It was a inspiring holding in hand the first edition of the JOURNAL OF AI, ROBOTICS & WORKPLACE AUTOMATION published by Henry Stewart Publications

We are pleased to give everyone the opportunity to download the entire article POINT OF NO RETURN by Jochen Werne & Johannes Winter here: https://lnkd.in/dmi9i9aB

The inspiring articles and case studies published in Volume 1 Number 1 are:

Editorial Tom Davenport, Distinguished Professor, Babson College, Research Fellow, MIT Center for Digital Business and Senior Advisor, Deloitte Institute for Research and Practice in Analytics

Practice papers:

The path to AI in procurement by Phil Morgan, Senior Director, Electronic Arts (EA)

How to kickstart an AI venture without proprietary data: AI start-ups have a chicken and egg problem — here is how to solve it by Kartik Hosanagar, Professor, The Wharton School of University of Pennsylvania and Monisha Gulabani, Research Assistant, Wharton UK AI Studio

Towards a capability assessment model for the comprehension and adoption of AI in organisations by Tom Butler PhD MSc, Professor, Angelina Espinoza-Limón, Research Fellow and Selja Seppälä, Research Fellow, University College Cork, Ireland

The path to autonomous driving by Sudha Jamthe, Technology Futurist and Ananya Sen, Product Manager and Software Engineer

Point of no return: Turning data into value by Jochen Werne, Chief Visionary Officer, Prosegur Germany and Johannes Winter, Managing Director, Plattform Lernende Systeme – Germany’s AI Platform

Robotic process automation and the power of automation in the workplace by Raj Samra, Senior Manager, PwC

Difficult decisions in uncertain times: AI and automation in commercial lending by Sean Hunter, Chief Information Officer and Onur Güzey, Head of Artificial Intelligence, OakNorth

The intelligent, experiential and competitive workplace: Part 1 by Peter Miscovich, Managing Director, Strategy + Innovation, JLL Technologies

Responding to ethics being a data protection building block for AI by Henry Chang, Adjunct Associate Professor, The University of Hong Kong

Legal issues arising from the use of artificial intelligence in government tax administration and decision making by Liz Bishop Barrister, Ground Floor Wentworth Chambers

Reflections by Jochen Werne, Chief Development & Chief Visionary Officer Prosegur Germany (published in Prosegur Express 02/2021)

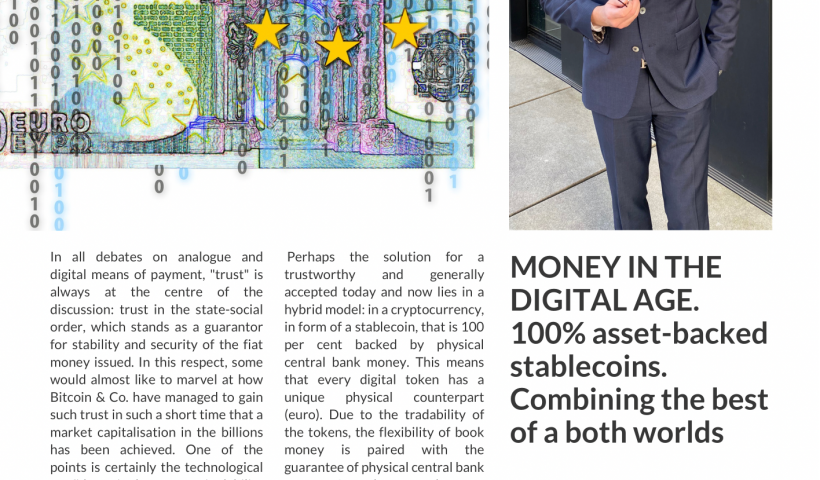

In all debates on analogue and digital means of payment, “trust” is always at the centre of the discussion: trust in the state-social order, which stands as a guarantor for stability and security of the fiat money issued. In this respect, some would almost like to marvel at how Bitcoin & Co. have managed to gain such trust in such a short time that a market capitalisation in the billions has been achieved. One of the points is certainly the technological confidence in the non-manipulability of the blockchain. But is the blockchain really not manipulable, or is it rather a question of time before an attack will succeed? And what conclusions are central banks around the world drawing from this as they look at creating central bank digital currencies? Currencies designed to bridge the gap between the stability of analogue central bank money and the demands of our digital age.

Perhaps the solution for a trustworthy and generally accepted today and now lies in a hybrid model: in a cryptocurrency, in form of a stablecoin, that is 100 per cent backed by physical central bank money. This means that every digital token has a unique physical counterpart (euro). Due to the tradability of the tokens, the flexibility of book money is paired with the guarantee of physical central bank money. Last but not least, a regulated trustee function guarantees that the existing and securely stored central bank money is always paired with its digital twin. Thus. the best of both worlds is firmly united.

28 February 2021 published in the current issue of the magazine gi Geldinstitute

For the trade magazine gi Geldinstitute, leading experts answered Stefanie Walter’s questions on the topic of “Process Mining at Banks”. Jochen Werne – Prosegur Germany, Gerrit von der Hardt – TARGO Dienstleistungs, Sebastian Hennerici – Aareal Bank AG, Gerrit Meier – Hanseatic Bank GmbH & Co KG, Thorsten Briest – PSD Bank Braunschweig eG, Christian Meusel – Berliner Volksbank eG, André H. Burger – Synpulse Management Consulting

Professional know-how and the right feeling for changing customer needs are essential factors in being able to innovatively develop needs-based solutions for our customers.

The entire roundtable talk in the current print edition or soon online at www.Geldinstitute.de

An event organised by acatech – the National Academy of Science and Engineering which is the voice of the technological sciences at home and abroad. acatech provides advice on strategic engineering and technology policy issues to policymakers and the public. The National Academy of Science and Engineering fulfils the mandate to provide independent, evidence-based advice that is in the public interest under the patronage of the Federal President.

Start: 05 March 2021 – 10:00 a.m. End: 05 March 2021 – 11:30 a.m Location: Virtual event – Language: German

Especially in the Corona pandemic, digital technologies proved their usefulness: through them, companies were more adaptable in the crisis. What role do digital technologies now play on the way out of the crisis – especially for medium-sized companies? How do they manage the digital transformation and develop new value creation models?

A debate organized by acatech

The host is discussing these and other questions with guests from business and research on 5 March.

PROGRAM

Welcome:

Dr. Johannes Winter, acatech Secretariat

Moderation:

Prof. Dr. Michael Dowling, University of Regensburg/acatech

Impulse/Podium: DATA, VALUES, VALUE CREATION – WHERE IS THE JOURNEY GOING?

Dr. Wolfgang Faisst, CEO ValueWorks.ai / Platform Learning Systems BEST PRACTICE INDUSTRY 4.0

LESER GmbH & Co. KG: Digital transformation in medium-sized companies Kai-Uwe Weiß, Head of Global Industrial Engineering FORCAM GmbH: Value creation through integrative IIoT platform solution Franz Gruber, Founder and Advisory Board

EXPERT DISCUSSION: DIGITAL SOLUTIONS FOR A RESILIENT COMPANY

Olga Mordvinova, CEO incontext.technology GmbH / Learning Systems Platform Jochen Werne, Prosegur Cash Services Germany GmbH / Learning Systems Platform Franz Gruber, FORCAM GmbH Kai-Uwe Weiß, LESER GmbH & Co. KG

Registration: Admission free; registration required. Please register under the following link, all registered will receive the access link before the event.

Edited by Prof. Dr. Peter Scholz; published by Palgrave Studies in Financial Services Technologies. Buy a copy here

Congratulations to Peter Scholz for publishing this excellent book on new technological investment methods. It was an honour for me to write the foreword and I wish every reader enriching insights into this new field of investing in the digital age.

Jochen Werne

Prof. Dr. Peter Scholz

This book is the first to provide comprehensive answers to these questions in a fundamental, decisive, detailed and nuanced way. It clarifies the basics, the technology and the tactics behind those clever, financial machines, gives insights into their previous track record to date and much more. Looking ahead, it provides a preview of what is and may be yet to come. As a matter of fact, so far only a relatively small percentage of the global investment community have more or less relied on robo-advisors, depending on their respective culture. It is also a fact that we are only at the beginning of development. We have all borne witness to how exponentially fast things can move forward. One such example is the evolution of smartphones—which by the way have been around for just a little longer than robo-advisors.

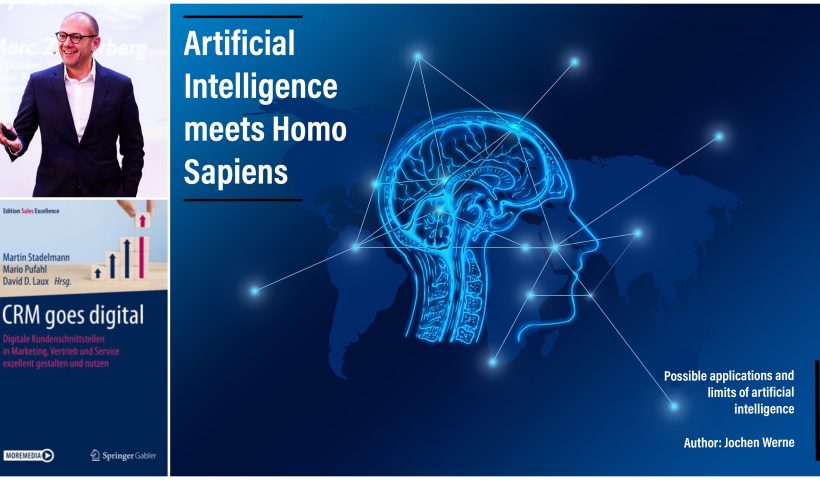

It has been a privilege contributing as co-author for the fifth time to an inspiring book project. “CRM goes digital“ has been initiated by Dr. Martin Stadelmann, Mario Pufahl and David Lauch and is part of the Springer Gabler Edition Sales Excellence book series (ESE)

Artificial Intelligence meets Homo Sapiens – Possible applications and limits of artificial intelligence

Author: Jochen Werne

Werne J. (2020) Artificial Intelligence meets Homo Sapiens – Einsatzmöglichkeiten und Grenzen Künstlicher Intelligenz. In: Stadelmann M., Pufahl M., Laux D. (eds) CRM goes digital. Edition Sales Excellence. Springer Gabler, Wiesbaden

Abstract

A special encounter. Algorithms developed by humans meet everything that man and nature embody – from industrial processes to our very own behaviour. A race between countries and companies has begun to decide the enormous potential of AI and its impact on our consumer behavior, as well as on our society. However, despite all the euphoria, it is important to understand the topic, its possible applications and also its limitations well, so as not to succumb to the danger of losing oneself in technology-believing magic.

About the book: CRM goes digital

Consistent customer orientation and digital transformation lead to completely new approaches in management: the focus is on omnichannel or mobile CRM concepts, big-data and social media instruments, and automation. But what does this mean in concrete terms for marketing, sales and service? What effects does digitalization have on product and service optimization or on sales management and customer loyalty? How can methodical customer orientation contribute to an improvement in sales performance? Answers to these and other questions are provided by the contributions from science and practice in this book. The authors illuminate the requirements and possible solutions of CRM systems along the concept of the customer journey using selected industry examples. They provide concrete recommendations for action and offer managers and users from customer-oriented business areas valuable orientation aids for the implementation of digital customer management.

From the content

CRM: strategies, organisation, controlling and employees

Concepts in digitisation

Best Practices in CRM: Case studies of customer-centric companies

Topics of CRM research

1st published in the German newspaper Handelsblatt on January 8, 2020 – translated by DeepL.com. Photos: Pixabay

Looking at the world sometimes gives the impression that things seem to be much better outside Europe. Examples? The world’s largest airport, Beijing-Daxing, goes into operation after four years of construction, while at BER, construction continues after 13 years. The coffee house chain Luckin Coffee, valued at $4.5 billion, will replace Starbucks as No. 1 in the Chinese market by the end of the year, two years after its foundation. Digital platform companies such as Apple, Amazon, Alphabet, Tencent & Co. have left the traditional commodity and industrial groups behind in terms of value.

What made these American and Asian companies so big? Absolute willingness to implement at high speed, massive state and private investments, sometimes industrial policy intervention, huge, scalable domestic markets and a just-do-it mentality favour economic and technological development alongside a number of other factors.

Is Europe, on the other hand, in a downward spiral? Is the continent now losing the much-discussed second half of digitisation, which is mainly about the digitisation of industry, now that the B2C race seems to be lost?

The recent history can also be told in a different way. The financial crisis of 2008/2009 has shown how valuable Europe’s and especially Germany’s strong industrial core is. A highly specialised, excellent SME sector and the leading groups from mechanical, plant and vehicle engineering to the pharmaceutical and chemical industries are anchors of stability. With Industry 4.0, the vision for the future of value creation comes from Germany, and there is a worldwide competition for its widespread introduction.

The strength lies in product innovation, especially in complex products such as machine tools, medical devices, vehicles or building services engineering. Germany also has world market leaders in engineering and in production and automation technology. Despite all the negative predictions, Germany has further expanded its strength in networked physical platforms with the integration of IoT, data and services in industrial environments and has secured a very good starting position. The German research landscape also holds an internationally good position in areas critical to success such as semantic technologies, machine learning and the digital modelling of products and users. And let’s not forget that the companies in the country have produced outstanding software products for the fast, reliable and scalable processing of big data and the integration of business processes.

While Germany wants to consolidate its pioneering position as the world’s supplier, the USA is relying on its expertise as a global networker and China is relying on short decision-making paths, capital intensity and a large domestic market in which it can scale quickly. In this situation, it is important that we concentrate on our strengths and resolutely tackle the digitization of industry and SMEs. However, this requires a much faster entry into the emerging B2B platform markets.

In Europe, we stand for a liberal value system, both economically and politically, which, as in the past, has proven to be the decisive differentiating factor in the medium and long term. The debate on the use of data is conducted in Europe in good tradition at an extremely high level and this in the good understanding that digitisation is not coming over us, but is made by people and is intended to serve them.

It is therefore the right moment to take a decisive step towards the future and to open up Europe’s path. To do this, we need a large, homogeneous domestic market that will make us almost competitive with the USA and China. We also need substantial investment in digital infrastructure and cybersecurity, as well as training and further education. Both competitive regions currently have the power to set standards in digitization as well. The goal of the European Union to create a single digital internal market is laudable, but final implementation is still pending. This implementation, however, is the important and very concrete next step in order to be able to achieve the competition-relevant scaling effects and to be able to play a competitive role in data-based business model innovations.

The second half is running and nothing is lost.

About the authors

Jochen Werne (48) is a member of the Executive Board and Chief Development Officer of Prosegur Cash Services GmbH, as well as a member of the Artificial Intelligence Learning Systems Platform and the Royal Institute of International Affairs, Chatham House.

LinkedIn: https://www.linkedin.com/in/jochen-werne-2292507a/

Twitter: @WerneJochen

E-mail: jw@JochenWerne.com

Dr. Johannes Winter (42) heads the office of the Learning Systems Platform and the technology department at the German Academy of Science and Engineering (acatech).

LinkedIn: https://www.linkedin.com/in/johannes-winter-13048629/

Twitter: @jw4null

e-mail: winter@acatech.de

On Tuesday, November 5, 2019, Managing Director Dr. Stefan Hirschmann and his team from VÖB-Services organised an inspiring BANKENNETZWERK networking event “Digitisation and digital competence in banks” with an auditorium of 70 banking professionals.

Bankennetzwerk am 5.10.2019

im Holiday in Düsseldorf

Digitalisierung und Digitalkompetenz

Foto und Copyright

Bernd Schaller

Kiefernstr. 18

40233 Düsseldorf

www.schallerfoto.de

info@schallerfoto.de

00491776769111

Learning from history is crucial to understand the current societal changes triggered by technological progress. It‘s the basis to be able to make smart strategic decisions in a fundamentally changing business environment.

Some examples in the keynote referring to Professor Niall Ferguson‘s inspiring book „The Square and the Tower“. Enjoy some of his insights here

Bankennetzwerk am 5.10.2019

im Holiday in Düsseldorf

Digitalisierung und Digitalkompetenz

Foto und Copyright

Bernd Schaller

Kiefernstr. 18

40233 Düsseldorf

www.schallerfoto.de

info@schallerfoto.de

00491776769111

The Digital Summit (previously the National IT Summit) and the work that takes place between the summit meetings form the central platform for cooperation between government, business, academia and society as we shape the digital transformation. We can make best use of the opportunities of digitisation for business and society if all the stakeholders work together on this.

The National IT Summit was renamed the Digital Summit in 2017. This was to take account of the fact that digitalisation comprises not only telecommunications technology, but the process of digital change in its entirety – from the cultural and creative industries to Industrie 4.0.

The Digital Summit aims to help Germany to take advantage of the great opportunities offered by artificial intelligence whilst correctly assessing the risks and helping to ensure that human beings stay at the heart of a technically and legally secure and ethically responsible use of AI.

The Digital Summit looks at the key fields of action within the digital transformation across ten topic-based platforms. The platforms and their focus groups are made up of representatives from business, academia and society who, between summit meetings, work together to develop projects, events and initiatives designed to drive digitalisation in business and society forward. The Summit will serve to present the results of the work that has been done in the past, to highlight new trends and discuss digital challenges and policy approaches.

Looking forward moderating the Panel Discussion on “Digital Platforms for new AI-based Services”

It has been pleasure being guest author for the DIGIPRAKTIKER, Finanz Colloquium Heidelberg.

What role does the human factor play in times of exponential technological progress?

Author: Jochen Werne, Director Business Development, Product Management, Treasury and Payment Services at Bankhaus August Lenz & Co. AG

I. Introduction

The only constant in history was, is and remains change. Gutenberg’s invention of the printing press in 1450 was a milestone on the timeline of human development. Today we still take note of this invention, which was considered an innovation at that time, but we have long lived surrounded by smartphones and cloud applications, in which we can store the most private information and retrieve it from anywhere in the world. Today’s change is being driven by a veritable digital revolution.

Digital change already has fundamental consequences for individuals and their lifestyles, but it is developing its full potential when it comes to interacting with our social environment. In times of smart robotics and maturing systems in relation to artificial intelligence, the question arises again and again what role humans play on the stage of these technologies. Is he …