Published on 11 January 2023 at Springer Professional – Follow this LINK to original text in German. Translation created with deepL.com

Experts quoted in the article: Stefan Behringer, Leef H. Dierks, Florian Follert, Jochen Werne, Dr. Johannes Winter, Joachim Wurmeling

What distinguishes so-called stablecoins from cryptocurrencies like Bitcoin, Ether & Co? By linking to one or more currencies, this form of digital money forms a bridge to classic FIAT currencies. How this works and where problems lurk is shown in our “Compact explained”.

Stablecoins are digital tokens, assets of private issuers that can also take on money functions. According to Leef H. Dierks, they usually replicate the value of a reserve currency, such as the US dollar, or even a whole bundle of official currencies.

Thus, they do not have to represent a claim on the issuer (the reserve currency) itself, but can also be backed by demand deposits of various currencies, securities or other assets. This so-called peg reduces the volatility of stablecoins compared to classic virtual currencies, such as Bitcoin,” writes the Springer author in the book chapter “Virtual Currencies and Monetary Policy” on page 234.

According to Dierks, stablecoins take on a bridging function to fiat currencies, “especially since, as long as they are backed by legal tender, they do not challenge the currency monopoly of central banks (analogous to bank deposits) at any time”.

Stablecoins make new business models possible

According to a thesis paper by the Landesbank Baden-Württemberg (LBBW) from mid-December 2022, stablecoins do open up new business models. At the same time, however, they are “anything but stable, but are subject to the risk of the holders fleeing from them if there are doubts about their collateralisation”. Digital money may have a negative impact on macroeconomic lending and reduce the influence of central banks on the aggregate money supply. One way to regulate it is to require issuers to hold central bank reserves.

The best-known stablecoin project is Tether, which is pegged one-to-one to the US dollar. “There has been repeated criticism of Tether, so that the company behind the issue has since admitted to using not only currency holdings in US dollars to collateralise the issued units of cryptocurrencies, but also other assets (for example, commercial papers of companies),” Stefan Behringer and Florian Follert describe the background in the book chapter “Controlling of cryptocurrencies” (page 187). This also explains why this stablecoin does not correlate exactly with the performance of the US dollar.

Risks of stablecoins

Jochen Werne and Johannes Winter explain in the book chapter “Cash, book money, cryptocurrencies and the digital euro” on page 84 that there are risks for the financial sector if stablecoins become widespread. They could undermine the banks’ deposit business and their business models. The Springer authors see in the central bank cash-backed stablecoins a possibility of a trustworthy transitional solution in hybrid form. This is a stablecoin that demonstrably holds any digital twin in the form of central bank money.

“Due to the tradability of the tokens, the flexibility of book money is paired with the guarantee of physical central bank money. Even the expected damage from a successful attack on the underlying blockchain could thus be minimised, since an unlawful acquisition of power of disposal over assets is quickly restricted in its usability. A regulated expert function guarantees that only central bank money or a digital twin is traded and thus the central supervisory function always lies with the central bank,” say Werne and Winter.

MiCA forms future legal framework

With the Markets in Crypto Assets (MiCA) regulation, the European Union has sewn a legal garment for the crypto industry in the 26 EU states. The new EU regulation is to enter into force by the beginning of 2023 and become effective 18 months later vis-à-vis all market participants.

“MiCA responds to the growth of the cryptoasset ecosystem and integrates a large number of new players into the European supervisory space,” explains Joachim Wurmeling, member of the Executive Board of the Deutsche Bundesbank, in a guest article on the occasion of the Bundesbank Symposium in November 2022. “In future, crypto service providers and issuers of crypto assets will not only have to ensure that the risks arising from the cryptoasset business are adequately managed; they will also have to apply for authorisation to issue crypto assets or to provide crypto services and be subject to ongoing supervision.”

In addition, he said, the regulation also applies to traditional financial institutions that provide services around cryptoassets. The regulatory approach for MiCA is new and is emerging alongside the traditional structure.

Ein Plädoyer für Vertrauen in einer Zeit des Misstrauens. Vertrauen ist die Grundlage, auf der Währungssysteme aufgebaut sind. Vertrauen bildet die Basis internationaler diplomatischer Beziehungen und ist die Grundlage für jeden Fortschritt.

Doch was passiert, wenn das Vertrauen einmal erschüttert ist?

Der aktuelle diplomatische Streit um einen milliardenschweren U-Boot-Vertrag, die Sorge um einen neuen kalten Krieg und der Zusammenbruch des Bretton-Woods-Systems vor genau 50 Jahren sind das Manuskript für diese maritim angehauchte französisch-amerikanische Geschichte über Geld und Vertrauen. Sie ist ein Lehrstück für unsere heutige Zeit, wo wir das Entstehen von Kryptofinanzmärkten miterleben und somit an der Schwelle zu einer neuen Form des Geldes stehen.

Nach dem traditionellen langen Sommerurlaub, erwacht Frankreich im September wie jedes Jahr aus dem kurzen selbst kreierten Dornröschenschlaf. Das Leben beginnt seinen gewohnten Gang zu nehmen, auch wenn manch einer noch in Erinnerungen schwelgt und dabei vielleicht die ersten Vorboten post-Covid-sorgenfreien Lebens genießt. Nicht so Philippe Étienne. Für ihn beginnt auf der anderen Seite des Atlantik, im für diese Zeit eigentlich malerischen Washington, der Herbst mit einem diplomatischen Gewittersturm. Ein Unwetter, das selbst für den 65-jährigen grau-melierten eloquenten Botschafter Frankreichs neu gewesen sein dürfte. 6 160 Kilometer entfernt beschließt im Élysée-Palast Président de la République Emmanuel Macron seinen Spitzendiplomaten in den USA, samt seines australischen Amtskollegen Jean-Pierre Thebault, zu Konsultationen nach Paris abzuberufen. Der in der französisch-amerikanischen Geschichte einmalige Akt wird von Außenminister Jean-Yves Le Drian mit der „außergewöhnlichen Schwere“ einer australisch-britisch-amerikanischen Ankündigung gerechtfertigt und mit den Worten „Lüge“, „Doppelzüngigkeit“, „Missachtung“ und „ernste Krise“ eindrucksvoll unterstrichen.

Im Mittelpunkt dieser Krise steht die überraschende Ankündigung der genannten Länder ab sofort ein strategisches trilaterales Sicherheitsbündnis (AUKUS) einzugehen. Ein Bündnis, welches auch die Beschaffung atomgetriebener U-Boote für Australien vorsieht und somit einen bereits 2016 initiierten 56 Milliarden Euro schweren französisch-australischen U-Boot- Auftrag quasi ad acta legt. Der Abschluss des Abkommens fällt in einen Zeitraum in welchem US-Präsident Joe Biden vor der UN-Generalversammlung beteuert: „Wir streben nicht – ich wiederhole: wir streben nicht – einen neuen kalten Krieg oder eine in starre Blöcke geteilte Welt an“. Über diesen sogenannten „neuen kalten Krieg“ zwischen den USA und China sprechen Experten, wie der bekannte Historiker Niall Ferguson jedoch bereits seit 2019. Es geht hierbei nicht um atomares Wettrüsten, sondern vielmehr um die Technologievorherrschaft in Cyber Security, Künstlicher Intelligenz und Quantum Computing. Auch wenn nukleargetriebene U-Boote im Zentrum des diplomatischen Disputs stehen, so stellt man im AUKUS-Abkommen doch schnell fest, dass die Zusammenarbeit in den oben genannten Feldern einer der wichtigsten Bestandteile des Vertrags ist. Ein Ziel, welches vielleicht auch mit französischen Interessen kongruent ist. Doch geht es im Streit zwischen den alten Freunden im ersten Moment weniger um das „Was“, sondern viel mehr um das diplomatische „Wie“ – das heißt, um den Vertrauensbruch, der ausgelöst wird, wenn man enge Bündnispartner einfach vor vollendete Tatsachen stellt. Tatsachen, die sie auch finanziell und persönlich betreffen.

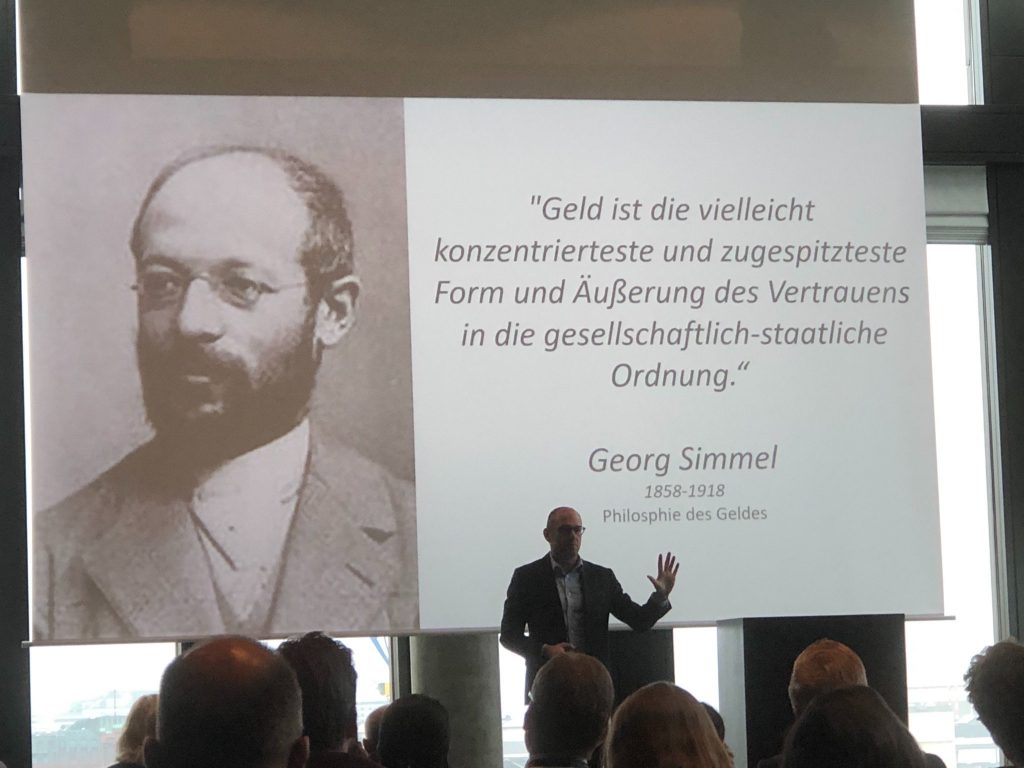

Denn Geld und Vertrauen sind eng verwoben. Das Vertrauen einer Bank, dass der Gläubiger seine Schulden zurückbezahlt. Das Vertrauen eines Bürgers, dass die Währung, in der er oder sie ihre Gehälter ausbezahlt bekommt, stabil ist. Das Vertrauen eines Staates in ein Währungssystem, dass die dort getroffenen Vereinbarungen von allen eingehalten werden. Georg Simmel bringt es in seiner „Philosophie des Geldes” so auf den Punkt: „Geld ist die vielleicht konzentrierteste und zugespitzteste Form und Äußerung des Vertrauens in die gesellschaftlich-staatliche Ordnung.“

Eine weiteres französisch-amerikanisches Vertrauensbruchsmelodrama mit maritimer Untermalung jährt sich in diesem Jahr zum 50. Mal. Die bewegenden Ereignisse des 6. August 1971 beschreibt Benn Steil, Senior Fellow des Council on Foreign Relations, in seinem Buch „The Battle of Bretton Woods“ wie folgt: „…ein Unterausschuss des Kongresses gab einen Bericht mit dem Titel ´Action Now to Strengthen the US-Dollar` heraus, der paradoxerweise zu dem Schluss kam, dass der Dollar geschwächt werden müsse. Das Dollar-Dumping beschleunigte sich und Frankreich schickte ein Kriegsschiff, um französisches Gold aus den Tresoren der New Yorker Fed abzuholen.“

Diese dramatisch anmutende Geste des damaligen französischen Präsidenten Georges Pompidou im finalen Akt des Zusammenbruchs des Bretton-Woods Systems wirkt auf den ersten Blick genauso befremdlich wie der Abzug der Botschafter heute. Die Basis jedoch ähnelt sich und lag damals wie heute in einem ebenfalls erschütterten Vertrauen zwischen den doch so eng verwobenen großen Nationen. Ohne tiefer auf die nach dem Zweiten Weltkrieg geschaffene neue Währungsordnung mit dem US-Dollar als Ankerwährung eingehen zu wollen, ist es wichtig den im „White Plan“ offensichtlichen Grund des französischen Aufbegehrens zu verstehen. Der Plan sah vor, dass die USA den Bretton-Woods-Teilnehmerstaaten garantierten, Gold auf unbestimmte Zeit zum festen Kurs von 35 US-Dollar pro Unze kaufen und verkaufen zu dürfen. Das Dilemma dieser Regelung wurde früh sichtbar. Denn bereits Ende der 1950er Jahren überstiegen die bei ausländischen Zentralbanken befindlichen Dollarbestände die Goldreserven der USA. Als der französische Präsident Charles de Gaulle 1966 die USA aufforderte die französischen Dollarreserven gegen Gold zu tauschen, reichten die Goldvorräte der FED, nur für etwa die Hälfte. Der immer tiefer sich verankernde Vertrauensverlust zwang den amerikanische Präsidenten Richard Nixon am 15. August 1971 die nominale Goldbindung aufzukündigen und der sogenannte „Nixon-Schock“ beendete das System wie es war.

Und dort wo etwas endet kann oder wird zwangsläufig etwas Neues beginnen.

Heute leben wir in einer Welt, in der die Stabilität unserer Währung auf unserem Vertrauen in die staatliche Finanzpolitik, der Wirtschaftskraft unseres Landes und auf der guten Arbeit einer unabhängigen Zentralbank beruht. Wir leben jedoch auch in einer Zeit in der sich am dichten Horizont bereits neue Währungssysteme abzeichnen. Die Basis dafür legte 2008 nicht überraschend eine der schwersten Vertrauenskrisen in das internationale Bankensystem, die die Neuzeit erlebete. Und umgesetzt werden die neuen Systeme mit Hilfe modernster Distributed-Ledger Blockchain Technologie. Das Neue mit seinem dezentralen Charakter fordert das Alte heraus. Während viele der neuen Währungen in der Kryptowelt, wie etwa der Bitcoin, großen Schwankungen unterworfen sind, versprechen Stablecoins eine Bindung und fixe Umtauschbarkeit an einen vorhandenen Wert, wie beispielsweise den US-Dollar oder auch Gold. Die alte Bretton-Woods-Herausforderung, dieses Versprechen auch jederzeit einhalten zu können, bleibt jedoch auch in der neuen Welt bestehen. Von der New Yorker Generalstaatsanwaltschaft verhängte Strafen in Millionenhöhe gegen den größten US-Dollar Stablecoin Tether wegen nicht lückenloser Nachweisbarkeit helfen dem Vertrauen wenig, besonders wenn weniger als 3 Prozent der Marktkapitalisierung auch wirklich in US-Dollar Cash hinterlegt ist. Es gilt wie immer bei neuem, Vertrauen aufzubauen. Sei es privatwirtschaftlich durch eventuell einen zu 100% mit Zentralbankgeld hinterlegten Stablecoin oder staatlich, mit durchdachten Central Bank Digital Currencies, wie dem von der Europäischen Zentralbank geplanten digitalen Euro.

Wir leben in einer Welt immer währenden schnellen Wandels und Vertrauen ist, wie Osterloh es beschreibt, „der Wille sich verletzlich zu zeigen“. Ohne Vertrauen gibt es keine Bündnisse, kein Miteinander, keinen Fortschritt.

Philippe Étienne war bereits nach ein paar Tagen zurück im herbstlichen Washington und arbeitet seither wieder daran wofür Diplomaten bestens ausgebildet sind – Vertrauen zu schaffen.

Interview mit Jochen Werne, CDO/CVO Prosegur Germany, zu effizienteren Prozessen nach dem Lockdown

In seinem Experten-Interview beleuchtet Jochen Werne zentrale Aspekte aus Sicht von Gastronomie und Handel für effizientere Prozesse nach dem Lockdown

Publiziert von Prosegur Deutschland: LINK HIER

Herr Werne, was sind Ihre persönlichen Beobachtungen in Bezug auf Wirtschaft und Gesellschaft nach einem Jahr der Krise?

Jede Krise bringt natürlich zunächst einmal Leid mit sich und eine Pandemie selbstverständlich Leid für den Einzelnen und seine Angehörigen, wenn ihn das Schicksal, der durch das Virus ausgelösten Krankheit ereilt. Alles Weitere ist wie eine Kettenreaktion. Beginnend vom Staat, der die hoheitliche Aufgabe hat seine Bürger zu schützen und dies im Falle einer Pandemie auch mit dem Herunterfahren des gesellschaftlichen Lebens durchsetzt. Dies wiederum hat bei geschlossenen Unternehmen die Folge drastischer Einkommenseinbußen bei weiterlaufenden Kosten. Bei nicht ausreichender Liquidität führt dies dann zu Insolvenzen, Arbeitsplatzverlusten und im schlimmsten Fall zu einer Wirtschaftskrise. Geschichtlich gesehen hat jedoch auch jede Krise – und diese ist keine Ausnahme – dazu geführt, dass die Wirtschaft effizienter wird und technologische Trends eine Beschleunigung erfahren.

Im Moment – in dieser für viele so schwierigen Situation – beobachte ich eine unglaubliche und inspirierende Kreativität. Sie beginnt bei den kleinen und mittelständischen Unternehmen, die sich versuchen agil, der gefühlt täglich neuen Lage anzupassen, sich zu verbessern, Kosten zu optimieren und sich optimal für die Zeit nach der Krise aufzustellen. Das stimmt hoffnungsfroh für die Zeit nach der Krise und es ist eine große Motivation mit einem fantastischen Team den eigenen Teil dazu beitragen zu können.

Jede Krise fordert von Unternehmen eine gewisse Resilienz.Die nationale Akademie der Technikwissenschaften (acatech), hat zum Digitalgipfel der Bundesregierung im November ein Impulspapier mit dem Titel „Resiliente Vorreiter“ vorgestellt. Darin wird Prosegur mit deiner digitalen Smart Cash Lösung als Best Practice Besipiel für ein zukunftsgerichtetes und kostenoptiertes Cash Managment für den Handel und die Gastronomie genannt. Wie funktioniert Prosegur Smart Cash?

Mit Prosegur Smart Cash können Gastronomen, Einzel- oder Großhändler Bargelder zur sicheren Verwahrung direkt in das Smart Cash Gerät einführen. Das Besondere – im Gegensatz zu einem einfachen Tresor ist es, dass einmal eingeführt, das Gerät automatisch das tägliche Zählen und Abrechnen des Bargeldes übernimmt. Die Zeit- und somit Kostenersparnis in den internen Prozessen bei unseren Kunden ist teilweise beträchtlich. Das Gerät verfügt über ein Kommunikationsprotokoll, das die Überweisung des Wertes der Abholung auf das Bankkonto des Kunden innerhalb von 24 Stunden ermöglicht. Sobald sich das Geld im Gerät befindet, liegt die Verantwortung und Verwaltung bei dem spezialisierten Team von Prosegur Cash, das für den Transport und die Verwahrung des Geldes zur Bankfiliale verantwortlich ist. Somit entfällt auch der teilweise tägliche und nicht ungefährliche Gang zur Bankfiliale.

Was sind die Vorteile von Prosegur Smart Cash?

Zusammengefasst spart es unseren Kunden Zeit und Geld und schafft mehr Transparenz und Sicherheit. Die Kunden von Prosegur Smart Cash können ihr Bargeld schnell und sicher aufbewahren und so unbekannte Verluste reduzieren. Prosegur Smart Cash ermöglicht eine Zeitersparnis durch die Automatisierung des Zählens und bei der täglichen Abrechnung des Bargeldes. Darüber hinaus muss der Kunde dank Prosegur Smart Cash nicht zur Bank gehen, um das Bargeld einzuzahlen, da Prosegur für die Sicherheit bei der Verwaltung und Übergabe des gesamten Bargelds an die Bank sorgt, was gefährliche Situationen für den Kunden vermeidet und ihm hilft, Zeit zu sparen, damit er sich voll und ganz seinem Geschäft widmen kann. Außerdem reduziert eine Smart Cash Lösung das häufige und teure Phänomen des sogenannten „unbekannten Verlustes“.

Was ist „Unbekannter Verlust“?

Jochen Werne: Hierbei handelt sich um den Verlust von Inventar oder anderen Geschäftsressourcen, der auf eine Vielzahl von Faktoren zurückzuführen ist, wie z. B. interner und externer Diebstahl, Verwaltungsversagen, Betrug oder Fehler im Cashflow. Diese Situation stellt für Gastronomen und Einzelhändler oftmals ein zentrales Problem dar.

Was beobachten Sie, in Bezug auf ihre Kunden und wie sich diese auf die Zeit nach dem Lockdown vorbereiten?

Jochen Werne: Es ist eine unglaubliche Sehnsucht zu beobachten, endlich wieder mit seinen Kunden in Kontakt treten zu dürfen, um Ihnen wieder leidenschaftlich die eigenen Leistungen und Services bieten zu dürfen. Viele Kleine und mittelständische Unternehmen, von den großen ganz abgesehen, haben massiv in Hygienekonzepte investiert und versucht die Zeit zu nutzen um die eigenen Prozesse zu kostenoptimieren.

Wir selbst haben noch nie so viele Beratungsgespräche in Bezug auf smarte Bargeldlösungen geführt wie heute. Dies hat sich noch einmal erhöht, nachdem deutliche Aussagen und Studien der Weltgesundheitsorganisation (WHO) und der Bundesbank darauf hinwiesen, dass die hygienische Sauberkeit vom Bargeld mindestens gleich dem von Kartenzahlungen ist und eine Ansteckungsgefahr in Bezug auf unsere täglichen Bezahlmethoden in beiden Fällen geringst ist.

Interessanterweise haben wir auch eine hohe Nachfrage nach Effizienzhebung bei Unternehmen mit kleinem Bargeldaufkommen festgestellt und die Zeit genutzt um als erstes Unternehmen in Deutschland auch für diese Gruppe eine entsprechende sehr kostengünstige digitalte Lösungen zu entwickeln. Eine Krise zwingt immer alle effizienter zu werden und es gibt meiner Meinung nach nichts besseres, als dies gemeinsam zu tun. Nur so schafft man es gemeinsam aus einer Krise gestärkt hervor zu gehen.

Does cash have a future? An article by Dunja Koelwel, editor in chief of gi Geldinstitute | 20.10.2020 – 13:02

Please follow this LINK for the original source in German. Translation made by DeepL.com

Cashless payment is on the advance worldwide, only the Germans hang on to cash. gi Geldinstitute therefore wanted to know from Ralf-Christoph Arnoldt (Bundesverband der Deutschen Volksbanken und Raiffeisenbanken BVR), Jochen Werne (Prosegur Germany), Dr. Harald Olschok (BDSW) and Leif Wienecke (Solarisbank) Does cash still have a future?

Signs such as “Cash only” should be a thing of the past in Germany, according to the digital association Bitkom. Wherever customers can pay, at least one digital payment option that can be used throughout Europe should be offered on a mandatory basis, according to the “Bitkom theses on freedom of choice in payment”.

“Cash shows itself to be an anchor of trust in uncertain times. With increasing concern about the corona virus, the amount of physical cash in circulation in the USA, for example, has risen,” says Jochen Werne, member of the management of Prosegur Cash Services Germany. gi geldinstitute therefore asked: What is the current situation regarding ‘war on cash’?

Since the Corona crisis, more and more people have been paying with cards or smartphones instead of with coins or notes. Is this a trend that is slowly eliminating cash? What is your perception?

Ralf-Christoph Arnoldt: Indeed, in recent months we have seen gains in card payments, especially in payments with Girocard. In the first half of 2020, transaction figures have increased by 20.7 percent compared to the same period last year. However, cash still plays an important role in everyday life in Germany, even if this love is eroding.

According to the Eurohandelsinstitut (EHI), the share of cash in turnover in 2019 was still 45.5 percent. Cash offers some advantages from the customer’s point of view. Paying with cash is convenient for the customer, anonymous, immediately final. Cash is freedom for customers. Regulators and business circles involved in the cash circle should accept this as a fact and not force them to change it.

Dr. Harald Olschok: Without doubt, a new phase of “war on cash” began during the Corona crisis. 75 percent of the member companies of the BDGW expect sales next year to be up to 20 percent lower than in the past. We assume that the proportion of cash payments in the retail sector will fall from around 48 percent at the beginning of 2020 to well below 40 percent. However, the crisis has also shown that Germans continue to have great confidence in cash as a secure means of payment and store of value. According to a survey by YouGov, Germans also cannot imagine living in a cashless society.

Leif Wienecke: Since the Corona crisis, we have seen an acceleration of many trend developments, some of which were already foreseeable before. This also includes contactless payment. This customer behaviour, which is relatively new in Germany, fits in well with corona-related hygiene measures. Basically, it can be said that, in addition to hygiene considerations, end customers are primarily looking for speed when choosing a means of payment. This is where digital and contactless payment methods come into play. Over the next few years, we will see a further decline in cash payments and an increasing use of digital payment methods such as mobile wallets.

Jochen Werne: What is important to people when it comes to their money – the “fruits of their labour”? Certainly its unlimited availability. If they can have confidence that they can get their money at any time, people choose the payment option that is most convenient for each individual. Some prefer to pay by smartphone, while for others it’s “only cash is true”. It is fundamental that we as consumers are free to decide from which means of payment we can freely choose. Freedom of choice is the key word.

A “per cash” argument often made is that technology is vulnerable and that in a crisis the value of security is always the highest good. This is why many people have been hoarding cash at the beginning of the lockdown. Do you believe that this money will now come back into circulation? And what do you think about the technological error potential of digital payment options?

Ralf-Christoph Arnoldt: The fact that cash was hoarded at the beginning of the lockdown was more due to the fact that people thought the cash supply could be endangered because of the Corona crisis. But that quickly proved to be incorrect. In the meantime, the hoardings have been continuously disbanded. We can see this, among other things, in the fact that the payout volumes at ATMs are still about 25 percent below the pre-corona level. If you want to compare the security of cash with card payments or digital payment options, you don’t get very far. If cash is stolen, for example, it is gone for good. If a payment card is stolen, the bank is usually liable.

Jochen Werne: It is undeniable that cash is seen by many as an anchor of trust in uncertain times. Electronic payment methods always risk a loss of trust due to technical failures. One of the last of these incidents was not long ago: during the pre-Christmas business on 23 December 2019, of all days, EC card payments were not accepted at many terminals. Many consumers who rely solely on digital payments have probably already had similar experiences of lesser consequence. Such situations can be observed time and again at the cash desks in department shops and supermarkets – for example, when the NFC chip on a card or simply the card reader does not work. Soon the eyes of the people standing around in the shopping queue turn to the payer, impatient and interested, trying to find out the name on the card of the supposedly insolvent unlucky person. Nevertheless, modern technologies are becoming more and more stable over time and a balance will be established between the various payment methods. Just as the “hoarded” will be returned to consumption or investment after the crisis. A cycle that, soberly, has always existed historically.

It became apparent that banks would no longer be able to offer free cash withdrawals from ATMs in the long term. This affects in particular people on low incomes, the elderly and, in general, all those who do not have access to digital forms of payment. Which solution do you think makes the most sense?

Leif Wienecke: Indeed, an accelerated dismantling of bank branches has been observed in recent months, but also before. The cost-benefit ratios seem to be out of proportion. Many end customers, especially older people, are suffering as a result. At the same time, however, one can also read about the creative solutions that savings banks, for example, are using to offer customers in rural areas the service they are used to (e.g. branch on wheels, transfer bus). I believe that other companies will fill the gap left by the banks. For some years now, supermarkets and petrol stations, for example, have been offering free “withdrawal” of cash. This trend to integrate banking services into the context of everyday life is known as contextual banking. The end customer wants to have access to cash or transactions wherever he or she is. As Solarisbank, we see the future in banking here.

Jochen Werne: Making an individual’s assets available as cash causes costs, just as paying with a card costs consumers money. The latest evaluation of 294 account models of 125 credit institutions in Germany by Stiftung Warentest shows that 55 models already charge fees for payment with the Girocard. It is the task of the institutions not only to manage their customers’ money, but also to meet the customer’s wish to make these assets available to them again in the form of cash or book money. The current practice of offering cash or accounts without fees and cross-subsidising them in return is a German phenomenon. The former head of BaFin, Dr. Elke König, already raised the question critically more than five years ago at the “Bank of the Future” event.

Today’s pressure on margins at banks now demands this adjustment. It is undisputed that, according to the German Bundesbank, ATMs are the most popular source of cash, accounting for 84 per cent of all cash withdrawals. Their number has risen by a good 18 per cent in Germany in recent years. On average, there is one ATM per 1,415 inhabitants. ATMs are therefore of enormous social and economic importance. It is not surprising that the area of “cash supply” is expressly listed as a “critical service” in Section 7 of the Critical Service Ordinance of the Federal Office for Information Security (BSI-KritisV), as a “service for the supply of the general public (…), the failure or impairment of which would lead to considerable supply bottlenecks or to threats to public security”. The fact that banks have to provide cash and cards to their customers, but are generally not able to do so profitably without charging is a long-term problem and needs to be improved. However, there is room for debate as to whether charges are the right way forward for consumers.

For US economics professor Kenneth Rogoff, the abolition of large banknotes is a first step. According to Rogoff, cash is synonymous with crime and the shadow economy – and in this respect it is a threat to the general public. Is cash really more “crime-sensitive” than digital payment methods?

Dr. Harald Olschok: As a “learned” Freiburg economist, I am always appalled by the populist and simplistic theses of the former chief economist of the IMF. It is much worse than you suggest. For Rogoff, “there is no question that cash plays a vital role in criminal activities, including drug trafficking, organised crime, extortion, corruption of authorities, trafficking in human beings and money laundering. (Der Fluch des Geldes, Munich 2016, p. 11). Oh yes, and undeclared work and illegal immigration are also owed to cash. Unfortunately, it has also been heard in the euro area. The 500 euro banknote has already been abolished. At the heart of the Rogoffian theses is the abolition of cash in order to impose negative interest rates. People should not save, but spend their money. This ignores the fact that fraud with non-cash means of payment, such as crypto-currencies, is booming. I expect that these forms of fraud will continue to increase. We must therefore assume the opposite.

Ralf-Christoph Arnoldt: Passing on a USB stick with millions of dollars in crypto-currencies, for example, is as easy as passing on a banknote. Criminals and the black economy are also part of the trend towards digitalisation, unfortunately sometimes even ahead of the investigating authorities.

Leif Wienecke: There is a lot of discussion on this topic and also conflicting studies. The Federal Government’s decision to tighten the reporting requirements for notaries, for example in real estate transactions, underlines Rogoff’s thesis. Nevertheless, I believe that it is not possible to generalise. Certainly, the anonymity of cash brings some advantages for criminals and money laundering can be curbed by switching to more strongly regulated, digital payment procedures.

And what about security? With cash, the problem is counterfeiting, with digital payments, for example, the tapping of identities and data. What is easier to protect?

Ralf-Christoph Arnoldt: I don’t see a big difference. It is always a mutual arms race. New security features for cash require more know-how and greater investment for counterfeiters. It is becoming more difficult, the number of offenders is getting smaller, but the sums that a counterfeiter puts on the market are bigger. The situation is similar for digital payments. As a financial group, we are doing everything we can to stay one step ahead of criminals through new cryptographic procedures, hardened systems and so on. It is not without reason that our experts are already working on cryptographic solutions that will be able to withstand the coming era of quantum computers. The challenge here is to maintain the convenience for the customers.

Jochen Werne: By its very nature, cash is without doubt the most robust payment method. This is regularly demonstrated in extreme scenarios such as disasters, failure of a digital infrastructure due to cyber attacks, natural disasters or technical failure. Cash is not tied to electricity, digital infrastructure, passwords or other technical features. In addition, the introduction of the second series of euro banknotes has enhanced security features and made banknotes more secure and more counterfeit-proof. As the Bundesbank reported at the beginning of the year, the number of counterfeit banknotes has fallen by a further five percent. With digital payment methods, consumers themselves have a responsibility to protect themselves. At the beginning of the Corona crisis, for example, the payment limit for contactless payments, such as in supermarkets, was increased. At first glance, this sounds harmless. But as a result, anyone can use a card – and it does not have to be their own – to pay for higher-priced goods without further security checks, such as by entering a PIN. And as far as data protection is concerned: with every cashless payment, consumers disclose personal information. Data that many companies use commercially.

Dr Harald Olschok: The risk of coming into contact with counterfeit money in Germany is still low. Most counterfeits are easy to detect. The security features of the current Euro series make it difficult for criminals. However, if digital payment methods are attacked, consumers should be aware that they lose much more than just their money.

China wants to take a step in this direction from 2021 onward at the state level as well. The aim is to link the Alipay payment solution with all private and state databases, including those in which cashless payment transactions are stored. The aim is to record and evaluate consumer behaviour. Subsequently, either rewards are offered or sanctions are threatened. Anyone who accumulates too much debt or fails to pay it back is no longer allowed to use express trains or planes in China. Although such a development is completely out of the question in European democracies in the foreseeable future, do you also expect consumer behaviour to play a much greater role in credit rating in the future?

Jochen Werne: Harvard history professor Niall Ferguson coined the term “new cold war” over a year ago. This “Cold War” is mainly about one technology leadership in artificial intelligence and takes place between the United States and China. Technologies are not good or bad, but how and for what purpose they are used by us humans, determines the outcome. Just because something is now technically possible, it does not necessarily make sense for a society. It is a great value of liberal democracies that these issues are discussed, that privacy is protected and that the state cannot act on its own authority.

On the question of creditworthiness, it can be said that the better a credit institution knows the borrower, the better a risk assessment can be made in order to quantify credit default risks. When assessing creditworthiness, the institution is required to use all relevant and available data for the decision. Today, it is technically possible to enrich the data provided by the future borrower with information about him/her from the Internet and social media and to round off the data with the help of AI algorithms and peer group comparisons. However, there is a high risk that private personal data may be processed here if inadvertently and the protection of privacy may be violated. This must be prevented. However, it remains to be seen how this will be dealt with in the future.

Leif Wienecke: First and foremost, it is a matter of making sensible use of the many possibilities of generated data to create added value. Companies such as banks primarily face the challenge of preparing their customers’ data in a meaningful way and integrating it for new applications. The ecosystems of the “GAFAs” or Alipay are “data first” companies which are integrated into the everyday life of their users. In principle, they only make decisions based on data and empirical findings. The above description from China, however, does not go hand in hand with our understanding of data or consumer protection, so we do not see this coming either.

On the other hand, it is of course essential to pursue data-driven innovation. Even the credit rating system that exists today can certainly be extended via relevant, contextual data points, in the interests of consumers and credit institutions. The topic of “social scoring”, i.e. the use of customer data from social networks, is controversial in Germany and is discussed above all in the context of consumer protection. This is correct, because the consumer should not only have to give his consent for such scoring, but should also be able to understand the algorithm and complain in case of discrimination.

Recently, initiatives have been heard repeatedly to make a CBDC (Central Bank Digital Currency) accessible to all citizens and not to limit an e-euro to institutional participants in the financial markets. What do you think about this?

Leif Wienecke: The CBDC issue is still in its infancy and has many facets. It is mostly about increasing the efficiency of payment transactions. End customers also benefit from this. In principle, innovation processes and initiatives to transform the financial industry are to be seen as positive. As with all topics with a European or international scope, it is important to create a uniform regulatory framework. Precisely because the introduction of a digital central bank currency for the public would not be accompanied by a change in the existing monetary system. At Solarisbank, we have been dealing with the block chain and crypto currency industry for over two years. Last year, we founded the subsidiary Solaris Digital Assets to realise our vision of the broad use of digital assets.

Ralf-Christoph Arnoldt: Unfortunately, very different things are mixed up here. Firstly, there is the technology on which most crypto currencies are based: the block chain. It is highly interesting because rights (to money, benefits from contracts, etc.) can be transferred securely and traceably. This technology has its use cases and will increase in importance. To issue a currency based on this digital solution is certainly forward-looking but not without risks. The speed with which sums of money can be transferred would in itself increase the speed at which money circulates to an extent at which we lack economic experience. Questions also remain to be answered about the security of the currency and who is responsible for the counter-value. It is therefore to be welcomed that we are dealing with this issue at an early stage so that we can learn with manageable and calculated risk.

The concept of the euro, on the other hand, suggests a digital currency as a means of payment. In my view, it is still too early for that. Not only because the overall economic effects can only be estimated to a limited extent at present, but also because this technology is geared to the security and distribution of data, not to transaction efficiency. The number of transactions is technically limited. There are concepts such as the Lightning technology to circumvent this and allow more transactions. However, the latter again functions as an intermediary according to principles similar to those of traditional payment transactions. Transactions are executed and then “booked” in the block chain – similar to a central bank transfer.

Likewise, too little attention is paid to the ecological aspect. According to estimates, Bitcoin alone consumed around 74 terawatt hours in one month at the end of 2019. By way of comparison, Germany’s total electricity consumption over the same period was around 47 terawatt hours.

And now the crucial question at the end: How do you make cashless payments?

Ralf-Christoph Arnoldt: With the Girocard – as far as possible contactless of course, and with pleasure also by mobile phone.

Leif Wienecke: I use Google Pay with my debit cards from our partners Tomorrow, Vivid Money and Bitwala. Offline I use the corresponding Visa cards. And online I also use PayPal.

Jochen Werne: Of course with cash and cashless.

Dr. Harald Olschok: In food retailing and gastronomy regularly with cash. For larger expenses, including refuelling, with credit cards.

Unlimited availability of our money and its ability to be used as a medium of exchange create certainty and lead to personal freedom. But which payment method is proving to be the most robust in any crisis? A reflection on the value of cash in a free society.

By Jochen Werne, Management Board member, Chief Development & Chief Visionary Officer (CDO/CVO) of Prosegur Cash Services Germany GmbH

In times when our life is being affected significantly by the effects of the situations like the COVID-19 pandemic, we become more aware of the basic needs in our lives. However, the COVID-19 crisis, which hits us globally so hard that we are even prepared to give up some of our civil rights and liberties guaranteed by the constitution, also reveals what certainty means and gives us and what we rely on in order to overcome a crisis and regain our freedom. We live in a world of exponential leaps in technology – and the technological progress has traditionally always resulted in a global improvement in living standards. The international community can be rightly proud of its achievement of reducing the percentage of people who have to live in absolute poverty from 35% to 8% in the last 30 years thanks to global trade. However, it is in times of crisis that we see just how sustainable the goals that have been achieved are. Here prudent and decisive action from political and business leaders is called for. Confidence gained in people and instruments is the greatest asset in times of uncertainty.

Cash: always available

The same applies for payments. While the independent good work over decades of many central banks such as the Deutsche Bundesbank, the European Central Bank and the US Federal Reserve is making itself noticeable in the crisis and the citizens rely on the stability of the euro and US dollar, cash is also showing itself to be an anchor of confidence in uncertain times. With growing concerns due to the coronavirus, in the USA for example the volume of physical cash in circulation has increased. In the week before 25 March this increased by 1.8% to 1.86 trillion dollars in absolute figures. This represents the biggest weekly increase since December 1999, when the fear of the so-called Millennium Bug was the reason for the rise. As we see today, the technological meltdown did not happen. However, 20 years later we are now more aware than ever of the vulnerability of technology and that in times of crisis the value of certainty is always the greatest asset. The increase in demand for cash, including in Germany, at the start of the corona crisis is probably attributable to this legitimate need of citizens for certainty and their great confidence in cash. According to the Bundesbank, the volume on Monday 16 March alone, the first day upon which schools and nurseries were closed, was 0.7 billion euros above the average.

Electronic payment methods, which are essential in so many areas such as online trading for example, repeatedly risk a loss of confidence due to technical failures. One of the most recent of these incidents occurred during of all times the Christmas shopping period on 23 December 2019, when EC card payments were no longer accepted at many terminals. It is a little like the situation described by the Roman poet Ovid: “People are slow to claim confidence in undertakings of magnitude.” Most certainly our savings – the fruit of our labour – are of this magnitude for us. It is for this reason that the availability of our money is so important. If this availability were restricted, we would start to feel that we might no longer be able to access our money, and a bank run would most likely be the result. It is not without reason that the “supply of cash” is expressly defined as a “critical service” in Section 7 of the Regulation on the Identification of Critical Infrastructures (BSI-Kritisverordnung – BSI-KritisV) of the Federal Office for Information Security (BSI). That is to say a “service to supply the general public […], the loss or impairment of which would result in significant supply shortages or risks to public security.”

Certainty in uncertain times

In the COVID-19 crisis, anxiety about health and the economic consequences of any crisis dominate our daily life. While fear is clearly caused by an external threat, anxiety is indeterminate. As the Greek stoic philosopher Epictetus wrote in his Enchiridion of stoic morals: “People are not disturbed by things, but by the view they take of them.” It was therefore also absolutely consistent that the World Health Organization (WHO), the European Central Bank, the Bundesbank and the Robert Koch Institute have been stressing repeatedly in the corona crisis that there is no documented case that would suggest there would be an increased virus risk due to the use of cash as opposed to card payment. They refer here to corresponding scientific studies and underline repeatedly that no information on such a risk has been documented.

Freedom established by the constitution

John Stuart Mill, one of the most successful liberal thinkers of the 19th century, defined freedom as the “first and strongest desire of human nature.” Accordingly, all governmental and social action must be directed towards granting the individual free development, while his freedom, as Mill formulates it in a principle known as the “principle of freedom,” may be limited under one condition: to protect himself or another person. Now, during a serious crisis, all citizens are forgoing some of their fundamental constitutional rights of freedom. This massive intervention is certainly consistent with Mills’ theory in this time of corona. In his novel The House of the Dead, Fyodor Mikhailovich Dostoevsky describes his own experiences of life in a Siberian prison camp and writes the subsequently oft-quoted sentence: “Money is coined liberty,” whereby he describes the vital relevance of a free exchange of goods in an environment where people are deprived of freedom – with cash in the form of coins. Although not in the same way as Dostoevsky, we are also living in a time of extreme change: on a social, economic and political level. We are living in a time when, due to exponential technological developments, whole industries and business models are changing radically and countries are competing for supremacy in areas such as Artificial Intelligence (AI). It is a time in which transformation is the new norm and an agile corporate culture has to be the key to success. It is currently the case in many traditional industries that “anything that can be digitised, will be digitised.” And inevitably this also raises the question of whether this is also the case for the first “instant payment” solution, one of the earliest and longest-lasting achievements of human civilisation – for our cash? Our current free choice of payment method is certainly good, as long as we can choose freely as consumers the payment method appropriate for the respective situation. Discussions about the possible restriction of the freedom of choice of citizens regularly prompt intellectuals to issue warnings. For example, the poet Hans Magnus Enzensberger is of the opinion regarding the issue of “restriction”: “Those who abolish cash, abolish freedom.” This opinion is also shared by Carl-Ludwig Thiele, a former member of the Executive Board of the Deutsche Bundesbank: “Abolishing cash would hurt consumer sovereignty — the free choice of citizens about their payment instruments […] Government agencies do not have the right to tell citizens how they should pay.“

Technological vulnerability, fall-back option and data protection

Particularly in extreme scenarios such as disasters, failures of a digital infrastructure due to cyber attacks, natural events or simply due to technical failure, it is made clear that cash, by its nature, is currently the most robust payment method. The fact that the contactless payment limit has been increased without further ado, for example in supermarkets, at first sounds harmless. However, as a result, anyone can pay for higher-priced goods using a card, and it does not have to be their own card, without any further security checks such as entering a PIN. Everyone has to examine and question critically for themselves the possible consequences of such a payment method. Also not to be disregarded is the issue of data protection. More cashless payments also mean more personal information disclosed by everyone. Data which numerous companies use for commercial purposes. At the latest since the introduction of the EU General Data Protection Regulation (EU GDPR), the sensitivity of the population of Europe with regard to data protection and privacy has been rising gradually. Klaus Müller, Germany’s top consumer protector and Executive Director of the Federation of German Consumer Organisations (vzbv), describes cash as “data protection in practice”. Anyone who pays with cash does not leave any traces to create a consumer profile, purchasing and payment behaviour cannot be manipulated. Cash also helps to protect financial privacy. This was emphasised by Udo Di Fabio, who was a judge of the Federal Constitutional Court for twelve years, at the Cash Symposium 2018 hosted by Deutsche Bundesbank. He explained that every citizen can dispose freely of their money. In his view this freedom would be restricted if financial management were completely digitised.

Smart cash management alleviates the workload of banks

Crises such as the current corona pandemic always bring to light new approaches and act as accelerators of transformation processes that have already been set in motion. With regard to cash-related industries, the banking world has already been in a transformation process for some time. A company such as Prosegur, which, with over 4,000 employees and 31 branches, is a market leader in Germany in the transportation of cash and valuables, is increasingly becoming a full payment-platform provider. Several banks have already taken the path of fully outsourcing their cash management for synergy and cost-saving reasons. Here, cash processes are becoming not only much leaner, but also more cost-effective. This is the case not only for banks, but also for retail customers. With smart machines installed by Prosegur at its customers, cash can be disposed of directly and credited to the customer account on the same day. The smart infrastructure, including dynamic monitoring and forecasting, optimises the logistics and reduces costs in cash logistics. This is the next step towards an efficient, digital and integrated cash management.

Coined Liberty 2.0 and the justification for and rightfulness of cash

In view of the technological progress and the associated social changes, it can be seen that key values from the human perspective are still valid. Based on an intellectual, serious discussion, the relevance to today of the theories of for example Dostoevsky with his experiences in an unfree society is clear: The discussion about the civil rights and liberties of citizens is always very closely related to their ability to use cash freely, to their freedom of choice of payment method and ultimately to the rightfulness of their actions with regards also to effiency and impact. Our open and liberal society is characterised by the fact that we are discussing and most certainly will continue to discuss “Coined Liberty 2.0” at this level.

It has been a great pleasure giving the keynote at the CashCon2020 together with Mirko Siepmann, member of the board at Bankhaus August Lenz and long term business partner of Prosegur Germany.

We reflected with the expert auditorium, topics as Cash versus Crypto, The rise and fall of cash through the ages; Why we Germans, of all people, stick so closely to cash and if ATMs – will soon be a thing of the past or will they withstand digital disruption?

A crypto currency challenges technology, regulation and humans.

Author: Jochen Werne

“Money is perhaps the most concentrated and acute form and expression of trust in the social-state order.”

Georg Simmel

In this clarity, the German philosopher and sociologist Georg Simmel, born in 1858, formulated the value of a currency in his work “Philosophy of Money”. This clear and comprehensible insight also provides a simple basis for understanding why, for example, states rely on the independence of their central banks. And just as simply the question arises, which order do you trust when it comes to crypto currency?

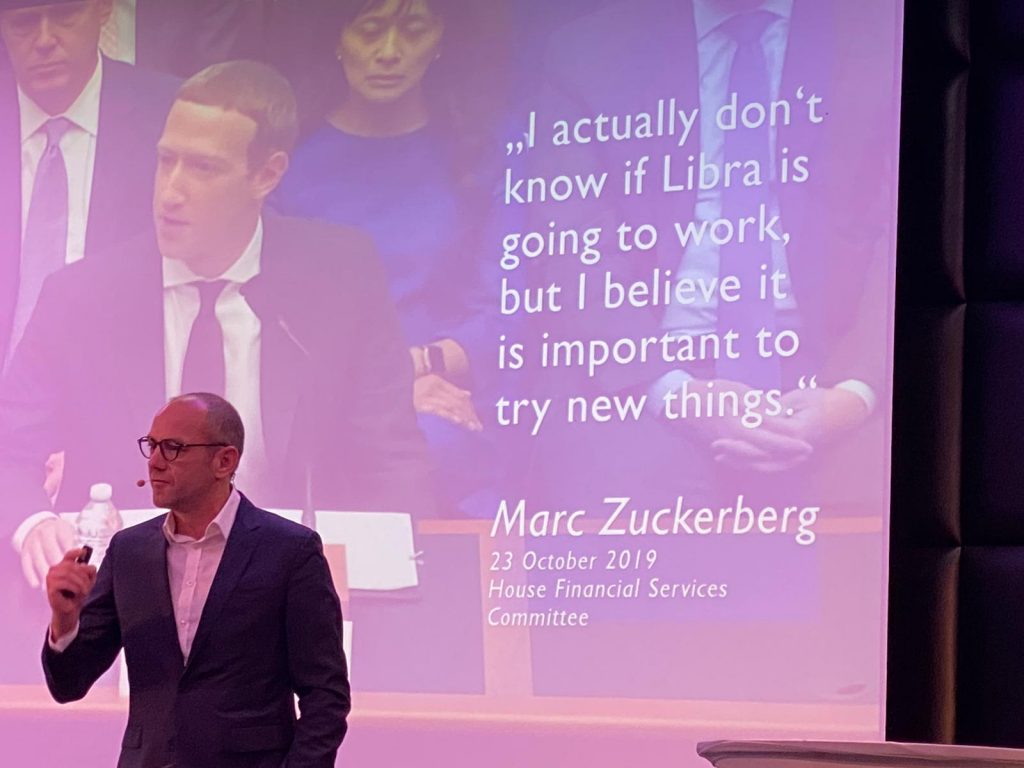

Almost 4,000 of these currencies now exist worldwide. After Bitcoin, Ether, XRP, Litecoin and Co., Libra now wants to establish itself as a future heavyweight in the market – and with a noble goal. Libra is to become the cashless payment option “for mankind” and make international payment easier.

Libra Coin – the currency of the future?

No crypto currency received comparable media attention, triggered only by the announcement of the project. And the emotionality and toughness with which the discussion is already being conducted shows how seriously the topic is being taken. It’s about reputation, influence, control, responsibility and only in the last instance about technology. Central banks and government bodies are sceptical about the “currency of the future” on a broad basis, even though the advancing globalization could argue for a single currency in the long run. A currency that supports a consistent free exchange of goods and services. Also under discussion is whether Libra Coin could be the means of payment for the approximately 1.7 billion people who have no access to banking services and whether the familiarity and the large target group of Facebook, combined with the announced low transaction costs, could make it possible to reach billions of people worldwide.

Challenges at all levels

Technically, not all hurdles have been cleared yet: In order to make a stable coin possible, it is necessary to find the right technology. It is precisely this stability that is supposed to distinguish Libra Coin from other crypto currencies and thus also make it suitable for skeptical end consumers. Members such as Mastercard, Paypal or Ebay should also provide the Libra Association with their names and brand promises additional confidence for the end consumer. But already today the alliance is not as stable as the founding members had hoped and the exits of Mastercard, Visa and Paypal weakens the consortium.

The Libra Association has repeatedly emphasized that it wants to comply with all regulatory aspects, but there are voices at the political and banking levels that are extremely sceptical about the project. The new payment system raises many questions in monetary and legal terms. Central banks and supervisors want to keep an eye on the influence of the potentially new currency and usually share the view that whoever acts like a bank must be treated like a bank. In other words, comprehensive requirements must be met and regulations observed – especially at the international level. This is difficult because current regulations are designed for the classical financial system, with which the Libra system has largely no points of contact. The aim is to keep total regulatory influence and not to allow any possible loopholes.

Despite its American origin, the Libra Coin is to be administered from Geneva by the Libra Association. The idea here is to be regulated by the Swiss Financial Market Supervisory Authority FINMA. Although Facebook has paid a lot of attention to the underlying technology, the legal issues still need to be clarified. Especially with regard to money laundering, consumer protection and possible misuse of the currency for illegal activities. Within the Association, there will be no special treatment for the founder Facebook, but equal voting rights for all members.

Acceptance and European values

With regard to Germany, it can be said that its citizens are within the international average as far as their affinity for digital is concerned. However, a historical-cutlurell caution can certainly be observed with regard to the topic of money, which certainly explains the well-known love of cash. A more pronounced European awareness of data protection with the General Data Protection Regulation (GDPR) makes many people, especially in Germany, sceptical about the subject. The fact that Libra was launched by Facebook is hardly a confidence booster after the Cambridge Analytica scandal. The fear of the transparent customer meets with security concerns about one’s own savings. Every German knows the quote: “Friendship ends with money” and thus new things are always put test. Culturally different in Sweden, where sometimes it’s only possible to pay by card. The same in China, where WeChat Pay and Alipay are no longer just a trend.

As always, changes are taking place step by step. It remains to be seen whether Libra Coin in its current form has future prospects. In any case, any change can only work if it is accepted and used by the end consumer despite all skepticism.

And this stands and falls – also in the digital world – with what Georg Simmel already put in the centre in terms of money in the 19th century: CONFIDENCE.

A more in-depth look at money and value can be found in the article “Coined Liberty 2.0“.

Following the keynote on “Libra in Retail?” at the Payment Summit 2019 in Hamburg, the article “Libra and the Dilemma of Trust” has been published to give participants further insides on the topic.