The participants of the seminar acquire knowledge that enables them as decision-makers to understand projects that are to use blockchain technology more quickly, to recognise opportunities and risks and to evaluate them together with experts.

It is a pleasure for me, as Managing Director of Prosegur Crypto GmbH, to support the seminar together with other leading blockchain experts such as Christoph Impekoven (micobo), Markus Honvehlmann (micobo), Dr. Marc Henniges (d-fine), Dr. Timo Bernau (GSK), Lucas Zaehringer (verity) and Cara Reuner (Ecota) to train banking experts to create future innovative use cases. We will discuss:

Digital Money

Central Bank Digital Money – Stable Coins

Programmable Money

E-Money Tokens

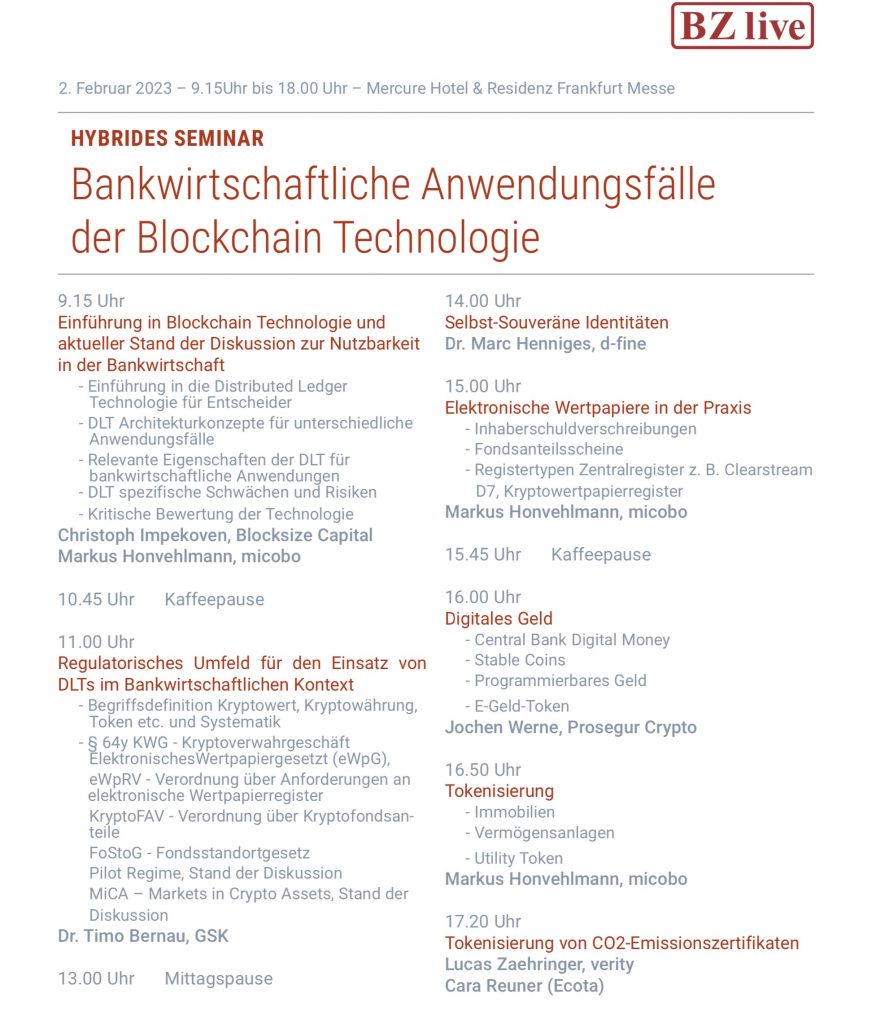

For more details please refer to the website of BZ-Live: https://www.bzlive.de/veranstaltung/1606//

It was a great pleasure to meet again personally and be connected virtually with friends like Dr. Andreas Heindl and Dr. Johannes Winter who, like many others inside and outside this Digital Summit, dedicate their passion to the digitisation of Germany day after day. Their passion is the engine for Germany’s competitiveness and prosperity. Exchanges like today between Germany’s leading experts in the field of digitalisation and the German government are crucial for the country’s future innovation.

This was underlined today by Federal Chancellor Olaf Scholz and the ministers Robert Habeck, Volker Wissing, Nancy Faeser and Bettina Stark-Watzinger. A special motivation was given by Estonian Prime Minister Kaja Kallas and Japan’s Digital Minister Tarō Konō.

Congratulations to the organization committee and thank you for the kind invitation. Details can be found HERE

Digital Summit 2022

Germany’s digitisation continues to remain one of the main topics of the German government. The aim is to accelerate and promote digitisation processes and to exploit their potential to develop prosperity, freedom, social participation, and sustainability.

In this context, the Digital Summit remains the central platform for shaping the digital transformation with all parties involved. It focuses on the key fields of action within the digital transformation across ten topic-based platforms. The platforms and their focus groups are made up of representatives from business, academia and society who, between summit meetings, work together to develop projects, events and initiatives designed to drive digitisation in business and society forward. The Summit will serve to present the results of the work that has been done in the past, to highlight new trends and discuss digital challenges and policy approaches.

This year’s Digital Summit of the Federal Government will be held on 8 and 9 December 2022. The Federal Ministry for Digital and Transport and the Federal Ministry for Economic Affairs and Climate Action will jointly coordinate the summit’s preparation in the future. In the new legislature, new formats, concrete results and international impulses are to make it the driving force and showcase for digitisation in Germany and beyond.

In the midst of these crazy times, most industries still haven’t gotten their shit together. However, a few bright minds managed to understand the paradigm shift, act accordingly and reap the rewards. So, Catharina van Delden and Bente Zehan talked to some of them! Join us on our learning journey over the next few weeks to see how completely unrelated industries deal very differently with the same challenges we all share – and let’s become better together!

Jochen Werne is Prosegur’s Chief Development and Chief Visionary Officer since 2019. Before that, he worked at different banks, most recently as a director of the German Bankhaus Lenz & Co. Since the beginning of 2022, he is also the managing director of Prosegur Crypto, which is applying for a crypto custody license in Germany.

The Madrid-based company Prosegur offers different security services worldwide. They’re most famous for their cash-in-transit services, with more than 50% market share in Germany. In recent years, Prosegur has explored ways to provide digital security services based on its long experience in a non-digital world.

How do you develop new business models and drive innovation within a company that makes its money with a very traditional business model like cash-in-transit?

I would like to jump right in with a personal example: Before I joined Prosegur in 2019, I had a career in banking. When you work in treasury, you have a lot of money you need to invest. As a bank, we were engaged in the investment business and in our case, most of the money had to be invested in the short term, unfortunately within a negative interest rate environment throughout the last years. So, the best solution would have been to put your money under the mattress instead of in a bank account. When I joined Prosegur, I explained this pain point and we discussed how we could solve this problem for treasurers. Since anything which has fewer costs than 0,5% is considered profit for a treasurer, we offered asset managers, high net worth individuals, and banks custody of short-term liquidity fully insured and compliant in our high-security facilities.

You’re in the security sector. From another conversation I recall you talking a lot about feeling safe vs. actually being safe – an image Catharina and I discussed before starting this series. Our example is a house standing by a cliff, with that a giant tsunami arriving. Instead of thinking about how to relocate, many industries seem to wonder about putting solar panels on the roof and perhaps repainting. Both are valid things to do – however, perhaps they’d have a different focus if they had zoomed out. Is that also a topic within your company, and how do you handle such problems?

This is how new business models and innovations can emerge: You have to take a different perspective, look at other people’s problems and find solutions based on your own experience and knowledge. That is an excellent picture. And if you take that into account, I think also from a psychological point of view, we live in our bubbles. Let’s take, for example, the phenomenon of social media: You “privately” click a like button, watch a video, or comment on a post without really knowing how much this very private behavioral data is influencing an algorithm (which in the best case just targets you as a potential buyer of a certain product). After all, you are only doing it “privately” – but you’re not! If you were to zoom out, you’re back at your tsunami example. It happens in everyday discussions, from climate change to energy crises. Sometimes, people take a point of view and go blindly in one direction. If you’re able to zoom out, you’re also able to change your behavior and find many more solutions to problems.

When making decisions and discussing innovations, it’s important to accept that you yourself are not able to see the whole picture. And based on that, you should go into discussions with an open mind – without thinking you’re completely right and cannot learn anything from the others. Innovation can only happen when people think outside the box, try to understand the whole picture, make new connections, and then act on their new insights.

Business leaders also need to ask themselves how they can innovate. Do they talk about the future, about what they need to create, and how it is no longer the same? Or are they just pushing to quickly return to their classic KPI models, missing the direction the rest of the world is moving in?

How do you take actions from the big picture and implement them? Basically, how do you zoom in again?

Prosegur works in an industry with low-profit margins. We can never sit back and say, “Yes, we have a wonderful company here, everything is going great!” It is labor-intensive work with – obviously – high labor costs.

So we can’t afford to be just visionary; we also need to focus on the essentials. We need justified results every month. Therefore, more than in other sectors, the rule is: if you deliver results, people will listen to you. It’s also part of my job to enthuse people and help them understand new concepts. But I wouldn’t say that’s purely related to my role; anyone in a leadership position should see it that way. Prosegur is a big matrix organization, so you have to use your network to move things forward.

In security, there are a lot of processes with rigid security protocols that won’t be changed in an agile approach quickly and easily. But with other and industry-adequate means the teams are improving efficiency every day.

How do you go about that?

People have to be trained. Otherwise, it won’t work. You have to get people to change. But don’t be surprised that the goal will never be achieved 100% because you will never get everyone to embrace change. Resistance to change within the individual is far too great and it’s very often just too convenient to stay in the comfort zone.

I would like to come back to your example of the house on a cliff. I have seen people who’ve ended up in a disaster professionally because they didn’t want to or were afraid to go into action. You have to be open-minded and sometimes even force yourself out of your personal comfort zone.

You founded Prosegur Crypto GmbH – a business model that to the untrained eye has little to do with your core business: cash. In convincing your board this is a relevant thing to do what are your learnings regarding the degree decision-makers need to understand new technology? Should everyone become a super tech expert?

I don’t ask the whole company’s management to be full experts on all technologies. That’s impossible. But please – as a responsible decision-maker – understand the leading technologies existing in this world! For example, as a banker, you should understand the concept behind blockchain. Of course, this is very technological, and most people can’t explain it in a good manner, but you must understand it. To better understand, decision-makers should have a “new-in-tech” training every couple of months, besides all the usual management training.

So, my appeal to every business leader is: Take your time and try to at least get the gist of things. You should understand what technology can and cannot do, and not just follow your daily headlines. The second part is to really listen to your existing experts whom you pay to know all the details. They need to be at the table and give their input to assess the next useful steps.

Lastly, we’ve talked a lot about networks. What are your best practices regarding this?

It is one of my favorite topics! First of all, you need to know that networks have not just existed since social media came into existence but have always existed. Network organizations have always brought – likewise interested – people together. Unfortunately, also on this topic, we do have to step out of our comfort zones to broaden our perspective. Otherwise, our networks take us as prisoners and we are as the known proverb says birds of the same feather who flock together.

There is very good literature on networks: like “The Square and the Tower” by Niall Ferguson or “The Starfish and the Spider” by Ori Brafman and Rod Beckstrom. Everyone should read these books.

————————————-

Tl;dr for the lazy

• People live in their bubbles and make themselves too comfortable within them, even if it sets them up to fail. It’s important that companies (and we as a society) zoom out to see the bigger picture. • Innovation and new business development can only happen if you combine your own experiences and opinions with other points of view. • Companies need to go beyond just recreating and reusing what has already worked for them. They should start asking questions and finding solutions that truly bring them on the right paths into the future. Even or especially if that means that they need to get out of their “safe space” (which is not so safe after all). • Instead of judging ideas and innovations as being “good or bad”, look at what they “can and cannot do” • You need to train and communicate openly with people to overcome the resistance towards change.

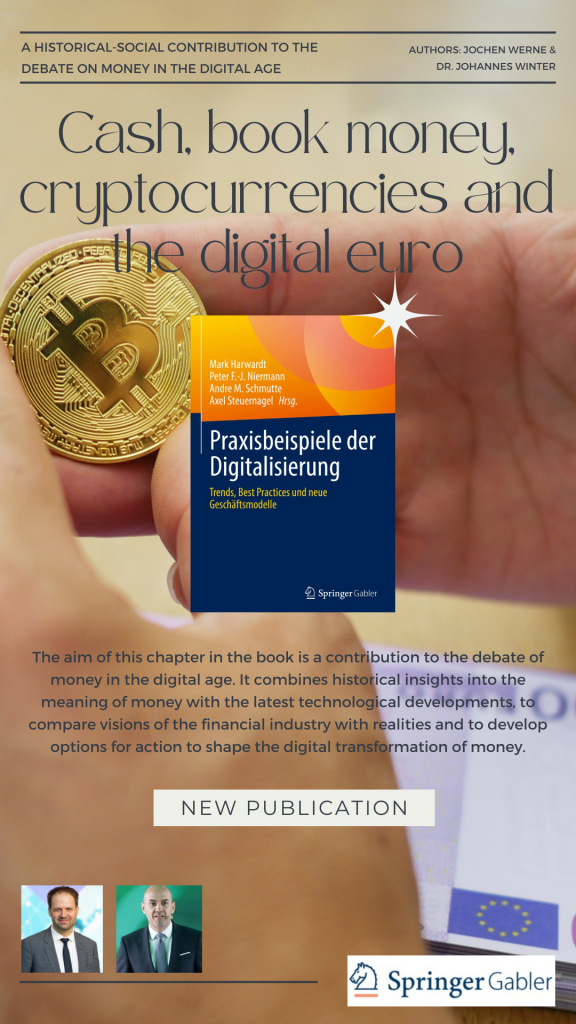

It was a pleasure contributing in co-authorship with the AI-expert and friend Dr. Johannes Winter / Jochen Werne to this new Springer Gabler publication ”Praxisbeispiele der Digitalisierung” (Best Practice of Digitilisation) which is available now as e-book and paperback at https://link.springer.com/book/10.1007/978-3-658-37903-2

Cash, Book Money, Crypto Currencies and the Digital Euro

The aim of the chapter in the book is a contribution to the debate of money in the digital age. It combines historical insights into the meaning of money with the latest technological developments, to compare visions of the financial industry with realities and to develop options for action to shape the digital transformation of money.

Abstract: In a world where tech companies are leading campaigns to create a new cryptocurrency and bitcoin is surpassing the US$50,000 mark because a visionary electric car maker wants to recognise the cryptocurrency as a means of payment, some fundamental questions arise: how must money be defined in a digital world to reliably fulfil the characteristics of a universally recognised store of value and medium of exchange? And what changes are in store for the financial industry when so-called stablecoins proliferate and challenge the banks’ classic deposit business and their outdated business models? The aim of this contribution to the debate is to combine historical insights into the meaning of money with the latest technological developments in the digital age, to compare visions of the financial industry with realities and to develop options for action for shaping the digital transformation of money.

Thomas Apitzsch, Michael Pfleger, Frederike HaberlandPages 309-325

About Springer Gabler

Springer Gabler Verlag is the leading specialist publisher for the business sector. Its classic and digital teaching materials and specialist media address current business questions and provide reliable, practical solutions.

Source: Die Welt – original language German | Translated by deepl.com

International security company Prosegur stores cryptocurrencies in super-secret locations without internet access. Partner O₂ Telefónica makes the communication possible and ensures that it is secure.

Looking at money, it quickly becomes clear that times have changed. In the ten biggest bank robberies, around 1.5 billion euros were taken, all told. In crypto hacks, it was around 3.9 billion euros in 2021 alone, according to the analysis company Crystal.

Jochen Werne is not surprised. “Anything of value arouses covetousness.” Werne is Chief Development Officer and Chief Visionary Officer Prosegur Germany. He develops new services for the German subsidiary of the international security group. Prosegur Crypto GmbH offers such a service, Werne is managing director: a custodian for digital assets – without an internet connection.

New money, new risks, new security concepts

Security world market leader Prosegur is famous for its yellow money carriers and became big in the cash business. With the boom of cryptocurrencies, new demands came to the company with headquarters in Madrid. The goal: to be able to offer the world’s most secure storage method for cryptocurrencies. In Germany, Prosegur works together with the business customer division of O2 Telefónica. Together, they are setting themselves up at a new level of security – the highest level, because billions in Bitcoin, Ethereum and other digital currencies are at stake.

“Our goal is to help give the new ecosystem the trust it deserves through security components,” says Werne. “Our history is closely intertwined with the security of any asset. Crypto custody is a logical evolution of our business.”

O2 networks vaults and money

O2 Telefónica is taking over the communication for Prosegur Germany, and completely. Karsten Pradel, Director B2B at O2 Telefónica, explains: “It starts with the mobile phone service for 3300 employees. In addition, around 1,000 of Prosegur’s yellow armoured cars and networked safes are equipped with a Global SIM from O2 Telefónica. In this way, the armoured vans and the security boxes are directly and securely connected to Prosegur’s company network. Via GPS, the routes of cash transporters can be documented and secured.”

O2 also provides fast fibre-optic access and secures internal communication against external access with VPN (Virtual Private Network) access. A completely new feature is a software-controlled data network (SD-WAN): this allows the Prosegur data traffic to be controlled intelligently and quickly.

In this way, the environment at the site can be secured against threats – where the internet traffic originates. An intelligent component links all communication paths and always selects the best one. This has three advantages, says Sören Jahnke, Global Solutions Engineer at O2 Telefónica: “A lot of bandwidth at a low price, more redundancy and thus communication security (because copper cable, fibre or mobile are used depending on availability and demand) and a better user experience because the services work better: ‘Everything runs much faster'”.

Where it gets critical is when people and the internet come into play

Prosegur aims to offer the ultimate crypto custody method. Yet transactions in cryptocurrencies are actually secure. Their cash book is the blockchain. That’s where the crypto money is stored. The blockchain is a digital document; digital copies of this document are stored simultaneously on a large number of computers – this makes it forgery-proof. When a transaction is made, the data chain contained in the document is supplemented in all copies by a data block that can never be deleted again.

However, it becomes critical when people and the internet come into play. Anyone who trades in cryptocurrencies needs a wallet. This is a kind of digital wallet. The wallet software in turn creates a digital signature and processes a transaction with the owner’s private key. Only in this way does the owner gain access to his crypto treasures stored in the blockchain and can use them. “You can always trace every step, what happened when and where,” says Jochen Werne.

Danger for assets and for people

This wallet can be made available in an app or on a computer and is usually connected to the internet. This is called a “hot wallet” – it is convenient because transactions can be made quickly, but it is vulnerable to hacker attacks. A “cold wallet” (also called “cold storage”) works without direct internet access – this can be a USB stick, for example. This form of asset storage has two problems. Firstly, a cold wallet can be the target of an extortionist or robber, just like a gold bar or large amounts of cash stored at home. Secondly, cold wallets are only secure as long as they are disconnected from the internet.

“For us, cold storage is not enough,” says Jochen Werne. “Because having large assets at the disposal of only one person not only endangers the assets, but also the person who has that power of disposal. Here, criminals not only resort to direct threats of violence on this person, but they often also threaten family members.” Prosegur Crypto therefore takes a different approach. The company stores customer data in a hardware security module (HSM). The technology works in much the same way as we would expect in an agent film.

No chance for “Ocean’s Eleven”

“This is a computer in a military-standard shielded case that is kept in one of our high-security facilities and is not connected to the internet,” Werne explains. If, contrary to all expectations, such a device should fall into the wrong hands, it deletes the stored data. Security protocols then stipulate that the data can be reconstructed via a highly complex system equipped with appropriate codes. Prosegur has a whole range of high-security facilities. The locations of the crypto-bunkers are, of course, secret.

“The entire security is fully electronically monitored with various modules and security protocols on several levels. These are smart fences, for example, where possible threats are analysed by artificial intelligence,” says Werne. Even an attack like in the film “Ocean’s Eleven” – George Clooney’s crew simply turns off the power there – would not work.

“WE BELIEVE WE CAN OFFER THE MOST SECURE CUSTODY METHOD FOR CRYPTO ASSETS IN THE WORLD”

JOCHEN WERNE Chief Development Officer and Chief Visionary Officer Prosegur Germany

And yet Prosegur customers can initiate blockchain transactions online – what follows is a sophisticated process. In the process, the hardware security module connects to a computer network that makes blockchain transactions possible.

The technology comes from GK8, a company specialising in crypto technology; the method used here is so-called multi-party computing (MPC). The transaction is transferred to the user’s blockchain via several security instances, using a patented technology that does not require a direct connection to the internet. This secures the critical moment of the transaction. “Everything else stays in cold storage” – most of the time the crypto assets are in the Prosegur high-security vault, without an internet connection. Jochen Werne: “We believe that we can offer the most secure custody method for crypto assets in the world. Currently, we are preparing to launch this service with the appropriate licensing in the strictly regulated German market as well.”

As Germany’s market leader for money and value services, it is of particular importance for Prosegur to maintain professional partnerships with the best companies on the market. We are pleased to be able to rely on our partner o2 Business (Telefónica Germany) in the telecommunications sector worldwide and it was a pleasure for us to serve as a reference for their new campaign.

Many thanks to Heike Windfelder, Fritz Fechner, Ilka Wiehe, Erhan Ocak Malte Jost Edda Heue Vanessa Eggestein Hasan Celebi Heiner Eberle Collja Lorig Michael Mogk Peter Strauss Ogilvy Telefonica INTOKU PICTURES for the support, the fantastic shooting day and the great result

Campaign #advertisement #Prosegur #Telefonica #O2

124.000 views in the first 18 hours just on YouTube … a good start

It was a inspiring holding in hand the first edition of the JOURNAL OF AI, ROBOTICS & WORKPLACE AUTOMATION published by Henry Stewart Publications

We are pleased to give everyone the opportunity to download the entire article POINT OF NO RETURN by Jochen Werne & Johannes Winter here: https://lnkd.in/dmi9i9aB

The inspiring articles and case studies published in Volume 1 Number 1 are:

Editorial Tom Davenport, Distinguished Professor, Babson College, Research Fellow, MIT Center for Digital Business and Senior Advisor, Deloitte Institute for Research and Practice in Analytics

Practice papers:

The path to AI in procurement by Phil Morgan, Senior Director, Electronic Arts (EA)

How to kickstart an AI venture without proprietary data: AI start-ups have a chicken and egg problem — here is how to solve it by Kartik Hosanagar, Professor, The Wharton School of University of Pennsylvania and Monisha Gulabani, Research Assistant, Wharton UK AI Studio

Towards a capability assessment model for the comprehension and adoption of AI in organisations by Tom Butler PhD MSc, Professor, Angelina Espinoza-Limón, Research Fellow and Selja Seppälä, Research Fellow, University College Cork, Ireland

The path to autonomous driving by Sudha Jamthe, Technology Futurist and Ananya Sen, Product Manager and Software Engineer

Point of no return: Turning data into value by Jochen Werne, Chief Visionary Officer, Prosegur Germany and Johannes Winter, Managing Director, Plattform Lernende Systeme – Germany’s AI Platform

Robotic process automation and the power of automation in the workplace by Raj Samra, Senior Manager, PwC

Difficult decisions in uncertain times: AI and automation in commercial lending by Sean Hunter, Chief Information Officer and Onur Güzey, Head of Artificial Intelligence, OakNorth

The intelligent, experiential and competitive workplace: Part 1 by Peter Miscovich, Managing Director, Strategy + Innovation, JLL Technologies

Responding to ethics being a data protection building block for AI by Henry Chang, Adjunct Associate Professor, The University of Hong Kong

Legal issues arising from the use of artificial intelligence in government tax administration and decision making by Liz Bishop Barrister, Ground Floor Wentworth Chambers

SECURITY BRIEFING. The battlefields of the past as a lesson for the protection of crypto assets today.

COLD HISTORY. HOT REALITY is a contribution to The Yearbook 2022 “Treasury and Private Banking”, edited by Roland Eller. The book is a well-known platform for building the bridge from the traditional to the new decentralised financial world.

COLD HISTORY. HOT REALITY by Jochen Werne is a plea for openness to new technologies, embedded in a historical-social security briefing on money, power and the indispensable need to protect assets. The battlefields of the past provide the framework for lessons on protecting crypto assets in our technology-dominated world and help us gain a basic understanding of the opportunities and threats in our new cyber reality.

COLD HISTORY – HOT REALITY was particularly inspired by conversations and articles from the following thought leaders, to whom I am deeply indebted.

Raimundo Castilla – CEO Prosegur Custodia Digitales, Ghislain D’Hoop – Ambassador of Belgium to Austria, Slovakia, Slovenia and Bosnia and Herzegovina, Permanent Representative to the United Nations, Roland Eller – Founder and CEO of Roland Eller Consulting, Niall Ferguson – Milbank Family Senior Fellow at the Hoover Institution at Stanford University, Christoph Impekoven – Co-Founder micobo GmbH, Benon Janos – CFO flatexDEGIRO Bank AG, Lior Lamesh – Founder & CEO of GK8, Bernd Lehmann – Historian, Commander of the German Navy (ret.), Rakesh Sharma – Author, Thomas Vartanian – Author and Counselor, Heath White – CEO Prosegur Germany, Johannes Winter – Managing Director of the Platform „Learning Systems“ – Germany‘s AI-platform

Preview and excerpt from Chapter I of “COLD HISTORY – HOT REALITY”

WHAT IS PAST IS PROLOGUE

Impressive and powerful, the words “What is past is prologue” are chiselled in white marble at the foot of the statue in front of the National Archives in Washington D.C.. The famous quote from William Shakespeare’s “The Tempest” is a haunting reminder to everyone that history provides the context for the present.

We live in a present that is changing at breathtaking speed. This fact concerns us daily, but if we do not take the time for a little history lesson, we are doomed to painfully repeat the mistakes of the past. More than aware of this realisation is the former CEO of tech giant Alphabet, Google’s parent company. He dedicated the following note to the New York Times bestseller, “The Square and the Tower: Networks and Power, from the Freemasons to Facebook”: “Niall Ferguson … brilliantly illuminates the great power struggle between networks and hierarchies that rages around the world today. As a software engineer familiar with the theory and practice of networks, I was deeply impressed by the insights of this book. Silicon Valley needed a history lesson and Ferguson delivered.” Not only is Eric Schmidt impressed, but many of the thoughts in this article are inspired by Niall Ferguson’s illuminating papers and lectures.

The beauty of the past is that everything that has already happened, successes and failures, can always be explained in detail and serve as lessons for future challenges. Successful leaders use this knowledge to develop solutions to the problems of the future and to develop communication strategies to make their visions understood by others.

This article was written at a time when humanity is in the final stages of a global pandemic that is saddling countries with an unprecedented debt burden. At the same time, a “New Cold War” is emerging and an arms race for technological supremacy has begun. With new possibilities, the old equilibrium is shaken and a new, albeit familiar, competition for power and money begins. All this at a time when crypto-blockchain-based monetary systems are rapidly becoming a new reality.

The article, with its historical analogies, aims to give the reader a better understanding of how money, power and security are closely intertwined. This helps to put quite complex issues into perspective and gives a clear view of the dangers and opportunities of our changing reality.

The world and change are not to be feared, but understood.

Jochen Werne

The new YEARBOOK will be available in Spring 2022. Find out more HERE

Chief Development & Chief Visionary Officer Jochen Werne on the subject of sustainability

This year, the Bavarian State Medal was awarded to Jochen Werne by State Minister Thorsten Glauber for his personal commitment and services to the environment.

Prosegur congratulated him on this honourable recognition and asked him how this passion flows into his daily work at Prosegur.

SAVE THE DATE: 29 September 2021 – 11.30 a.m. Berlin Time

It‘s a great pleasure giving a keynote at the VÖB-Service GmbH #VSK2021 Conference and to discuss with financial industry experts fundamental questions about the FUTURE OF MONEY

The ten most successful bank robberies in human history, in which the equivalent of US$1.62 billion was captured at great expense, seem almost like the work of amateurs compared to the US$3.78 billion captured by cybercriminals in 2020 alone. In a world where tech companies are spearheading campaigns to create a new #cryptocurrency, where bitcoin is surpassing the US$50,000 mark because a visionary electric car maker wants to recognise cryptocurrency as a means of payment, Jochen Werne, Member of the Executive Board Prosegur Germany, asks some fundamental questions. “How must money be defined in a digital world in order to fulfil the characteristics of a generally recognised and reliable store of value and medium of exchange?” Or also: “What changes are coming to the financial industry when #Stablecoins spread and challenge the classic deposit business of banks?”

In our stream Digitalisation at #VSK2021, Jochen Werne presents possible answers to these and other questions.

Be there and register today for the #Kreditwirtschaft congress on Wednesday, 29 September! ? https://lnkd.in/gMe2g59