He writes in his article: In an increasingly regulated market environment, providers who use their data intelligently will be the most successful, says Jochen Werne from Experian in an interview with FinanzBusiness.

Data is the new oil, they say: “The quality of data will become the kingmaker in the credit risk market of the future and open the way to new market opportunities,” says Jochen Werne, CEO of data service provider Experian DACH. In an increasingly regulated market environment, providers who use their data intelligently and master the balance between data protection and customer experience will be the most successful.

Werne names six “top challenges” for this year. These arise from regulations from the European Banking Authority (EBA) – and from technological developments. On the one hand, risk management is to be significantly improved and sustainability criteria verified at the behest of the European Central Bank and the EBA supervisory authority. On the other hand, artificial intelligence (AI) is opening up completely new opportunities in an increasingly complex market environment.

Original published in German by IT Finanzmagazin – find here. Translation provided by DeepL.com. Photos provided by Pixabay, Experian, Jochen Werne. Collage design by Canva

STRATEGY 23 January 2024

EBA deadline of 30 June: data quality will be decisive in the assessment of credit risks

Financial institutions are facing a significant change in the assessment of credit risks this year. Now comes 30 June: the deadline for new standards in credit risk assessment. Jochen Werne (CEO Experian DACH) is convinced that data quality will become the kingmaker in the credit risk market.

by Jochen Werne, CEO Experian DACH

Since 2021, financial service providers have been required to implement the supervisory priorities of the ECB and EBA. These priorities include the comprehensive improvement of credit risk management practices and the integration of new risk factors, particularly in the area of climate and the environment, into their risk management strategies. At the same time, the requirements for data management in the context of credit scoring are increasing. Artificial intelligence (AI) will play a key role here and banks will have to adapt to the new EU AI Act.

“By the deadline of 30 June 2024, large banks must have adapted their systems and infrastructures in accordance with the EBA Loan Origination and Monitoring Guidelines (EBA-GL LOM) for effective credit risk management and monitoring.”

This also includes closing data gaps. However, smaller, nationally supervised financial institutions must now also comply with these new guidelines, as additional elements of the 7th MaRisk amendment came into force on 1 January 2024, which are based on the EBA guidelines, among other things. Financial organisations must review their existing practices in 2024 and adapt their credit risk assessment standards accordingly. In future, credit assessment models will have to take much greater account of transparency, fairness and sustainability, particularly from an ESG perspective. The game changer for this is increasing their data quality.

All of this leads to five important changes:

1. Profitability strategies in a challenging market environment

“Investments in technologies such as generative AI and forward-looking risk management are becoming increasingly important.”

Advanced data analytics support organisations in various phases of their customer lifecycle. Already in the application phase, high data quality enables a more efficient assessment of creditworthiness. In portfolio management, advanced data analysis helps to proactively manage risks and dynamically manage the credit portfolio. Advanced analytics and high data quality help to strengthen resilience to risks, including data-based early risk identification and an optimised dunning and collection process.

2. Digitalisation for resilience, including against novel risks

“Over the next 12 months, strengthening business resilience through automation and digitalisation will be key to responding to new risks such as AI, cyber threats and geopolitical tensions.”

These challenges not only affect the target customer landscape, but are also of great importance in the context of new ESG requirements. Due to their complexity and innovative nature, traditional approaches based on historical data cannot cope with these risks: Traditional approaches to data analysis and model preservation increasingly have to deal with slow regulatory processes on the one hand and a more dynamic macroeconomic environment and growing cyber risks on the other. In order to cope with this competitive situation, new strategies in the utilisation of all relevant data are urgently required, which place advanced analytics and the improvement of data quality at the centre.

3. PSD3, PSR and FIDA: Banks between risk and opportunity

As one of the players with the greatest wealth of data, this presents banks with a high risk in the face of new competitors. At the same time, however, it also offers them an opportunity to become a trusted partner for consumers. These regulations, which focus on the promotion of open banking services, greater control of data access and measures against online fraud, represent a starting point for financial institutions to think about the further use of transaction data. In addition to combating fraud, advanced analytics of transaction data, even taking into account all compliance requirements, opens up additional opportunities for interaction with end customers to improve the customer experience or the chance to monetise data.

4. Growth driver EU AI Act

“The EU AI Act will have a significant impact on the use of AI in the financial sector and further strengthen the financial sector’s technology focus.”

AI and machine learning (ML) will further automate decision-making processes in the future and strategic investments in this area will therefore become even more crucial for growth in the future. According to a study by Forrester Consulting commissioned by Experian, 60 per cent of German companies already take a similar view and have a comprehensive AI-based risk management programme in place. By using these technologies, credit and fraud risks can be assessed more precisely and efficiently, even in uncertain economic times. Companies that implement these developments are positioning themselves as pioneers in a rapidly developing, technology-driven financial sector: 78 per cent of the companies surveyed in the study in Germany also state that they are prioritising the use of further AI and ML applications.

5. Continuation of cloud migration in the financial world

“The ongoing implementation of continuous development and continuous improvement, particularly in the areas of business, analytics and IT, is becoming increasingly important.”

This includes identifying core business processes that will benefit significantly from cloud migration and defining clear priorities and objectives for the migration process. Cloud-based data analytics plays a central role in gaining valuable insights from customer behaviour, market trends and operational data to improve business processes and make more informed decisions.

—————————-

About the author: Jochen Werne has been CEO DACH at Experian since August 2023. Previously, he served as Managing Director at Prosegur Crypto and as Chief Development & Chief Visionary Officer at Prosegur, where he was responsible for the development and implementation of strategies in the areas of business development, innovation and international sales. Werne’s career includes significant leadership positions at Bankhaus August Lenz & Co. AG, Mediolanum Banking Group, where he served as Director and Authorised Representative and was instrumental in the company’s digital business transformation. His academic career includes a FinTech programme at the University of Oxford (2017-2018) and a Diploma in International Banking at Goethe University Frankfurt (1997-2000).

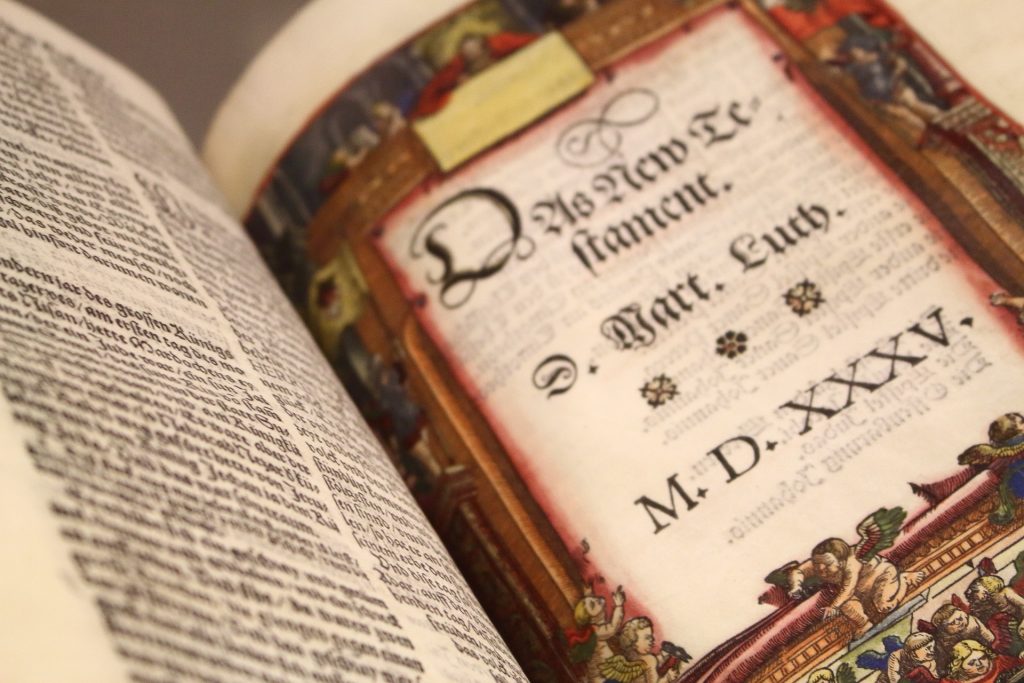

From the eloquent words of Shakespeare in Henry V, where he once proclaimed, “all things are ready if our minds be so”^1 to the monumental shifts brought by Gutenberg’s printing press^2, history reminds us that change is both an inevitable and defining characteristic of human progress. As the world stands at the threshold of a new epoch marked by rapid technological shifts and pronounced geopolitical transformations, this profound sentiment compels us to reflect on the paramount importance of preparedness and perspective. The way societies respond to these shifts determines the direction of their trajectory. In our current age, Europe finds itself at the nexus of global transformations driven by technological advancements and geopolitical tectonics.

Technology: A Historical Reflection

Peering through the lens of history, one quickly realizes that technology has been both a beacon of hope and an augury of upheaval. Take the 15th century’s monumental invention of the printing press as a case in point^2. This groundbreaking innovation democratized access to information and catalysed a substantial uptick in literacy rates across Europe. As Eisenstein posits, the “Printing Revolution” catalyzed an era where knowledge was no longer the privilege of the few but a right of the many^2. Yet, its reverberations were not confined to just reading and writing. The press became the vessel through which Martin Luther disseminated his Ninety-Five Theses, triggering a religious revolution that reshaped the European continent.

However, the journey wasn’t without turbulence. This democratization of knowledge played a pivotal role in challenging the established order, culminating in events like the Reformation, which MacCulloch describes as Europe’s great house divided^3.

Niall Ferguson, in “The Square and the Tower”, beautifully illustrates the timeless tension and interplay between networks and hierarchies^4. Historically, technologies like the printing press have emerged as disruptors, challenging established orders and reshaping hierarchies. The press, for instance, allowed for the free flow of ideas, becoming an early network that democratized information. Yet, not everything it propagated was for the betterment of society. The infamous “Malleus Maleficarum”, an ostensibly scholarly treatise, fueled the flames of the European witch hunts, leading to persecution, paranoia, and a dark chapter in history^5.

From Past to Present: The Tech Geopolitical Nexus

Fast forward to the present, and we witness a world where technology continues to shape geopolitical realities. Maddison’s macro-economic study reveals that the global center of economic gravity has been steadily shifting towards the East, particularly since the dawn of the 21st century^6. Nowhere is this shift more apparent than in the realm of technology.

The US-China tech rivalry, explored by Fuller, highlights the strategic challenges posed by China’s technological ascent^7.

The race for supremacy in AI, quantum computing, 5G, and biotechnologies marks the modern-day power play. But this isn’t merely about technological one-upmanship; it signifies a larger canvas of geopolitics, economics, and even societal values.

Many analysts are drawing parallels to the Cold War, coining the term “Tech Cold War” or “Cold War II”. Unlike the 20th-century version, primarily characterized by nuclear deterrence between the USSR and the US, this new Cold War positions the US and China in an intense rivalry for technological, economic, and military dominance. In the midst of this rivalry, both nations are hyper-aware of the stakes.

Navigating the Waters of New Geopolitical Paradigms

More than a century ago, the naval strategist Alfred Thayer Mahan, in his seminal work on sea power, postulated that maritime dominance was crucial to national greatness.

Today the Indo-Pacific has become the focal point of 21st-century geopolitics. Here, China’s assertive ‘Two Ocean Strategy’ is emblematic of its ambitions to exert influence both in the Pacific and the Indian Ocean. This expansive maritime vision is not just about sea lanes and trade; it’s a reflection of China’s aspirations to be a global power.

Simultaneously, the Taiwan question looms large in this maritime strategy. Its strategic location in the first island chain poses both an opportunity and a challenge for Beijing. Control over Taiwan would offer unencumbered access to the broader Pacific.

However, the rise of one power often brings countermeasures by others. The ‘AUKUS’ agreement between Australia, the United Kingdom, and the United States is a manifestation of this dynamic. While cloaked in the language of technological collaboration, especially in the realm of nuclear-powered submarines, the underlying intent of AUKUS is clear. It seeks to counterbalance China’s growing naval capabilities and assertiveness, particularly in the South China Sea.

Reflecting on Mahan’s sea power doctrine in this context provides a sobering perspective. Mahan believed that maritime dominance was the linchpin of global influence. Yet, he also understood the responsibilities and challenges that came with such power. In our contemporary setting, while nations pursue their maritime strategies, it is imperative they also embrace the principles of dialogue, cooperation, and conflict avoidance.

Taiwan epitomizes this interplay. As a beacon in semiconductor manufacturing, Taiwan’s geopolitical relevance can’t be overstated. Any instability could trigger economic consequences potentially dwarfing the aftermath of the Covid-19 pandemic^9.

Taiwan and Europe: Quietly Interwoven, Profoundly Connected.

In the intricate web of global technology supply chains, few names stand out as prominently as Taiwan Semiconductor Manufacturing Company (TSMC). Founded in 1987, TSMC has ascended the technological hierarchy to become the world’s leading semiconductor foundry, a testament to its unwavering commitment to innovation and excellence.

TSMC’s significance is multifaceted. For one, it’s the world’s largest dedicated independent semiconductor foundry^8. With clients ranging from major tech giants like Apple and Nvidia to burgeoning startups, TSMC’s production underpins a vast swathe of the digital products and solutions we rely on daily. However, TSMC’s role isn’t merely a commercial or technological one. It is geopolitical. With the escalating “Tech Cold War” between the U.S. and China, TSMC finds itself at an intriguing junction. The company’s strategic importance is underscored by global reliance on its cutting-edge chip manufacturing capabilities. This reliance has not only made TSMC a coveted partner but also a strategic asset in the larger scheme of global geopolitics. The U.S. push to ensure TSMC sets up manufacturing bases on its soil, and China’s keen interest in the semiconductor sector, highlights the foundry’s pivotal position.

Furthermore, TSMC embodies Taiwan’s broader significance in the tech world. As the geopolitical tussle intensifies, Taiwan – and by extension, TSMC – becomes a linchpin for global tech supply chains. A disturbance in TSMC’s operations, as speculated, could have cascading ramifications across industries, from consumer electronics to automotive and healthcare. Any significant disruption in this intricate supply chain would reverberate globally, with experts suggesting a potential 5% drop in global automotive production^9.

As chips become smaller, denser, and more powerful, the precision and capability of lithography machines must evolve in tandem.

Here’s where Europe and ASML, a Dutch gem, comes into play. The company is the sole producer of extreme ultraviolet (EUV) lithography machines^8, an advanced technology that allows for the creation of incredibly dense and efficient chips. With transistors now approaching atomic scales, EUV lithography is no less than a technological marvel, allowing chipmakers to etch circuits just a few nanometers wide.

However, the conversation around ASML isn’t merely about technological mastery. Given its unique position as the only producer of these EUV machines, ASML enjoys a quasi-monopolistic status in this niche yet profoundly impactful domain. In an era where technological supremacy is increasingly intertwined with geopolitical power, also ASML’s importance cannot be overstated. The machines they produce are not just expensive and sophisticated pieces of equipment; they are, in many ways, gatekeepers to the next generation of digital innovation.

Such a near-monopoly naturally draws attention. Nations and corporations are keenly aware of the strategic value inherent in controlling or accessing state-of-the-art chipmaking technology. With the ongoing technological cold war, where semiconductor supply chains have become part of the geopolitical chessboard, ASML finds itself in a spotlight it never sought but cannot avoid.

Europe’s Crucial Pivot

Europe’s position in this evolving tech landscape is unique. While traditionally viewing the Atlantic alliance as a cornerstone of its foreign policy, the rise of China necessitates a recalibrated approach^10. Europe’s interlinked trade with China, especially through critical chokepoints like the Malacca Strait, underscores the strategic dimension of this relationship^11.

In this whirlwind of technological and geopolitical flux, Europe is not an idle spectator. With a collective GDP nearing $22 trillion, it wields considerable influence. Europe’s role is multi-dimensional: an economic powerhouse, a voice of reason in tumultuous times, and often a mediator in global disputes.

The ECB recognizes that the financial institutions it oversees must adapt to these transformative times. A crucial element of this adaptation is embracing digitalization, with a special emphasis on robust data-driven risk management.

Strengthening Resilience: The intricate web of global economies translates to shared vulnerabilities. It’s imperative for Europe’s financial edifice to be robust, equipped to handle external shocks, and maintain systemic stability.

Digitalisation & Institutional Strengthening: The burgeoning fintech sector necessitates a complete metamorphosis for legacy banks. This isn’t a mere cosmetic digital overhaul. Banks need to internalize and deploy intelligent digitalization. Central to this transformation is data analytics, supercharged by AI. Harnessing data, drawing meaningful insights, and predicting trends will determine who thrives in this new era.

Climate Change Initiatives: Europe has consistently championed sustainability. The financial sector’s alignment with green, sustainable practices isn’t just altruistic; it’s also economic prudence, ensuring long-term viability and stability.

The above mentioned ECB focus is highlighted by Experian’s 2023 report on why AI-driven, regulatory-compliant analytics solutions are becoming imperative for European banks^13.

The AI Paradigm: Europe’s value-based Ethical Approach

Europe’s approach to AI regulation, championing the cause of ‘explainable AI’, shows its commitment to integrating technology with ethics. This dedication harks back to its legacy of literacy and the importance of accessibility, a theme explored by Graff^14. As Europe navigates the ‘Asian Century’^15, it does so with a clear vision: to leverage its historical experiences and chart a course that balances innovation with ethical considerations. The European AI Act encapsulates this approach. The Act’s core philosophy revolves around ensuring AI applications are safe and respect existing laws and values. This includes transparency obligations, strict criteria for ‘high risk’ AI applications, and a provision for setting up a European Artificial Intelligence Board.

One might wonder, why the emphasis on explainability? As AI systems permeate critical sectors, from healthcare to finance, their decisions can profoundly impact individuals. An ‘explainable AI’ ensures that these decisions are not just accurate but also comprehensible to the average person. This empowers individuals, fostering trust in AI systems.

The Act, however, isn’t just about explainability. It recognizes the diverse applications of AI and categorizes them based on risk. For ‘high-risk’ applications, stringent requirements, from transparency to accuracy and security, are mandated. This stratified approach ensures that while innovation isn’t stifled, critical areas receive the scrutiny they warrant.

Economic Powerhouses: A Comparative Analysis

Any discussion on global transformation would be incomplete without examining the economic engines driving these changes. China’s astounding growth, with a GDP of $17.7 trillion by 2022^16, and its decade-long average annual growth rate of 6.5%, contrasts with the US’s $25.3 trillion GDP and a more conservative 2.3% growth rate^17. The European Union, showcasing resilience and integration, clocks a collective GDP nearing $22 trillion^18, with trade figures underscoring its global economic clout^19.

Conclusion: Europe’s Way Forward

Our world is in a state of flux, reminiscent of those transformative moments in history. From the monumental shifts of the Printing Revolution^2 to the divisive yet transformative Reformation^3, Europe has witnessed and shaped global trajectories. As it stands at the crossroads of another transformation, it draws from its rich historical tapestry, aiming to strike a balance between embracing the future and preserving its core values.

The digital future beckons, but it’s not without its challenges. Whether it’s the complex web of tech geopolitics or the imperative of sustainable growth, Europe’s journey forward will need to be both adaptive and principled. At the heart of this journey lies the potent combination of data and ethics. And as Europe strides into the future, it carries with it a clear message: progress, when rooted in ethics and driven by knowledge, can usher in an era that’s not just technologically advanced but also just, balanced, and peaceful.

Footnotes:

^1 Shakespeare, William. “Henry V.” Act IV, Scene 3. ^2 Eisenstein, Elizabeth L. “The Printing Revolution in Early Modern Europe.” Cambridge University Press, 1983. ^3 MacCulloch, Diarmaid. “Reformation: Europe’s House Divided 1490-1700.” Penguin UK, 2004. ^4 Ferguson, Niall. “The Square and the Tower: Networks and Power, from the Freemasons to Facebook.” Penguin, 2018. ^5 Kramer, Heinrich and Sprenger, James. “Malleus Maleficarum.” Dover Publications, 1971. ^6 Maddison, Angus. “Contours of the World Economy 1-2030 AD: Essays in Macro-Economic History.” Oxford University Press, 2007. ^7 Fuller, Douglas B. “Cutting off our nose to spite our face: US policy toward Huawei and Taiwan in the shadow of the Chinese tech challenge.” International Security 45.3 (2021): 52-89. ^8 Chappell, Bill. “ASML: The Obscure Dutch Company That’s Enabling Big Advances In Tech.” NPR, 2019. ^9 “The Economic Impact of a Taiwan Crisis.” Nikkei Asia, 2023. ^10 Casarini, Nicola. “The Rise of China and the Future of the Atlantic Alliance.” Oxford University Press, 2020. ^11 Lanteigne, Marc. “China’s Maritime Security and the ‘Malacca Dilemma’.” Asian Security 4.2 (2008): 143-161. ^12 “European Central Bank Annual Report.” 2023. ^13 Experian PLC. “Annual Report and Financial Statements.” 2023. ^14 Graff, Harvey J. “The Legacies of Literacy: Continuities and Contradictions in Western Culture and Society.” Indiana University Press, 1987. ^15 Khanna, Parag. “The Future is Asian: Commerce, Conflict, and Culture in the 21st Century.” Simon and Schuster, 2019. ^16 “World Bank Data: China.” 2022. ^17 “World Bank Data: United States.” 2022. ^18 “World Bank Data: European Union.” 2022. ^19 “European Commission Trade Statistics.” 2022.

About the author

Jochen Werne is CEO of Experian DACH. Large-scale global data powerhouses like Experian with it’s more than 20.000 data and analytics experts and a market cap of nearly €30bn have a pivotal role to play in this evolving narrative. As a global vanguard in data analytics, Experian is uniquely poised to offer financial institutions the insights and tools essential for navigating the multifaceted challenges of our times. In a world inundated with data, discerning patterns, understanding trends, and anticipating potential pitfalls will be the linchpin of success.

A plea for trust in a time of mistrust. Trust is the foundation on which monetary systems are built. Trust forms the basis of international diplomatic relations and is the foundation for all progress.

But what happens once trust is shaken?

The diplomatic dispute over a multibillion-dollar submarine treaty – which took place three months before the Russian – Ukrainian war, concerns about a new cold war, and the collapse of the Bretton Woods system exactly 50 years ago are the manuscript for this maritime-themed French-American story about money and trust. It is an object lesson for our times, where we are witnessing the emergence of crypto-financial markets and thus stand on the threshold of a new form of money.

TIME OF MISTRUST

by Jochen Werne

After the traditional long summer vacation, France awakens in September from its brief self-created slumber, as it does every year. Life begins to take its usual course, even if some are still reminiscing, perhaps enjoying the first harbingers of post-Covid worry-free life. Not so Philippe Étienne. For him, on the other side of the Atlantic, in Washington, which is actually picturesque at this time of year, autumn begins with a diplomatic thunderstorm. A storm that must have been new even for the 65-year-old gray-haired eloquent ambassador of France. 6160 kilometers away, at the Élysée Palace, Président de la République Emmanuel Macron decides to call his top diplomat in the United States, along with his Australian counterpart Jean-Pierre Thebault, to Paris for consultations. The unprecedented act in Franco-American history is justified by Foreign Minister Jean-Yves Le Drian with the “exceptional gravity” of an Australian-British-American announcement, and impressively underlined with the words “lie,” “duplicity,” “disrespect” and “serious crisis.”

At the heart of this crisis is the surprise announcement by the aforementioned countries to enter into a strategic trilateral security alliance (AUKUS) with immediate effect. An alliance that also provides for the procurement of nuclear-powered submarines for Australia, effectively putting to rest a 56-billion-euro French-Australian submarine order already initiated in 2016. The conclusion of the agreement comes at a time when U.S. President Joe Biden has asserted to the UN General Assembly, “We do not seek – I repeat, we do not seek – a new cold war or a world divided into rigid blocs.” However, experts, such as renowned historian Niall Ferguson, have been talking about this so-called “new cold war” between the U.S. and China since 2019, and it is not about nuclear arms races, but rather about technology supremacy in cyber security, artificial intelligence and quantum computing. Even though nuclear-powered submarines are at the center of the diplomatic dispute, one is quick to note in the AUKUS agreement that cooperation in the aforementioned fields is one of the most important components of the treaty. An objective that is perhaps also congruent with French interests. But the dispute between the old friends is less about the “what” than about the diplomatic “how” – that is, about the breach of trust that is triggered when close allies are simply presented with a fait accompli. Facts that also affect them financially and personally.

Because money and trust are closely interwoven. The trust of a bank that the creditor will repay its debts. A citizen’s trust that the currency in which he or she is paid their salaries is stable. A state’s trust in a currency system that the agreements made there will be honored by all. Georg Simmel, in his “Philosophy of Money,” sums it up this way: “Money is perhaps the most concentrated and pointed form and expression of trust in the social-state order.”

Last year marked the 50th anniversary of another French-American trust-busting melodrama with a maritime backdrop. Benn Steil, senior fellow at the Council on Foreign Relations, describes the moving events of August 6, 1971, in his book, The Battle of Bretton Woods, as follows: “…a congressional subcommittee issued a report entitled ‘Action Now to Strengthen the U.S. Dollar` that concluded, paradoxically, that the dollar needed to be weakened. Dollar dumping accelerated and France sent a warship to pick up French gold from the vaults of the New York Fed.”

At first glance, this dramatic gesture by then French President Georges Pompidou in the final act of the collapse of the Bretton Woods system seems as strange as the withdrawal of ambassadors today. The basis, however, is similar and lay then as now in an equally shaken trust between the great nations that were nevertheless so closely intertwined. Without going deeper into the new monetary order created after World War II, with the U.S. dollar as the anchor currency, it is important to understand the reason for the French revolt evident in the “White Plan.” The plan provided that the U.S. guaranteed the Bretton Woods participating countries the right to buy and sell gold indefinitely at the fixed rate of $35 per ounce. The dilemma of this arrangement became apparent early on. For by the end of the 1950s, dollar holdings at foreign central banks already exceeded U.S. gold reserves. When French President Charles de Gaulle asked the U.S. to exchange French dollar reserves for gold in 1966, the FED’s gold reserves were only enough for about half that amount. The ever more deeply anchored loss of confidence forced the American president Richard Nixon on August 15, 1971 to cancel the nominal gold peg and the so-called “Nixon shock” ended the system as it was.

And where something ends something new can or will inevitably begin.

Today we live in a world where the stability of our currency is based on our confidence in government fiscal policy, the economic strength of our country, and the good work of an independent central bank. However, we also live in a time when new currency systems are already looming on the dense horizon. The basis for this was laid in 2008, not surprisingly, by one of the most serious crises of confidence in the international banking system that modern times have seen. And the new systems are being implemented with the help of cutting-edge distributed ledger blockchain technology. The new, with its decentralized nature, is challenging the old. While many of the new currencies in the crypto world, such as bitcoin, are subject to large fluctuations, stablecoins promise a link and fixed exchangeability to an existing value, such as the US dollar or even gold. However, the old Bretton Woods challenge of being able to keep this promise at all times remains in the new world. Millions of dollars in penalties imposed by the New York Attorney General’s Office on the largest U.S. dollar stablecoin, Tether, for not being fully verifiable do little to help trust, especially when less than 3 percent of the market capitalization is actually deposited in U.S. dollar cash. As always with new ones, trust has to be built up. This can be done privately, perhaps with a stablecoin backed 100% by central bank money, or by the state, with well thought-out central bank digital currencies, such as the digital euro planned by the European Central Bank.

We live in a world of perpetual rapid change and trust is, as Osterloh describes it, “the will to be vulnerable.” Without trust, there are no alliances, no togetherness, no progress.

Philippe Étienne was back in autumnal Washington after just a few days and has since been working again on what diplomats are best trained for – building trust.

Sources

Billon-Gallan, A., Kundnani, H. (2021): The UK must cooperate with France in the Indo-Pacific. A Chatham House expert comment. https://www.chathamhouse.org/2021/09/uk-must-cooperate-france-indo-pacific (Retrieved 24.9.2021)

Brien, J. (2021): “Stablecoin without stability”: Tether and Bitfinex pay $18.5 million fine. URL: https://t3n.de/news/stablecoin-tether-bitfinex-strafe-1358197/?utm_source=rss&utm_medium=feed&utm_campaign=news (Retrieved: 9/30/2021).

Corbet, S. (2021): France recalls ambassadors to U.S., Australia over submarine deal. URL: https://www.pressherald.com/2021/09/17/france-recalls-ambassadors-to-u-s-australia-over-submarine-deal/ (Retrieved 9/25/2021).

Ferguson N. (2019): The New Cold War? It’s With China. And It Has Already Begun. URL: https://www.nytimes.com/2019/12/02/opinion/china-cold-war.html (Retrieved: 9/30/2021).

Graetz, M., Briffault, O. (2016): A “Barbarous Relic”: The French, Gold , and the Demise of Bretton Woods. URL: https://scholarship.law.columbia.edu/cgi/viewcontent.cgi?article=3545&context=faculty_scholarship p. 17 (Retrieved 9/25/2021).

Osterloh, M., Weibel, A. (2006): Investing trust. Processes of trust development in organizations, Gabler: Wiesbaden.

Steil, B. (2020): The Battle of Bretton Woods: John Maynard Keynes, Harry Dexter White, and the new world, p. 377.

Stolze, D. (1966): Does de Gaulle defeat the dollar? In ZEIT No. 36/1966. URL: (https://www.zeit.de/1966/36/besiegt-de-gaulle-den-dollar/komplettansicht (Retrieved: 9/26/2021)

The Guardian Editorial (2021): The Guardian view on Biden’s UN speech: cooperation not competition URL: https://www.theguardian.com/commentisfree/2021/sep/22/the-guardian-view-on-bidens-un-speech-cooperation-not-competition(Retrieved: 9/29/2021)

Unal, B., Brown, K., Lewis, P., Jie, Y. (2021): Is the AUKUS alliance meaningful or merely a provocation – A Chatham House expert comment. URL: https://www.chathamhouse.org/2021/09/aukus-alliance-meaningful-or-merely-provocation (Retrieved: 9/24/2021).

Time Online (2021): France sees relationship in NATO strained. URL: https://www.zeit.de/politik/ausland/2021-09/u-boot-deal-frankreich-australien-usa-streit-nato-jean-yves-le-drian?utm_referrer=https%3A%2F%2Fmeine.zeit.de%2F (Retrieved: 9/25/2021)

Reflections by Jochen Werne, Chief Development & Chief Visionary Officer Prosegur Germany (published in Prosegur Express 02/2021)

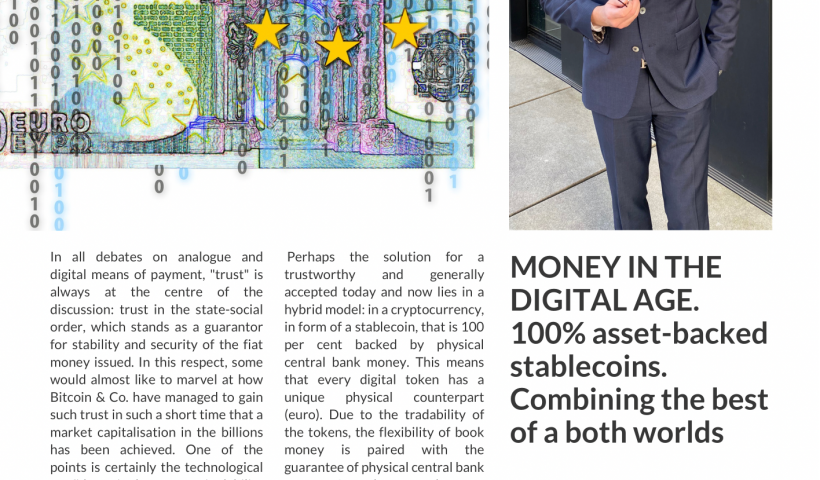

In all debates on analogue and digital means of payment, “trust” is always at the centre of the discussion: trust in the state-social order, which stands as a guarantor for stability and security of the fiat money issued. In this respect, some would almost like to marvel at how Bitcoin & Co. have managed to gain such trust in such a short time that a market capitalisation in the billions has been achieved. One of the points is certainly the technological confidence in the non-manipulability of the blockchain. But is the blockchain really not manipulable, or is it rather a question of time before an attack will succeed? And what conclusions are central banks around the world drawing from this as they look at creating central bank digital currencies? Currencies designed to bridge the gap between the stability of analogue central bank money and the demands of our digital age.

Perhaps the solution for a trustworthy and generally accepted today and now lies in a hybrid model: in a cryptocurrency, in form of a stablecoin, that is 100 per cent backed by physical central bank money. This means that every digital token has a unique physical counterpart (euro). Due to the tradability of the tokens, the flexibility of book money is paired with the guarantee of physical central bank money. Last but not least, a regulated trustee function guarantees that the existing and securely stored central bank money is always paired with its digital twin. Thus. the best of both worlds is firmly united.

It is an honour to be able to support this forward-looking Data Literacy Charter, initiated by the Stifterverband, as a first signatory together with the most competent representatives from politics, education, business and science.

Jochen Werne

DATA LITERACY CHARTA

Find all original information in German > HERE / please find below a translation for English speaking audience – created with DeepL.com

The Data Literacy Charter, initiated by the Stifterverband in January 2021 and supported by numerous professional societies, formulates a common understanding of data literacy and its importance for educational processes. The charter is in line with the Federal Government’s data strategy and with the Berlin Declaration on the Digital Society.

Author and authors: Katharina Schüller, Henning Koch, Florian Rampelt

SUMMARY Data literacy encompasses the data skills that are important for all people in a world shaped by digitalisation. It is an indispensable part of general education.

With the Data Literacy Charter, the signatories express the common understanding of data literacy in the sense of comprehensive data literacy and its importance in educational processes. This understanding is in line with the Federal Government’s data strategy and with the Berlin Declaration on the Digital Society.

Data literacy includes the skills to collect, manage, evaluate and apply data in a critical way. If data is to support decision-making processes, it needs competent answers to four fundamental questions:

What do I want to do with data? Data and data analysis are not an end in themselves, but serve a concrete application in the real world. What can I do with data? Data sources and their quality as well as the state of technical and methodological developments open up possibilities and set limits. What am I allowed to do with data? All legal rules of data use (e.g. data protection, copyrights and licensing issues) must always be considered. What should I do with data? Because data is a valuable resource, a normative claim derives from it to use it for the benefit of individuals and society. The supporters of the Charter see data literacy as a central competence of all people in the 21st century. It is the key to systematically transforming data into knowledge.

Data literacy enables people, businesses and scientific institutions, as well as governmental or civil society organisations,

to actively participate in the opportunities offered by data use; deal confidently and responsibly with their own and other people’s data; to use new drivers and technologies such as Big Data, Artificial Intelligence or Internet of Things to meet individual needs, address societal challenges and solve global problems. Data literacy strengthens judgement, self-determination and a sense of responsibility and promotes the social and economic participation of all of us in a world shaped by digitalisation.

GUIDING PRINCIPLES Five principles characterise the importance and role of data literacy as a key competence of the 21st century.

Data literacy must be accessible to all. Data literacy serves to promote maturity in a modern digitalised world and is therefore important for all people – not only for specialists. The aim of teaching data literacy is to ensure that each individual and our society as a whole deal with data in a conscious and ethically sound manner. Data literacy enables successful and sustainable action that is based on evidence and that takes appropriate account of uncertainty and change in our living environment. We are therefore committed to ensuring that data literacy is taught broadly and can be acquired by all people.

Data literacy must be taught throughout life in all areas of education. Data literacy must be anchored in all formal and non-formal education sectors and thus established as part of general education. To do this, we must continuously teach learners how data relates to their respective lifeworlds: Data are digital images of real phenomena, objects and processes – this applies to all fields of application. How to collect or procure, evaluate, apply and interpret data appropriately for the respective application must be systematically learned and practised. The basic concept of data literacy and its sub-areas therefore applies across the board, even if the level of competence imparted varies depending on the educational sector and level. In concrete terms, this requires the inclusion of data literacy in the curricula and educational standards of schools, in the curricula of degree programmes and in teacher training programmes. Learners should not only be addressed as passive consumers of data. Rather, we want to enable them to actively shape data-related knowledge and decision-making. In order to make lifelong learning of data literacy possible, data literacy programmes for extracurricular and vocational training are also needed. We advocate developing and promoting these, for example, together with adult education centres or public libraries.

Data literacy must be taught as a transdisciplinary competence from three perspectives. Data literacy involves three perspectives: the application-related (“What is to be done?”), the technical-methodical (“How is it to be done?”) and the social-cultural (“What is it to be done for?”). We therefore want to ensure that data literacy is taught from a trans- and interdisciplinary approach. This includes ● the application-oriented perspective (for example, applications from the natural and engineering sciences, economics, medicine, psychology, sociology, linguistics, media studies and many more), the technical-methodological perspective (for example, from the perspective of statistics, mathematics, computer science and information science), the socio-cultural perspective (for example, reflection on legal, ethnological, ethical, philosophical as well as inequality aspects) ● as well as the perspective of teaching (for example on the part of subject didactics and educational science).

Data literacy must systematically cover the entire process of knowledge and decision-making with data. Data literacy ensures that answers to real problems are found with the help of data in a structured and qualitative way. Data literacy therefore includes the following areas of competence: ● Using and protecting data (ability and motivation to responsibly acquire, analyse, share and obtain appropriate data and information in the context of the task at hand). Classify data and information derived from it (ability and motivation to contextualise and interpret data and information and to critically question learning systems, such as AI applications). ● Act in a data-supported manner (open-minded attitude towards data in the sense of a data culture including insight into the role of data for evidence-based action, ability to handle data with confidence including effective communication of data-based decisions).

Data literacy must comprise knowledge, skills and values for a conscious and ethically sound handling of data. Data literacy comprises three competence dimensions that must be mapped in all three competence areas. Each competence area is characterised by ● specific knowledge (dimension “Knowledge”), ● the skills and abilities to apply this knowledge (dimension “Skills”) and ● by the willingness to do so, i.e. the corresponding value attitude (dimension “Values”). Data ethics is a central component of a key competence and is reflected in all sub-areas of data literacy. This means that when data is collected, managed, evaluated and used in a critical way, ethical aspects play an important role throughout. Data ethics and values contribute significantly to ensuring that not only the right means are used to solve problems with the help of data, but above all that the right goals are pursued: Data should make a sustainable positive contribution to society and therefore be used responsibly, context-sensitively and with a view to possible future consequences.

The signatories of the Data Literacy Charter will take measures to disseminate this understanding of data literacy and to further strengthen the associated competences. They call on other actors to do the same in their sphere of influence.

The initial signatories Institutions & Initiatives (in alphabetical order)

Bund Katholischer Unternehmer e.V. (BKU)

Deutsche Arbeitsgemeinschaft Statistik (DAGStat) mit ihren 14 Mitgliedsgesellschaften und dem Statistischen Bundesamt Destatis

Deutscher Volkshochschul-Verband (DVV)

Deutsche Statistische Gesellschaft (DStatG)

Digitalrat der Bundesregierung

Europäisches Wirtschaftsforum e.V. – EWiF Deutschland

Federation of European National Statistical Societies (FENStatS) mit ihren 27 Mitgliedsgesellschaften und der Europäischen Zentralbank

FernUniversität in Hagen

FOM Hochschule für Oekonomie & Management

Hochschulforum Digitalisierung

Initiative for Applied Artificial Intelligence by UnternehmerTUM

Institute of Electrical and Electronics Engineers (IEEE), European Office

International Association for Statistical Education (IASE)

KI Bundesverband e.V.

KI-Campus – Die Lernplattform für Künstliche Intelligenz

Partnership in Statistics for the Development in the 21st Century (PARIS21) / OECD

RWI – Leibniz-Institut für Wirtschaftsforschung

Stifterverband

Technische Universität Dortmund

Weltethos-Institut | An-Institut der Universität Tübingen

Individuals (in alphabetical order)

Regina Ammicht Quinn, Dorothee Bär, Thomas K. Bauer, Manfred Bayer, Jörg Bienert, Felicitas Birkner, Vanessa Cann, Thomas M. Deserno, Roman Dumitrescu, Johanna Ebeling, Florian Ertz, Andrea Frank, Gerd Gigerenzer, Jessica Heesen, Ulrich Hemel, Norbert Henze, Burghard Hermeier, Wolfgang Heubisch, Oliver Janoschka, Johannes Jütting, Claudia Kirch, Volker Knittel, Henning Koch, Ralf Klinkenberg, Annegret Kramp-Karrenbauer, Alexander Knoth, Beate M. Kreiner, Sebastian Kuhn, Monique Lehky Hagen, Andreas Lenz, Andreas Liebl, Anna Masser, Volker Meyer-Guckel, Antje Michel, Ralf Münnich, Dominic Orr, Ada Pellert, Martin Rabanus, Walter J. Radermacher, Philipp Ramin, Florian Rampelt, Richard K. Frhr. v. Rheinbaben, Peter Rost, Philipp Schlunder, Harald Schöning, Katharina Schüller, Rainer Schwabe, Andrea Stich, Sascha Stowasser, Renata Suter, Georges-Simon Ulrich, Daniel Vorgrimler, Jochen Werne, Johannes Winter

The hallmark of an open society is that it promotes the unleashing of people’s critical faculties, and the Data Literacy Charter, in this best sense, promotes the much-needed creation of data literacy for all areas of our digital society

Unlimited availability of our money and its ability to be used as a medium of exchange create certainty and lead to personal freedom. But which payment method is proving to be the most robust in any crisis? A reflection on the value of cash in a free society.

By Jochen Werne, Management Board member, Chief Development & Chief Visionary Officer (CDO/CVO) of Prosegur Cash Services Germany GmbH

In times when our life is being affected significantly by the effects of the situations like the COVID-19 pandemic, we become more aware of the basic needs in our lives. However, the COVID-19 crisis, which hits us globally so hard that we are even prepared to give up some of our civil rights and liberties guaranteed by the constitution, also reveals what certainty means and gives us and what we rely on in order to overcome a crisis and regain our freedom. We live in a world of exponential leaps in technology – and the technological progress has traditionally always resulted in a global improvement in living standards. The international community can be rightly proud of its achievement of reducing the percentage of people who have to live in absolute poverty from 35% to 8% in the last 30 years thanks to global trade. However, it is in times of crisis that we see just how sustainable the goals that have been achieved are. Here prudent and decisive action from political and business leaders is called for. Confidence gained in people and instruments is the greatest asset in times of uncertainty.

Cash: always available

The same applies for payments. While the independent good work over decades of many central banks such as the Deutsche Bundesbank, the European Central Bank and the US Federal Reserve is making itself noticeable in the crisis and the citizens rely on the stability of the euro and US dollar, cash is also showing itself to be an anchor of confidence in uncertain times. With growing concerns due to the coronavirus, in the USA for example the volume of physical cash in circulation has increased. In the week before 25 March this increased by 1.8% to 1.86 trillion dollars in absolute figures. This represents the biggest weekly increase since December 1999, when the fear of the so-called Millennium Bug was the reason for the rise. As we see today, the technological meltdown did not happen. However, 20 years later we are now more aware than ever of the vulnerability of technology and that in times of crisis the value of certainty is always the greatest asset. The increase in demand for cash, including in Germany, at the start of the corona crisis is probably attributable to this legitimate need of citizens for certainty and their great confidence in cash. According to the Bundesbank, the volume on Monday 16 March alone, the first day upon which schools and nurseries were closed, was 0.7 billion euros above the average.

Electronic payment methods, which are essential in so many areas such as online trading for example, repeatedly risk a loss of confidence due to technical failures. One of the most recent of these incidents occurred during of all times the Christmas shopping period on 23 December 2019, when EC card payments were no longer accepted at many terminals. It is a little like the situation described by the Roman poet Ovid: “People are slow to claim confidence in undertakings of magnitude.” Most certainly our savings – the fruit of our labour – are of this magnitude for us. It is for this reason that the availability of our money is so important. If this availability were restricted, we would start to feel that we might no longer be able to access our money, and a bank run would most likely be the result. It is not without reason that the “supply of cash” is expressly defined as a “critical service” in Section 7 of the Regulation on the Identification of Critical Infrastructures (BSI-Kritisverordnung – BSI-KritisV) of the Federal Office for Information Security (BSI). That is to say a “service to supply the general public […], the loss or impairment of which would result in significant supply shortages or risks to public security.”

Certainty in uncertain times

In the COVID-19 crisis, anxiety about health and the economic consequences of any crisis dominate our daily life. While fear is clearly caused by an external threat, anxiety is indeterminate. As the Greek stoic philosopher Epictetus wrote in his Enchiridion of stoic morals: “People are not disturbed by things, but by the view they take of them.” It was therefore also absolutely consistent that the World Health Organization (WHO), the European Central Bank, the Bundesbank and the Robert Koch Institute have been stressing repeatedly in the corona crisis that there is no documented case that would suggest there would be an increased virus risk due to the use of cash as opposed to card payment. They refer here to corresponding scientific studies and underline repeatedly that no information on such a risk has been documented.

Freedom established by the constitution

John Stuart Mill, one of the most successful liberal thinkers of the 19th century, defined freedom as the “first and strongest desire of human nature.” Accordingly, all governmental and social action must be directed towards granting the individual free development, while his freedom, as Mill formulates it in a principle known as the “principle of freedom,” may be limited under one condition: to protect himself or another person. Now, during a serious crisis, all citizens are forgoing some of their fundamental constitutional rights of freedom. This massive intervention is certainly consistent with Mills’ theory in this time of corona. In his novel The House of the Dead, Fyodor Mikhailovich Dostoevsky describes his own experiences of life in a Siberian prison camp and writes the subsequently oft-quoted sentence: “Money is coined liberty,” whereby he describes the vital relevance of a free exchange of goods in an environment where people are deprived of freedom – with cash in the form of coins. Although not in the same way as Dostoevsky, we are also living in a time of extreme change: on a social, economic and political level. We are living in a time when, due to exponential technological developments, whole industries and business models are changing radically and countries are competing for supremacy in areas such as Artificial Intelligence (AI). It is a time in which transformation is the new norm and an agile corporate culture has to be the key to success. It is currently the case in many traditional industries that “anything that can be digitised, will be digitised.” And inevitably this also raises the question of whether this is also the case for the first “instant payment” solution, one of the earliest and longest-lasting achievements of human civilisation – for our cash? Our current free choice of payment method is certainly good, as long as we can choose freely as consumers the payment method appropriate for the respective situation. Discussions about the possible restriction of the freedom of choice of citizens regularly prompt intellectuals to issue warnings. For example, the poet Hans Magnus Enzensberger is of the opinion regarding the issue of “restriction”: “Those who abolish cash, abolish freedom.” This opinion is also shared by Carl-Ludwig Thiele, a former member of the Executive Board of the Deutsche Bundesbank: “Abolishing cash would hurt consumer sovereignty — the free choice of citizens about their payment instruments […] Government agencies do not have the right to tell citizens how they should pay.“

Technological vulnerability, fall-back option and data protection

Particularly in extreme scenarios such as disasters, failures of a digital infrastructure due to cyber attacks, natural events or simply due to technical failure, it is made clear that cash, by its nature, is currently the most robust payment method. The fact that the contactless payment limit has been increased without further ado, for example in supermarkets, at first sounds harmless. However, as a result, anyone can pay for higher-priced goods using a card, and it does not have to be their own card, without any further security checks such as entering a PIN. Everyone has to examine and question critically for themselves the possible consequences of such a payment method. Also not to be disregarded is the issue of data protection. More cashless payments also mean more personal information disclosed by everyone. Data which numerous companies use for commercial purposes. At the latest since the introduction of the EU General Data Protection Regulation (EU GDPR), the sensitivity of the population of Europe with regard to data protection and privacy has been rising gradually. Klaus Müller, Germany’s top consumer protector and Executive Director of the Federation of German Consumer Organisations (vzbv), describes cash as “data protection in practice”. Anyone who pays with cash does not leave any traces to create a consumer profile, purchasing and payment behaviour cannot be manipulated. Cash also helps to protect financial privacy. This was emphasised by Udo Di Fabio, who was a judge of the Federal Constitutional Court for twelve years, at the Cash Symposium 2018 hosted by Deutsche Bundesbank. He explained that every citizen can dispose freely of their money. In his view this freedom would be restricted if financial management were completely digitised.

Smart cash management alleviates the workload of banks

Crises such as the current corona pandemic always bring to light new approaches and act as accelerators of transformation processes that have already been set in motion. With regard to cash-related industries, the banking world has already been in a transformation process for some time. A company such as Prosegur, which, with over 4,000 employees and 31 branches, is a market leader in Germany in the transportation of cash and valuables, is increasingly becoming a full payment-platform provider. Several banks have already taken the path of fully outsourcing their cash management for synergy and cost-saving reasons. Here, cash processes are becoming not only much leaner, but also more cost-effective. This is the case not only for banks, but also for retail customers. With smart machines installed by Prosegur at its customers, cash can be disposed of directly and credited to the customer account on the same day. The smart infrastructure, including dynamic monitoring and forecasting, optimises the logistics and reduces costs in cash logistics. This is the next step towards an efficient, digital and integrated cash management.

Coined Liberty 2.0 and the justification for and rightfulness of cash

In view of the technological progress and the associated social changes, it can be seen that key values from the human perspective are still valid. Based on an intellectual, serious discussion, the relevance to today of the theories of for example Dostoevsky with his experiences in an unfree society is clear: The discussion about the civil rights and liberties of citizens is always very closely related to their ability to use cash freely, to their freedom of choice of payment method and ultimately to the rightfulness of their actions with regards also to effiency and impact. Our open and liberal society is characterised by the fact that we are discussing and most certainly will continue to discuss “Coined Liberty 2.0” at this level.

The Data Literacy Charter, initiated by the Stifterverband in January 2021 and supported by numerous professional societies, formulates a common understanding of data literacy and its importance for educational processes. The charter is in line with the Federal Government’s data strategy and with the Berlin Declaration on the Digital Society.

The Data Literacy Charter, initiated by the Stifterverband in January 2021 and supported by numerous professional societies, formulates a common understanding of data literacy and its importance for educational processes. The charter is in line with the Federal Government’s data strategy and with the Berlin Declaration on the Digital Society. With the Data Literacy Charter, the signatories express the common understanding of data literacy in the sense of comprehensive data literacy and its importance in educational processes. This understanding is in line with the Federal Government’s data strategy and with the Berlin Declaration on the Digital Society.

With the Data Literacy Charter, the signatories express the common understanding of data literacy in the sense of comprehensive data literacy and its importance in educational processes. This understanding is in line with the Federal Government’s data strategy and with the Berlin Declaration on the Digital Society.