It has been a great pleasure not only to give a speech at the plenary meeting for the Wirtschaftsjunioren Hamburg, but also to discuss in-depth the impact of AI on our society with a highly engaged auditorium.

Together with the Wirtschaftsjunioren / (c) WJ Hamburg

After the meeting the Wirtschaftsjunioren summarised the evening on Facebook as follows:

“At yesterday’s plenary meeting of the Education Committee, we combined the exciting topic of artificial intelligence with the beautiful (junior) life. Our keynote speaker Jochen Werne, Director Business Development & Marketing at Bankhaus Lenz, lecturer and author, gave a vivid presentation on the opportunities, dangers and challenges of AI for companies and society. How does it feel to pass on your activated smartphone to the person sitting next to you? What does a folded leaf have to do with the moon and AI?

Jochen Werne / (c) WJ Hamburg

We had SALT AND PEPPER as a guest for the further practical testing of AI. In a VR environment, we were able to build future production facilities using the BoxPlan product. The innovative Startup Smunch, the online canteen for happy teams, provided us with very real, delicious food. In the lounge-like atmosphere of the Ruby Hans Workspaces we found a great setting for stimulating conversations and networking.

Smunch / (c) WJ Hamburg

Ruby Hans Workspaces / (c) WJ Hamburg

Smunch Dinner / (c) WJ Hamburg

We would like to thank all guests and cooperation partners for a successful junior evening: Private Family Banker, Exclusive Agent Bankhaus August Lenz & Co. PUBLIC LIMITED COMPANY, SALT AND PEPPER technology and management consulting, software development, Smunch.co And remember, on 26.05.2019 is the European election, Step Up For Europe (see group photo 😉 )”

Wirtschaftsjunioren Hamburg – Engagement for Europe / (c) WJ HamburgProf. Dr. Peter Scholz (HSBA) & Sven O. Müller (7orcas) / (c) WJ Hamburg

Thank you very much to the Wirtschaftsjunioren Hamburg and Alexander Köhne for the highly appreciated invitation.

Original published in German in the Handelsblatt KI-Summit “KI-Business Guide”. Translation performed by DeepL.com

“Google, how are my stocks doing and what to do?” AI in the financial sector – the next big thing? by Jochen Werne, Bankhaus August Lenz

AI is making its way into every industry, but banks, insurance companies and FinTechs in particular are seeing a renaissance for their data-based business models in disruptive times. Jochen Werne, director and head of the innovation team at Munich-based private bank Bankhaus August Lenz, explains the role that the human factor will play in banking and consulting in the future.

Google, Apple, Facebook and Amazon (GAFA) have long seen artificial intelligence as the technology of the future. Banks and insurance companies also see the potential in machine and deep learning approaches to be a relevant player in the future in an increasingly technology-driven market environment. After “FinTech”, “Blockchain” and “Crypto-currencies”, “AI” is the new buzzword of the industry. From the AI-optimized chatbot to highly complex, self-learning, investment algorithms – the omnipresence of the term suggests that the integration of Artificial Intelligence into one’s own business model seems to be virtually necessary for survival. But is that really the case, where do we stand and which factors cannot be replaced by technology?

What becomes possible in times of exponential technologies is de facto nothing less than a revolution. The financial industry holds a vast amount of valuable and already processed data. Not only do they reflect our daily and extremely private life, from buying tickets for the subway via apps to the preference of our garments – but they reflect also the payment flows of entire companies and industries, and therefor our entire economy. Maturing AI systems not only make it easier to prepare and process this data, they also make it much cheaper, faster and more targeted. AI will not only enable banks to make their services more customer centric, it will also transform most areas of the financial industry – from asset management to business operations and money laundering prevention to marketing.

Data protection has top priority

Every major technological leap has historically been accompanied by a positive and an abusively usable development. TIME magazine recently published an article by Apple CEO Tim Cook entitled “It’s time for action on privacy. We all deserve control over our digital life”. Every electronic transaction generates customer-specific data. These structured data sets, which have been collected for many years, are now becoming the most valuable raw material. It’s important to create meaningful use-cases especially when it comes to the enrichment of existing structured data sets with external, possibly unstructured data. However, this is exactly where the risk lies. If sensitive data falls into the wrong hands and is deliberately misused, cyber attacks can cause considerable damage to individuals and groups. Trust is and remains therefore one of the most important assets of a credit institution or financial service provider. Consequently, the protection of customer data in a digital banking world has absolute priority today more than ever before. When using AI technology, it is therefore essential to use private and sensitive data in the interests of the customer. And this is where not only IT and cyber security departments of banks come into play, but also politics: their primary task must be to find meaningful solutions for handling the effects of the use of AI on society, the economy and thus on our lifes and the work of tomorrow. And this without endangering the competitiveness of our own country. The fact that this topic is taken seriously is evident not only in national initiatives such as the German Platform for Artificial Intelligence “Lernende Systeme”, but also, for example, in the European Artificial Intelligence shoulder-to-shoulder approach, which is being pushed forward at full speed by France and Germany.

The ideal model for private customer business: Connection of AI and human-based advise

In order to advance the acceptance of AI in the financial sector, it is important that existing digital tools are even better adapted to customer needs. The successful symbiosis between people and digital technology is indispensable. With the help of online financial forums, banking apps, vlogs and digital industry comparisons, private individuals can now achieve basically the same level of knowledge as financial professionals, but what is usually lacking is the successful filtering of the “information overload” and the consideration of the behavioral finance problem.

A realistic model for the successful transformation of the financial sector is therefore quite simple: streamline business models and processes, use data efficiently and always place the needs of customers at the centre of all activities. Taking advantage from technological progress always comes with successful deployment scenarios. Consequently, the technological revolution associated with the use of AI systems can only succeed if it is accepted by society – meaning, by us humans.

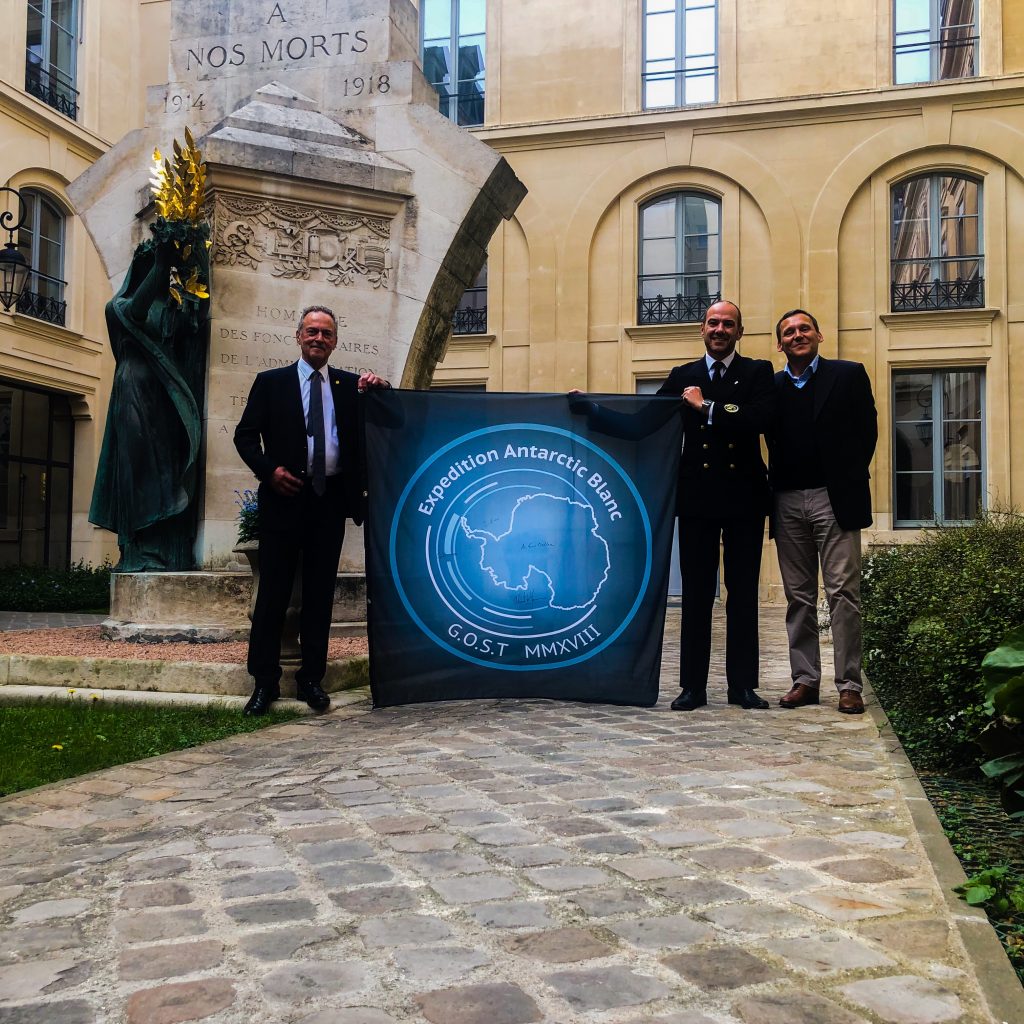

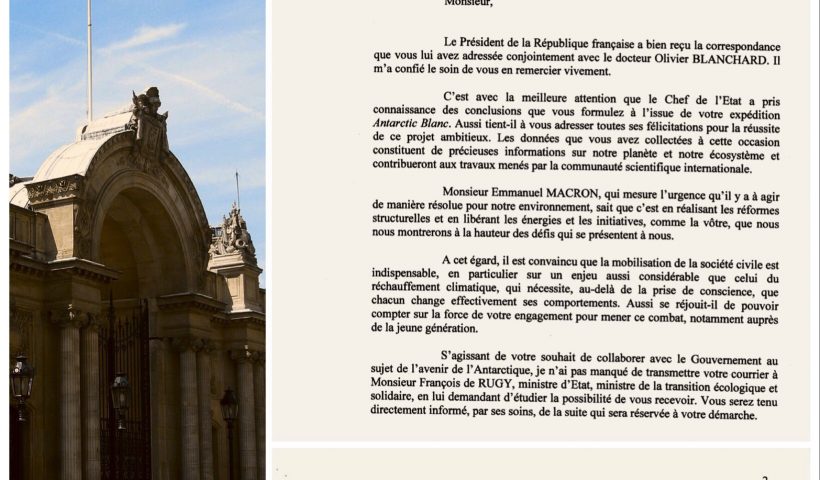

It has been an honour for the delegation of GOST’s Expedition Antarctic Blanc consisting of Jochen Werne (Expedition Leader), Dr. Olivier Blanchard (Chief Liaison Officer to France) and Dr. Wolfgang Händel (Chief Logistics Officer) to be received by Mme Sophie-Dorothée Duron, Conseillère Biodiversité Eau Mer and Mme Carole Semichon, Chargée de mission – Milieu marin, Environnement polaire. The international Antarctic expedition has been successfully carried out with French assistance. The delegation presented the expedition flag, which represented France in Antarctica, as a symbol of remembrance. Mme Duron expressed her gratitude and said that she will present the flag to François de Rugy, ministre d’État, ministre de la Transition écologique et solidaire. In addition to that ideas have been exchanged how to strengthen the ties and to further involve the civil society into ecological topics also via expeditions of the Global Offshore Sailing Team.

We are grateful for this fruitful get-together and we’re looking forward to our next meetings in Paris.

Es war ein großes Vergnügen gemeinsam mit dem GOST Chief Historian Bernd Lehmann in einem 45-minütigen Interview geführt von Christopher Griebel im Deutschen Museum über viele Facetten der Seefahrt und der zu dem Zeitpunkt bevorstehenden Antarktisexpedition Antarctic Blanc zu diskutieren.

Es ist etwas besonderes auf diese Pre-Expedition Dokumentation genau heute am 1. April 2019 zurückzuschauen, an dem Tag, wo eine Delegation bestehend aus Jochen Werne (Expedition Leader), Dr. Olivier Blanchard (Chief Liaison Officer to France) und Dr. Wolfgang Händel (Chief Logistics Officer), französischen Regierungsvertretern in Paris die Expeditionsflagge übergeben werden.

It’s greatly inspiring and an honour being part of this unique platform which is concentrating knowledge and illustrating perspectives in the field of artificial intelligence and self learning systems

The Plattform Lernende Systeme brings together expertise from science, industry and society for fostering Germany‘s position as an international technology leader. It understands itself as a forum for exchange and cooperation.

Designing self-learning systems for the benefit of society is the goal pursued by the Plattform Lernende Systeme which was launched by the Federal Ministry of Education and Research (BMBF) in 2017 at the suggestion of acatech. The members of the platform are organized into Working Groups and a Steering Committee which consolidate the current state of knowledge about self-learning systems and Artificial Intelligence. They point out developments in industry and society, analyse the skills which will be needed in the future and use real application scenarios to demonstrate the benefit of self-learning systems. A Managing Office at acatech coordinates the work of the platform.

Concept and aims of the platform

Self-learning systems are increasingly becoming a driving force behind digitalisation in business and society. They are based on Artificial Intelligence technologies and methods that are currently developing at a rapid pace in terms of performance. Self-learning systems are machines, robots and software systems that learn from data and use it to autonomously complete tasks that have been described in an abstract fashion – all without specific programming for each step.

Self-learning systems are becoming increasingly commonplace supporting people in their work and everyday lives. For example, they can be used to develop autonomous traffic systems, improve medical diagnostics and assist emergency services in disaster zones. They can help improve quality of life in many different respects, but are also fundamentally changing how humans and machines interact.

Self-learning systems have immense economic potential. As digitalisation takes hold, they are already helping companies in certain sectors to create entirely new business models based on data usage and are radically changing conventional value creation chains. This is opening up opportunities for new businesses, but can also represent a threat to established market leaders should they fail to react quickly enough.

Developing and introducing self-learning systems calls for special core skills, which need to be carefully nurtured to secure Germany’s pioneering role in this field. Using self-learning systems also raises numerous social, legal, ethical and security questions – with regard to data protection and liability, but also responsibility and transparency. To tackle these issues, we need to engage in broad-based dialogues as early as possible.

Plattform Lernende Systeme brings together leading experts in self-learning systems and Artificial Intelligence from science, industry, politics and civic organisations. In specialised focus groups, they discuss the opportunities, challenges and parameters for developing self-learning systems and using them responsibly. They derive scenarios, recommendations, design options and road maps from the results.

AI thought leaders met on the 21st and 22nd at the #HBAISummit not only to discuss the latest developments in machine and deep learning programming but especially real use-cases, trends in the start-up scene, the role of Germany and Europe in the AI race and the impact of AI on our society. Read more here

It has been a great pleasure discussing and being inspired by a highly engaged auditorium during two sessions:

C’est un grand honneur d’avoir reçu une invitation du ministère français de la Transition écologique et solidaire à remettre le drapeau de l’expédition internationale à Mme Sophie-Dorothée Duron, Conseillère Biodiversité Eau Mer au Cabinet du Ministre sur la recommandation du Président de la République française Emmanuel Macron.

Le 1er avril 2019 à 16h00, Mme Sophie-Dorothée Duron, Conseillère Biodiversité Eau Mer, accueillera une délégation de l’expédition internationale Antarctic Blanc, menée avec succès et avec le soutien de la France. La délégation présentera le drapeau de l’expédition, qui représentait, entre autre, la France en Antarctique, comme un symbole du souvenir.

Le Président français Emmanuel MACRON a personnellement souligné dans sa lettre de soutien à l’Expédition l’importance de la préservation de l’écosystème de notre planète et la valeur d’une sensibilisation de la société par cette initiative.

TEMPÊTES ET ICEBERGS

Expédition Antarctique Blanc poursuivait des objectifs historiques, sociaux et environnementaux. Les 12 participants de l’initiative à l’expédition, soutenue également par les Nations Unies et 19 États, ont traversé sur un voilier de 20 mètres, deux fois en 12 jours, dans les conditions les plus difficiles, l’une des routes maritimes les plus dangereuses du monde – le détroit de Drake, couvrant 1129 milles marins (plus de 2 000 km). Le voyage a été marqué par le passage de plusieurs systèmes orageux en Antarctique et au large du Cap Horn, ce qui a retardé de plusieurs jours le retour de l’expédition. Des vents soufflant jusqu’à 50 km/h, des vagues jusqu’à 8m de haut et des températures autour du point de congélation ont exigé des performances physiques de haut niveau de la part des participants à l’expédition.

CÉRÉMONIE COMMÉMORATIVE INTERNATIONALE.

Naviguer sur des routes historiques. L’expédition a commémoré les chercheurs, explorateurs et marins dont les navires ont dû surmonter les difficultés survenues pour atteindre une région inconnue du monde. L’équipe internationale a organisé une cérémonie commémorative sur l’île volcanique proche de l’Antarctique, d’importance historique, l’île de la Déception. Au nom de tous les États ayant soutenu l’expédition et des Nations Unies, une couronne de glace locale a été symboliquement formée et déposée afin de rendre hommage aux réalisations internationales dans l’exploration de ce continent unique. Les pays ayant soutenu l’expédition comptent parmi les signataires du Traité sur l’Antarctique du 23 juin 1961, un traité politiquement unique en son genre. Les chefs d’Etat et de gouvernement des 19 nations ont exprimé leur soutien à cette expédition unique et privée par des lettres adressées au chef de l’expédition, Jochen Werne, notamment pour la réalisation de cette cérémonie de commémoration.

LA FRANCE ET LE TRAITÉ ANTARCTIQUE.

La France a adhéré au Traité sur l’Antarctique le 23 juin 1961 et, par sa signature, a également reconnu que “dans l’intérêt de l’humanité tout entière, l’Antarctique est utilisé exclusivement à des fins pacifiques et ne doit pas devenir le théâtre ou l’objet de discorde internationale” “qu’il est dans l’intérêt de l’humanité toute entière que l’Antarctique soit à jamais réservée aux seules activités pacifiques et ne devienne ni le théâtre ni l’enjeu de différends internationaux”. La France a également souligné son engagement en faveur de la préservation de cet écosystème en tant que “réserve naturelle dédiée à la paix et à la science”.

INITIATIVE DU PNUE POUR DES MERS PROPRES.

L’objectif principal de l’expédition était de sensibiliser le public international à la préservation de l’écosystème unique de l’Antarctique et de soutenir l’initiative des Nations Unies Clean Seas pour combattre les déchets plastiques dans les océans. Avec l’Expédition Antarctique Blanc, cet important projet du Programme des Nations Unies pour l’environnement est maintenant accepté sur tous les continents de notre planète.

LES CONSÉQUENCES DU CHANGEMENT CLIMATIQUE SUR L’ÉCOSYSTÈME.

De plus, l’expédition a soutenu le projet de recherche de l’Université du Connecticut et de l’Université Northeastern sur le métabolisme du plancton en en prélevant des échantillons, ce qui pourrait apporter une contribution fondamentale à l’obtention de réponses rapides sur les réactions de l’écosystème face au changement climatique.

DES BALEINES DANS L’ANTARCTIQUE.

Avec l’observation de 18 baleines différentes et la documentation détaillée sur leur position et leur comportement, l’expédition a également contribué à l’établissement de la plateforme mondiale d’observation des baleines “Happy Wales”. Cette plateforme vise à fournir à la science des connaissances approfondies sur le comportement et le développement des plus grands mammifères de notre planète.

LE DÉVELOPPEMENT DES ENFANTS ET DES JEUNES.

Afin de promouvoir des projets internationaux pour les enfants et les jeunes, plusieurs retransmissions en direct en mer et sur le continent Antarctique avec les enfants de l’école de voile du Yacht Club de Monaco ont eu lieu. A son retour, l’équipe a visité l’école de voile Cedena Yacht School Puerto Williams, au Chili, qui est ouverte aux enfants de tous les milieux de la région la plus méridionale de notre planète, et qui les encourage par le sport à développer leurs propres objectifs et traits de caractère, propices à leur développement personnel. En plus d’un don de l’équipe de l’expédition, elle a posé la première pierre d’un échange international et les enfants ont suivi une présentation sur l’Antarctique et son importance.

LA RECONNAISSANCE INTERNATIONALE.

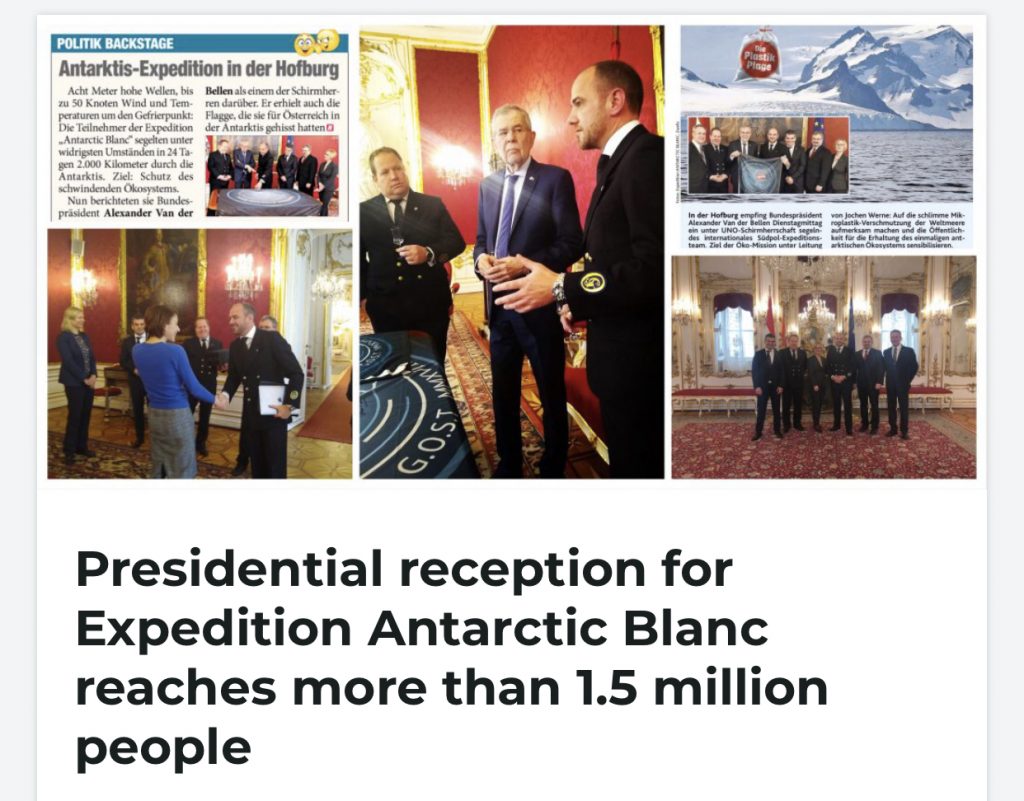

La visite à Paris marque la cinquième réception importante pour Expédition Antarctique Blanc après celle du Prince Albert II à Monaco, de l’ambassadrice des pôles des Pays-Bas, Carola van Reijnsoever, à La Haye, du Président de l’Autriche Alexander Van der Bellen à Vienne et du secrétaire particulier de Sa Majesté la Reine du Danemark Henning Fode.

INVITATION À LA PRESSE

Après la remise du drapeau le 1er avril 2019 à 16h00 à Paris, le chef d’expédition Jochen Werne et le chef de liaison en France Olivier Blanchard seront à la disposition de la presse pour répondre à des questions et interviews, ou se prêter à des photos et des tournages.

Sur demande, la délégation peut également participer à des conférences de presse à Paris ce jour-là.

Oliver Picht Navigateur et chef de la documentation

Linden Blue Chef des communications

Bernd Görgner Chief Medical Officer

Benon Janos Coordinateur des initiatives environnementales

Wolfgang Händel Directeur de la logistique

Hans Axtner Maître de cérémonie

Michael Melnick Coordinateur en chef des sciences

David Gamba Observateur en chef

Wolf Kloss Skipper et propriétaire d’un bateau d’expédition

Karl Papenfuss Maté

Commentaire sur l’initiateur de l’expédition – The Global Offshore Sailing Team (GOST)

L’expédition “Antarctic Blanc” est la suite de l’initiative polaire lancée en 2016 avec des objectifs comparables sous le nom de “Arctic Ocean Raptor”, mais dans la zone maritime du Spitzberg et jusqu’à la limite de la banquise arctique. Un autre aspect important a été la commémoration des marins de toutes les nations, qui ont rempli leurs fonctions de marins au cours des opérations maritimes dans l’Arctique dans des conditions météorologiques généralement impitoyables et qui ont en partie perdu la vie. Au nom du roi norvégien Harald V et du gouvernement canadien, une couronne a été remise au lac ; la Belgique, l’Allemagne, la Grande-Bretagne et l’Italie ont également apporté leur soutien international à cette expédition. Fondée en 1999 par Jochen Werne et Guido Zoeller, l’équipe Global Offshore Sailing Team s’est à nouveau engagée dans l’histoire maritime et les questions environnementales avec cette expédition particulièrement exigeante et sa campagne People’s Diplomacy.

There is no lack of buzzwording when it comes to trends in the financial sector: Disruption, FinTech, block chain, crypto. Currently, another term is climbing the zenith of a media hype – platform banking. And not without good reason. “Platform Banking” was voted “Financial Word of the Year” in 2018. Behind this lies the call for banking institutions to open up to third-party providers. Banks and savings banks should not only offer their own services on open platforms, but should also integrate third-party offers and services. Consistently thought through to the end, banks will thus become more intermediaries for all possible services and less providers of their own financial services. The legally necessary prerequisites for such an approach in the strictly regulated financial market have already been set in motion by the adoption of the Payment Services Directive PSD2. Will platform banking become a new hope for the industry, or another risk component in the attempt to lose fewer customers to new technology competitors?

The hype surrounding the topic is understandable: Eight of the ten world’s most valuable companies – Amazon, Google, Microsoft, Apple and Co. – have a platform in their business model. And even more striking: Only one of these companies was already among the top 10 worldwide in 2008. This growth potential, which is the result of the platform expansion, is of course intended by many industries to benefit themselves. The world of finance is also changing rapidly. In recent years, a variety of innovative developments have taken place in the areas of payment transactions and payments. The arrival of third party providers and fintechs has changed the market sustainably and comprehensively. According to a recent whitepaper by Deloitte Consulting, banks will also have to consider a platform strategy in the future: In the future, the customer base will also be able to access products and services from third-party providers in addition to the existing offering. The long-term goal behind this is well known – to retain existing customers, acquire new ones and increase margins.

Platform as recipe for success?

In general, a platform can be seen as a place where supply and demand meet. Economists call such a market – not a new discovery. Due to the digitization of all areas of business and life, geographical boundaries of the marketplaces belong to the past. The result: an almost unlimited number of supply and demand meet on a digital platform – and competition is known to stimulate business. In these business models, the so-called “network effect” ensures that with each new provider on a platform, the incentive for demanders and customers also increases. And in general the more demanders there are on the platform, the more lucrative it becomes for the suppliers. Both sides save enormous search and time efforts and transaction costs are reduced. In short, reflects this the recipe for success behind industry giants such as Amazon, AirBnB, Uber and Co. Nevertheless, there are existing fundamental reservations. The desire of many bank managers to grab a straw in order to grasp a component of hope in a difficult market environment seems understandable. However, blind action is fatal in this situation. Banks must not forget what the emergence of competition in the form of FinTechs has already revealed: frightening weaknesses with regard to their own modern hardware and software solutions, organisation and innovative corporate culture. The fact is that the challenge facing change management is proving to be enormous. And this already now, without having given space to the idea of creating a single platform. The current wave of closing down banking or partnership-based Robo Advisor solutions shows how quickly these carriers of hope can become problems. The commission model behind this, which is always transparent and low priced, is hardly profitable for the banking infrastructure and marginalises the added value that an institution is able to provide for its customers.

The complexity of the changes on all levels, starting with the completely changed, technological possibilities and their effects on the transformation of long-established business models, over the resulting new economic situation of the enterprises are enormous. The difference to the past decades lies in the temporal component. If companies today do not react directly to market changes, they open the way for competitors to their own customers. And this faster than ever before. In such disruptive times, all those involved want an “efficient” change process. However, active, well-considered and vital change management is often criminally neglected. For this one opens door and gate to blind actionism.

The business model of a financial platform is complex, the regulatory framework is strict and the willingness of customers to switch is only slightly visible. For this reason, this business model has so far been too uninteresting for Internet groups. And now, of all things, the banks, often perceived as conservative and unmodern, are to be transformed into digital platforms that can compete with Amazon & Co?

Enormous change management challenge

Banks need a forward-looking and sustainable strategy. That is beyond question. At the latest since the massive “democratization” of the Internet at the end of the 1990s, our lives have been shaped by leaps in technology. In short, the world feels like it is turning faster than ever before. What does this mean for the banks of the 21st century? Anyone who does not understand this exponential dynamic of technical possibilities or does not take them sufficiently into account in his business model can quickly lose touch – with the customers of today and tomorrow. Open banking is both an opportunity and a technological challenge for the banking industry. The European Payment Service Directive 2 – or PSD2 for short – has inevitably made opening up to third parties the focus of the digital strategy.

At the technical level, this is primarily associated with the use of programming interfaces, so-called APIs, which enable both internal and external cost-effective and fast access to data, as well as functions of software applications. What provides the end customer with a cross-product customer experience, means for banks to strategically cooperate with external partners. For FinTechs, cooperation is also advantageous. It creates fast access to customers and their data, as well as to the necessary financial and structural prerequisites.

Anticipating these developments requires a good eye for tomorrow’s customers. After all, customer data is a success driver for future business models. A few years ago, FinTechs began to “poach” their digital offerings among the customer base of traditional institutes. All of this culminated in Robo-Advisors, standardized, computer-controlled asset managers with low fees. It was therefore time for the banks to set sail anew. The plan was to enter into symbioses with FinTechs or “buy” their products directly into their own portfolios. For many large banks, it has become good form to enter into cooperation with small, independent and innovative financial service providers. This is also clearly demonstrated by the current situation of FinTechs. Mergers and co-operation are nothing else than a proof for the fact that the search for sustainable business models is not easy with a fixed idea to solve, not even with the platform strategy. Nevertheless, neither the previous business models nor the product possibilities seem to be mature.

Don’t forget the human factor

The personal relationship, the touchpoint between customer and consultant in the real world, has been increasingly reduced by the acceptance of digital banking. Nevertheless, even if a digital experience is a good thing for a modern bank, consumers continue to appreciate human contact points – especially in economically or politically turbulent times.

The challenge lies in providing the right balance between the digital experience and the traditional, trust based, personal customer relationship.

Jochen Werne

This is precisely the added value that banks can really deliver in this environment today. And this without having to rely on the healing promises of platform banking. Be a guide in the digital jungle and protect customers from ill-considered gut decisions. In addition, it is important to include the customer’s background, apart from monetary issues, in the decision-making process. This usually requires a counterpart. Not a digital one, but a human one. A person of heart and soul who generates trust and can provide a place for personal encounter. Today, it is the customer alone who determines where this is located and what it should look like. The same goes for when this meeting takes place. The modern customer expects the best possible service regardless of space and time, not only in view of the phenomenon of digital gadgets.

At a time of fast pace and constant digital transformation, it is ultimately the Bank’s task to invoke traditional values, ensure humanity and meet the need to be an institution that the client trusts. Perhaps even beyond monetary concerns.

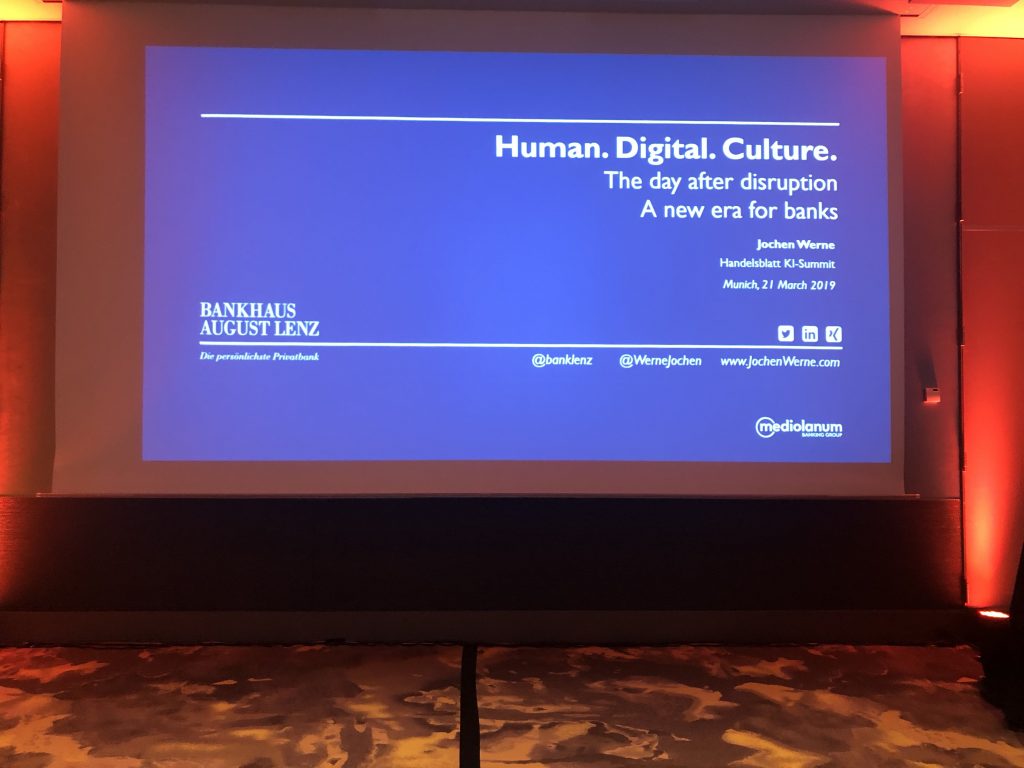

It’s a great pleasure having the chance to meet international experts and supporting the Summit as Speaker on AI in Finance and with an evening fireside chat about leadership, transformation and the sea.

Fireside Chat in der Future Lounge about Leadership in times of transformation

KI-INsights Businessguide

Read interviews and articles from experts in the KI-Businessguide published by the Handelsblatt for the Summit and free to download on this website

It was a pleasure supporting the publication with reflection on AI developments in the Financial Industry called: “Google, how are my stocks doing and what to do?” AI in the financial sector – the next big thing?

AI in Finance Session in the Handelsblatt KI-SUMMIT

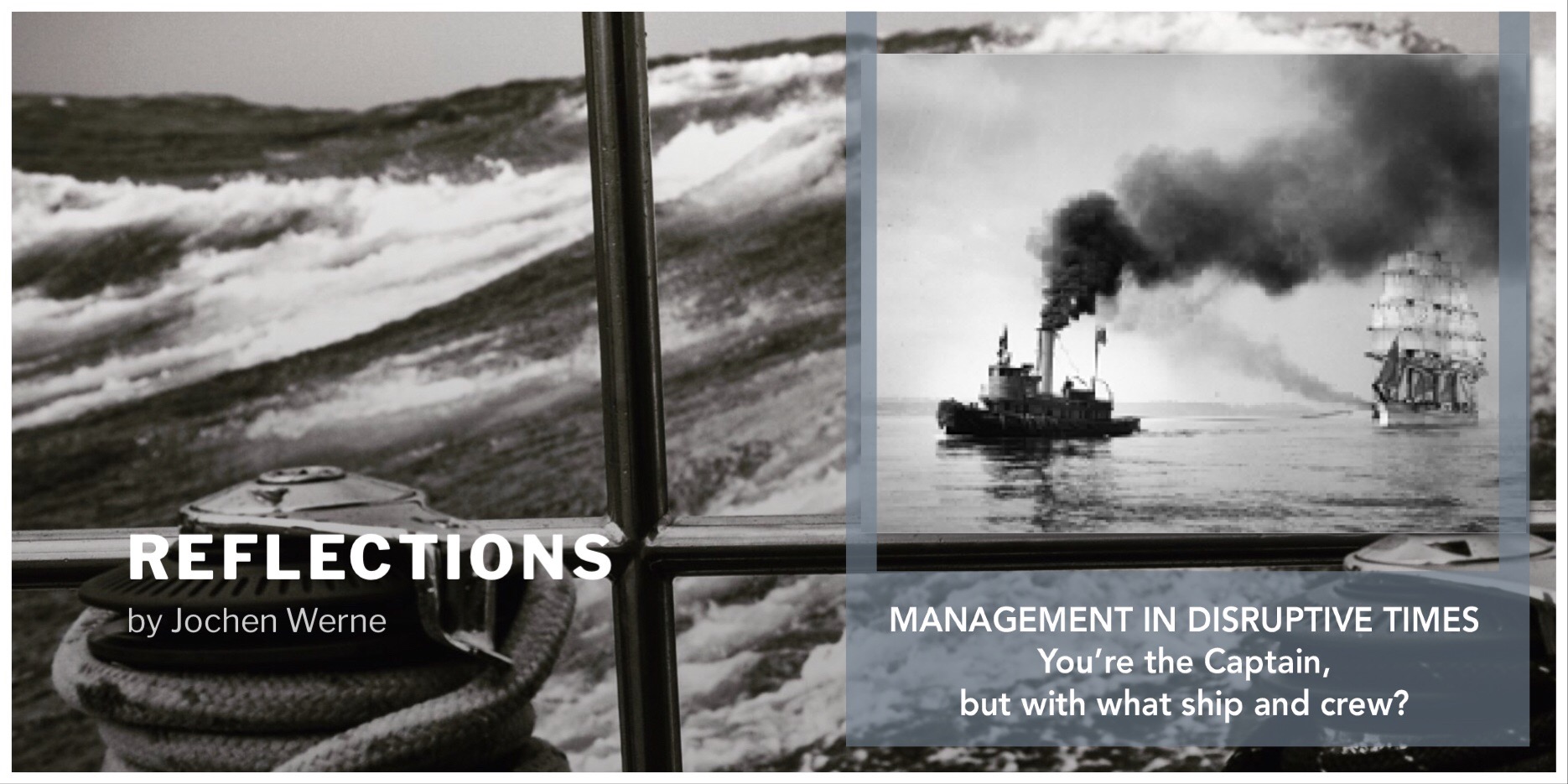

“An analogy for business leaders in the financial industry that compares the challenging times of today’s technological enterprise transformation with the changes during the time of the industrial revolution when steam ships ended the centuries-long era of sailing ships.”

In 1971, the BBC began broadcasting a series on the history of James Onedin, who, as captain and later as shipowner, lived through the stormy times of industrialisation and the conversion of the entire industry from sailing to steam navigation. The series, which takes place in Victorian England in the second half of the 19th century, describes in a special way the subtleties of the interplay of a changing market. New technologies, new skills of market participants, increased conflict potential between entrepreneurs and managers and reorientation in an environment of shrinking margins – special challenges for those who tried to continue their business as before: with sailing ships.

The documentation shows impressively how highly hierarchical organisations like the Royal Navy react and often struggle in times of major technological changes

The captain is responsible for bringing his ship, crew and cargo safely and within a specified time and financial framework to the port of destination. But what if the ship is no longer able to do this and the competition suddenly moves across the blue oceans with completely different ships? What if the shipowner does not have the capacity to trust the new technologies or simply does not have the financial resources to re-equip his fleet? And what about the crew? Does the crew has the necessary skills to sail on the new ships?

Many captains of banks and financial institutions seem to have this scenario all too present. E.g. due to declining customer traffic in bank branches, the high costs for a broad branch network are hardly to be paid today. Germany as a financial centre is “overbanked”, interest rates in the basement – the conditions in Germany for successful banking have never been as challenging as they are now. To this end, customers are continuing to drive change in the industry with their changing demands on digital tools.

Outwaiting a problem or tackling it

The complexity of economic changes has been enormous in every epoch, the difference to current upheavals lies in the temporal component. If companies do not react immediate to market changes today, they might loose their customers faster than ever before. In such disruptive times, all those involved want an “efficient” change process. The only problem is that the term “change” is so omnipresent that it is often perceived as stress and overload. As a result, many levels of management fall into one of the following situations: either they try to sit out the situation and leave change to their successors, or they push many, often less effective measures in an attack of blind actionism. Active, thoughtful and vital change management is often neglected.

More entrepreneurial thinking

Processes of change require both superiors and employees. If the existing situation cannot be improved or adapted at any vertical level, it must be questioned. Concluding, this means for all those involved that situations must always be reflected and corrective measures initiated at an early stage.

Understanding the corporate culture is vital for a successful transformation

In many companies, however, this need for action, which has a high potential for conflict, is often insufficiently communicated. In some places there is a lack of interest for employee issues, a lack of error and conflict culture and a minimal willingness to change. If banks neglect these issues, change processes threaten to fail on a broad basis. This means that managers in a disruptive environment have a natural need for action. The implementation of new strategies, systems and structures and early adaptation to changing market situations are vital factors for survival. A well-known quote by former US President Wodrow Wilson (1913-1921) is particularly valid for today’s highly competitive financial sector: “If you want to make enemies, try to change something.”

Those companies that create the change will share the large financial services market with the new market players and use instruments that did not exist in the classic banking of the past.

Just like James Onedin, who for the longest time was an advocate of classic sailing ships, finally added a modern steamship to his fleet. And to facilitate the change for himself personally, he named the ship after someone he loved.