rate phase, which has now already lasted for a long time, is putting massive pressure on the margins of traditional houses. Political crises, trade disputes, currency problems such as in Turkey and Brexit naturally also have a direct effect on the classic business models of banks: In the future, they will have to adapt more than ever and increasingly prove their agility. The exponential leaps in technology and ever shorter product cycles are forcing the global economy as a whole to change and adapt to changing circumstances more than ever before. Kodak is a good example. For the sake of simplification, the company has often been accused of not being far-sighted, but it has failed because of a culture that has allowed little change. Two letters are currently electrifying the economy: AI. After decades of disinterest, artificial intelligence is suddenly once again regarded as the decisive guarantor of a company’s future viability. The immediate integration of AI into one’s own business model seems indispensable, even vital for survival. Without smart software, you’d think you were dedicated to meaninglessness. Similar to Facebook, the financial industry holds very valuable data. The preparation and processing of this data will not only become easier with maturing AI systems, but also much faster, cheaper and more targeted. It is nevertheless private and sensitive data. In order to make this resource usable in conjunction with external data, the industry must at the same time ensure its long-term security. Data may only be used in the sense of the customer, the human being – an objective that certainly has to apply to all AI-based approaches. Artificial intelligence offers an enormous range of opportunities for companies to be closer to their customers. But it also has its limits and here we are not only talking about technical limits, but also about limits that arise when the customer’s mindset does not go hand in hand with what is technically possible. Technology will only prevail if people accept it. Too radical a step, without consideration for all three areas Human, Digital and Culture, is always counterproductive.

Springer Professional: You describe that many decision-makers in the banks are well aware of the necessary changes in the business model. At the same time, however, top management often does not seem to set a concrete course and have corresponding visions. Why do you think that is?

Jochen Werne:Digitization, technological advances and the acceleration of product cycles are forcing executives to reposition their businesses. The question is no longer whether and why companies should change and introduce a more flexible organizational form, but only: How quickly and sustainably can they do it? The need for successful Change Management is not new and digitization was not an unforeseeable event. What is new, however, is the sum of the technical innovations, the possibilities offered by the technological leaps and the resulting need for extremely high implementation speeds. This circumstance has far-reaching effects on the entire management of the company. This often leads to different change processes overlaying each other, individual change processes being interrupted, modified or restarted and the organization being in a state of continuous change. And this also applies to the manager.

Springer Professional: In order to become a driver of innovation as a bank, it is necessary to anticipate not only upcoming technological but also social changes, some of which still vary greatly from region to region. One example is the payment behaviour of customers, which looks different in Germany than in other European countries or even in Asia. Many financial service providers now have think tanks or innovation labs to take on this task. But does some good ideas go up in smoke due to poorly thought-out change management?

Jochen Werne:Every new innovative offering must be easy for the customer to understand, intuitive to use and as a bank, absolutely trustworthy in terms of data security. The customer relies on the security of the communication channels as well as the careful handling of his private data. The challenge is to ensure data protection while at the same time providing the highest possible level of customer convenience. The resources of traditional banks offer enormous advantages here. An established bank is perceived as a brand by its clients, who at best associate it with important values such as trustworthiness, competence, industry knowledge and personal service. This trust is enormously important to us and should definitely be used.

Springer Professional:Companies in other industries sometimes find it easier to cope with change processes because they are not subject to additional strict regulations, as is the case with banks. Nevertheless, financial service providers such as Wirecard have succeeded in clearly differentiating themselves from traditional banks with their business model. Recently, the share value of this Fintech has even overtaken Deutsche Bank, the industry leader, as the most valuable institution. What can the industry learn from this?

Jochen Werne:Laws and guidelines have a strong influence on the competitive situation. MIFID II and PSD II are prime examples of this. In the second case, industry experts predicted that the mere opening of the banking infrastructure to third parties would lead to a major shift in competition. This is a big advantage for FinTechs, but also the FinTech industry, which is already in the process of market consolidation, has to make considerable investments and adjustments, even if the new regulations now also open up new market opportunities. Non-adaptable service providers without sustainable and a viable business models will be driven out of the market, as will banks whose offerings do not meet the needs of customers in a digital world. The example shows not only the usefulness of cooperation, but also its necessity. The advantages of banks, such as routine handling of regulatory issues or cross-selling opportunities due to the existing customer base, will continue to exist even after the market consolidation of the FinTech industry and the introduction of new technological standards.

Springer Professional: In order to be a driver of innovation, a bank does not necessarily have to handle all tasks alone. Where and when do cooperations with Fintechs make sense from your point of view?

Jochen Werne: What some have, others lack. Banks have a solid customer base, greater financial resources and, most importantly, a banking licence and the necessary know-how to deal with the relevant regulatory authorities. In addition, traditional financial institutions with many years of market experience, expertise in customer business and their trust can score points. Fintechs, on the other hand, have business models that are geared precisely to bringing innovative, customer-centric digital tools to market in a short space of time. Strategic alliances make sense, because ultimately everyone benefits – especially the customers. Not only the young generation today has very high demands on innovative mobile banking, but all age groups have discovered the new mobile possibilities in a very short time. Personal access to customers, which has persisted despite all the financial crises to date, is a sign that banks have preserved their most important asset – the trust of their customers. In an increasingly transparent and open financial world, however, the extent to which the customer’s loyalty to his bank will remain, is open.