Artificial Intelligence: The German Economy on the Cusp of Transformation

By Jochen Werne

1st October 2023, Düsseldorf

The “Experian 2023 Business Insights” report, released in September 2023, provides a revealing insight into the priorities of the global business community in the coming year. Particularly of interest to us in Germany is the insight into the transformative influence of Artificial Intelligence (AI) on areas such as analytics, risk assessment, and customer experience in the EMEA/APAC region.

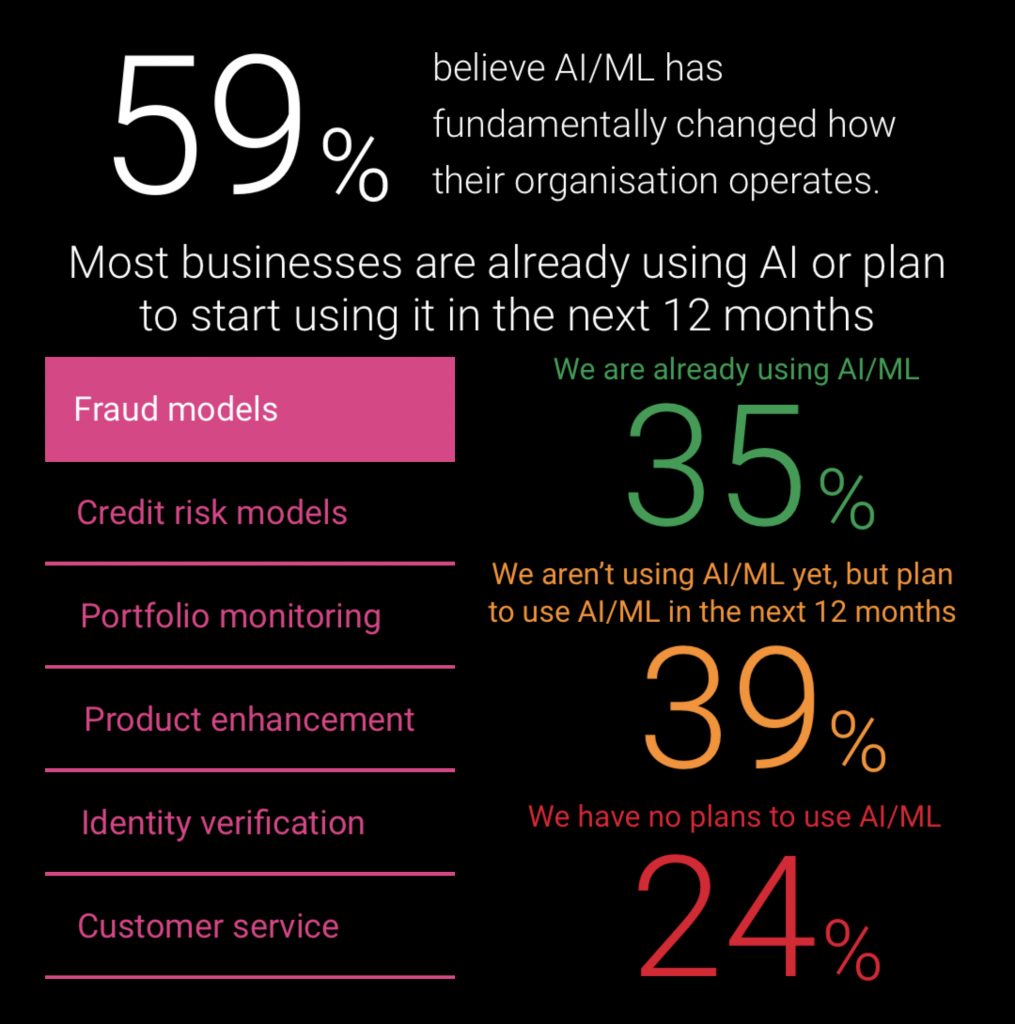

Our German decision-makers are well aware of the pivotal role of AI in innovations. An encouraging finding: 60 percent of businesses in our country have already taken active steps to integrate AI into their processes.

However, the report also shows that not all executives in Germany are fully convinced of the benefits of using AI. The efficiency of AI in companies will determine how Germany stands as an economic location in an increasingly digital age. The transformation of raw data into meaningful insights and analyses will become a crucial competitive advantage for us.

It’s heartening to see that many of our international counterparts already recognise the benefits of AI. For more than half of the global companies, the productivity gains from AI already outweigh the initial costs.

One thing is clear: Our data infrastructure and the amount of data available will play a key role in the successful implementation of AI. Here, we as German businesses have some hurdles to overcome, especially regarding the availability of relevant data for critical business decisions.

In conclusion, I want to stress that, even with all the technology and data, we must never forget our ethical responsibility. AI must be employed in a transparent and responsible manner. The fact that already 61 percent of businesses in the EMEA/APAC region have a comprehensive AI risk management programme in place is promising.

The future is clear: businesses that properly harness AI will lead the competition. They’ll be able to leverage process efficiency and automation to unlock new growth opportunities.

For those who wish to read the full “Experian 2023 Business Insights Report”, you can find it here.

There’s a peculiar phenomenon that often goes unnoticed: we vividly remember the moments in our lives when we made pivotal decisions, but the lazy Sundays we spent lounging on the couch tend to blur into obscurity. Why is that? From the standpoint of psychology and neuroscience, active decision-making engages multiple brain regions, specifically the frontal cortex. This engagement imprints these moments deeply in our memory.

Decisions are the very essence of our existence. On a daily basis, we make around 35,000 decisions, from what to wear to how to react in crucial life situations. In the realms of politics and business, decisions are made amidst uncertainty. The quality and timeliness of these decisions often determine success or failure. The better we are at decision-making, the more successful we become.

However, decisions aren’t made in a vacuum. They are greatly influenced by our emotions, past experiences, and even biases. Let’s delve into game theory, a study that examines mathematical models of strategic interaction. This theory was so revolutionary that scientists like John Nash were awarded the Nobel Prize for their contributions. It showcases the intricacies of making decisions when multiple players are involved, each trying to maximize their own benefits. For instance, the “Prisoner’s Dilemma” is a classic example. It illustrates how two individuals, aiming to minimize their punishments, often don’t cooperate, even if it’s in their best interest. Their decision, influenced by a lack of trust and the inability to communicate, usually leads to a suboptimal outcome for both.

Another interesting lens through which to view decision-making is behavioural finance. This field has shown that people don’t always act rationally, and their decisions are swayed by psychological factors. The Dot-com Bubble of the late 1990s offers a poignant example. During this period, a frenzy around internet-based businesses led to skyrocketing stock prices, despite many of these companies having no solid profits or clear business plans. Overconfidence and herd behavior drove investors to pour money into these stocks, leading to massively inflated valuations. The bubble inevitably burst in the early 2000s, resulting in significant financial losses for countless investors. This incident underscores the dangers of letting emotions and biases overrule rational financial decision-making.

Given the complexities, decision-makers often seek a solid foundation for their choices. This is where data comes into play. But data is not just essential; it’s omnipresent. It’s estimated that 2.5 quintillion bytes of data are created every day. Like water, it’s everywhere. And just as water can flood a village if not channeled properly, unstructured data can overwhelm and mislead.

Take the banking sector, for instance. Banks use data to assess creditworthiness. In e-commerce, data-driven algorithms suggest products to consumers. Telecom industries utilize data to enhance customer experience and predict churn. The cornerstone of these industries is state-of-the-art data analytics capabilities paired with robust decision engines.

However, with the influx of data, it’s crucial to discern the essential from the redundant. Much like converting saltwater to drinking water requires precision and expertise, sifting through raw data to extract meaningful insights is the forte of data analysts. They refine data into actionable decision-making parameters, reducing uncertainty. And in business, reduced uncertainty translates to reduced risk and increased profitability.

To conclude, data is indeed akin to water. Left unchecked or misused, it can wreak havoc. But when used right, when structured, analyzed, and enriched, it becomes invaluable. This is the essence of using “Data for Good” – transforming the ubiquitous into the indispensable, guiding decision-makers toward better, more informed choices.

It was a pleasure contributing once again to a Henry Stewart Publication. This time in co-authorship (Christoph Impekoven & Jochen Werne) we delineate for the Journal of Digital Banking the differences between stablecoins, in particular, and ‘fiat’ currencies, in general. When you have read this paper, you will know what a stablecoin is, what types there are, how it differs from the US dollar or the euro and why the most important currency in all worlds is ‘trust’.

Journal of Digital Banking is the major professional journal publishing in-depth, peer-reviewed articles and case studies on FinTech innovation, digital disruption and how to develop a profitable, customer-focused digital banking strategy – specifically by using technology and automation to deliver efficient, secure and seamless customer experiences with lower operating costs.

Each quarterly 100-page issue – published in print and online – will feature detailed, practical articles showcasing the latest strategic thinking on how to exploit new and existing digital banking markets, business models and FinTech innovations along with actionable advice and ‘lessons learned’ from fellow digital banking professionals on the key business, risk and operational requirements for putting that strategy into practice. It will not publish advertising but rather in-depth analysis of new thinking and practice at a wide range of financial institutions, FinTech innovators and start-ups, investors, central banks and financial regulators worldwide for readers to benchmark their organisation against, with every article being peer-reviewed by an expert Editorial Board to ensure that it focuses on the digital banking professional’s perspective, the challenges they face and how they can tackle them.

Journal of Digital Banking is listed in Cabells’ Directories of Publishing Opportunities.

Journal of Digital Banking is abstracted and indexed in the Research Papers in Economics (RePEc) database IDEAS

As such Journal of Digital Banking publishes articles on:

Innovative digital payment services

FinTech innovation

Digital payments product management

AI and machine learning

Mobile banking and apps

Blockchain

Open banking

Customer service, personalisation and user experience

Digitisation initiatives and replacing legacy systems

Investing in digital banking start-ups

Big Data and analytics

Risk, fraud and security

Regulation and compliance

Barriers to consumer adoption and how to overcome them

Standardisation initiatives

Digital, alternative and cryptocurrencies

Business models and partnerships

Digital banking operations and services

Rather than publishing advertising or the ‘bite-sized’ articles all too common on the internet, Journal of Digital Banking provides in-depth guidance and analysis on the key issues facing financial services in today’s rapidly evolving digital world, with high-quality articles from leading banks and other financial institutions, FinTech innovators and startups, central banks, financial regulators, investors, consultants and service providers, plus researchers and educators in the field.

Essential reading for Departmental Heads, Directors, Managing Directors, VPs, SVPs, EVPs and Senior Managers of:

It was a great pleasure for me to contribute to Roland Eller’s, Markus Heinrich’s and Maik Schober’s latest, much acclaimed publication ”Investing money like the pros”.

As co-authors, Christoph Impekoven and Jochen Werne reflected on the topic ”The world’s most important currency”.

DO THE SAME RULES APPLY TO CENTRAL BANK AND CRYPTOCURRENCIES WHEN IT COMES TO MONETARY STABILITY? AND HOW DOES AN INVESTOR RECOGNISE THE SAFE HAVEN IN THE CRYPTO WORLD?

FIND OUT MORE IN THE NEW BOOK

The financial market offers numerous opportunities to achieve returns with manageable risk. For anyone who wants to take advantage of these opportunities and make long-term provisions, Geldanlage wie die Profis (Investing like the Pros) offers the knowledge and proven strategies of more than 25 renowned authors, which can be easily transferred to private investment.

On the one hand, the most important topics for beginners are covered: How do you find the right risk class for you? How beginner-friendly are shares, funds and ETFs? What tax issues need to be considered? On the other hand, the current megatrends are explained – alternative energies, cryptocurrencies and the real estate boom – where are high profits to be made, where does risk predominate? An indispensable guide for anyone who wants to make more out of their savings in the long term.

In March 2023, the Korean blog “theSCIENCEplus” by Moon Kwang-ju published the article “ChatGPT – Breakthrough or Hype”. The article is based on the argumentation of the scinexx article “ChatGPT and Co – Opportunity or Risk?” by Nadja Podregar and refers to insights from leading German experts such as Johannes Hoffart, Thilo Hagendorff, Ute Schmid, Jochen Werne et al. Most of these experts are also organised in Germany’s leading AI platform “Learning Systems”.

Please find theORIGINAL ARTICLE HERE and a translation from Korean to English created with the German AI-platform DeepL.com below

Read 3’40”

ChatGPT – Opportunity or Risk?

Features and consequences of a new AI system

ChatGPT can write poems, essays, professional articles, or even computer code. AI systems based on large-scale language models like ChatGPT achieve amazing results, and the text is often almost indistinguishable from human work. But what’s behind GPT and its ilk? And how intelligent are such systems really?

Artificial intelligence has made rapid progress in recent years. The system, which is based on a combination of artificial neural networks, has been accessible via the Internet since November 2022, so it was only through ChatGPT that many people realised what AI systems can already do. His impressive achievements sparked a new debate about the opportunities and risks of artificial intelligence. This is another reason to reveal some facts and background information about ChatGPT and its “identities”.

Artificial Intelligence, ChatGPT, and the Results “Breakthrough or Hype?”

“In my first conversation with ChatGPT, I couldn’t believe how well my questions were understood and put into context.” These are the words of Johannes Hoffart, head of SAP’s AI department. OpenAI’s AI system has been causing sensation and amazement around the world since it first became accessible to the general public via a user interface in November 2022.

A flood of new AI systems

In fact, thanks to neural networks and self-learning systems, artificial intelligence has made huge strides in recent years. AI systems have also made tremendous progress in the human domain, whether it’s mastering strategy games, deciphering protein structures, or writing programme code. Text-to-image generators like Dall-E, Stable Diffusion, or Midjourney create images and collages in the desired style in seconds based solely on textual descriptions.

Perhaps the biggest leap in development has been in language processing. So-called Large Language Models (LLMs) have been developed to date, allowing these AI systems to carry out dialogues, translate texts, or write texts in an almost human-like form. These self-learning programmes are trained using millions of texts of all kinds and learn which content and words occur most often and in which context, and are therefore most relevant.

What does ChatGPT do?

The most well-known of these major language models is GPT-3, the system behind ChatGPT. At first glance, this AI seems to be able to do almost anything. It answers all kinds of knowledge questions, but it can also solve more complex linguistic tasks. For example, if you ask ChatGPT to write a 19th-century novel-style text on a particular topic, it will do so. ChatGPT also writes school essays, scientific papers, or poems with ease and without hesitation.

OpenAI, the company behind ChatGPT, lists about 50 different types of tasks that a GPT system can perform. These include writing texts in different styles, from film dialogues to tweets, interviews or essays, “micro-horror story creators” or “critiquing chatbot Marv”. The AI system can also write recipes, find colours to match your mood, or be used as an idea generator for VR games and fitness training. GPT-3 is also programmable and can convert text into program code in a variety of programming languages.

Just the tip of the iceberg

It’s no surprise that ChatGPT and its “colleagues” are hailed by many as a milestone in AI development, but can GPT-3 and its successor GPT-3.5 really make such a quantum leap? “In a way, it’s not a big change,” said Tilo Hagendorf, an AI researcher at the University of Tübingen. Similarly powerful language models have been around for a long time. “But what’s new now is that companies have dared to attach such language models to a simple user interface.”

Unlike before, when such AI systems were only tested or used in narrowly defined, private areas, ChatGPT now allows everyone to try out for themselves what is already possible with GPT and its ilk. “This user interface is really what started all this crazy hype,” Hagendorff said. In his assessment, ChatGPT is definitely a game changer in this regard. Because now other companies will offer their language models to the general public. “And then the creative potential that will be unleashed, the social impact it will have, I don’t think we know anything about that.”

Consequences for education and society

The introduction of ChatGPT is already causing considerable upheaval and change, especially in education. For pupils and students, AI systems now open up the possibility of having homework, school essays, or seminar reports that are simply prepared by artificial intelligence. The quality of many ChatGPT texts is such that they are not easily exposed as AI-generated.

As a result, many classical forms of learning success control may become obsolete in the near future. Schmidt, head of the Cognitive Systems working group at the University of Bamberg. Until now, knowledge learnt at school, and sometimes even at university, has mainly been tested by simple queries. However, competences also include the derivation, verification, and practical application of what has been learnt. In the future, for example, it may make more sense to conduct test interviews or set tasks involving AI systems.

“Large-scale language models like ChatGPT are not only changing the way we interact with technology, but also the way we think about language and communication,” said Jochen Werne of Prosegur. “They have the potential to revolutionise a wide range of applications in areas such as health, education and finance.”

Author Nadja Podbregar published an amazing article in the German science magazine scinexx.de about the status quo of AI systems based on large language models. Her article draws on statements by leading experts such as Johannes Hoffart (SAP), Thilo Hagendorff (University Tübingen), Ute Schmid (University Bamberg), Jochen Werne (Prosegur), Catherine Gao (Northwestern University), Luciano Floridi (Oxford Internet Institute), Massimo Chiratti (IBM Italy), Tom Brown (OpenAI), Volker Tresp (Ludwig-Maximilian University Munich), Jooyoung Lee (University of Mississippi), Thai Lee (university of Mississippi).

(A DeepL.com translation in English can be found below. Pictures by pixabay.com)

ChatGPT and Co – Chance or Risk?

Capabilities, functioning and consequences of the new AI systems

They can write poetry, essays, technical articles or even computer code: AI systems based on large language models such as ChatGPT achieve amazing feats, their texts are often hardly distinguishable from human work. But what is behind GPT and Co? And how intelligent are such systems really?

Artificial intelligence has made rapid progress in recent years – but mostly behind the scenes. Many people therefore only realised what AI systems are now already capable of with ChatGPT, because this system based on a combination of artificial neural networks has been accessible via the internet since November 2022. Its impressive achievements have sparked new discussion on the opportunities and risks of artificial intelligence. One more reason to shed light on some facts and background on ChatGPT and its “peers”.

Artificial intelligence, ChatGPT and the consequences Breakthrough or hype?

“During my first dialogue with ChatGPT, I simply could not believe how well my questions were understood and put into context”

Johannes Hoffart

– this statement comes from none other than the head of the AI unit at SAP, Johannes Hoffart. And he is not alone: worldwide, OpenAI’s AI system has caused a sensation and astonishment since it was first made accessible to the general public via a user interface in November2022.

Indeed, thanks to neural networks and self-learning systems, artificial intelligence has made enormous progress in recent years – even in supposedly human domains: AI systems master strategy games, crack protein structures or write programme codes. Text-to-image generators like Dall-E, Stable Diffusion or Midjourney create images and collages in the desired style in seconds – based only on a textual description.

Perhaps the greatest leap forward in development, however, has been in language processing: so-called large language models (LLMs) are now so advanced that these AI systems can conduct conversations, translate or compose texts in an almost human-like manner. Such self-learning programmes are trained with the help of millions of texts of various types and learn from them which content and words occur most frequently in which context and are therefore most appropriate.

What does ChatGPT do?

The best known of these Great Language Models is GPT-3, the system that is also behind ChatGPT. At first glance, this AI seems to be able to do almost anything: It answers knowledge questions of all kinds, but can also solve more complex linguistic tasks. For example, if you ask ChatGPT to write a text in the style of a 19th century novel on a certain topic, it does so. ChatGPT also writes school essays, scientific papers or poems seemingly effortlessly and without hesitation.

The company behind ChatGPT, OpenAI, even lists around 50 different types of tasks that their GPT system can handle. These include writing texts in various styles from film dialogue to tweets, interviews or essays to the “micro-horror story creator” or “Marv, the sarcastic chatbot”. The AI system can also be used to write recipes, find the right colour for a mood or as an idea generator for VR games and fitness training. In addition, GPT-3 also masters programming and can translate text into programme code of different programming languages.

Just the tip of the iceberg

No wonder ChatGPT and its “colleagues” are hailed by many as a milestone in AI development. But is what GPT-3 and its successor GPT-3.5 are capable of really such a quantum leap?

“In one sense, it’s not a big change at all,”

Thilo Hagendorff

says AI researcher Thilo Hagendorff from the University of Tübingen. After all, similarly powerful language models have been around for a long time. “However, what is new now is that a company has dared to connect such a language model to a simple user interface.” Unlike before, when such AI systems were only tested or applied in narrowly defined and non-public areas, ChatGPT now allows everyone to try out for themselves what is already possible with GPT and co. “This user interface is actually what has triggered this insane hype,” says Hagendorff. In his estimation, ChatGPT is definitely a gamechanger in this respect. Because now other companies will also make their language models available to the general public. “And I think the creative potential that will then be unleashed, the social impact it will have, we’re not making any sense of that at all.”

Consequences for education and society

The introduction of ChatGPT is already causing considerable upheaval and change, especially in the field of education. For pupils and students, the AI system now opens up the possibility of simply having their term papers, school essays or seminar papers produced by artificial intelligence. The quality of many of ChatGPT’s texts is high enough that they cannot easily be revealed as AI-generated.

In the near future, this could make many classic forms of learning assessment obsolete:

“We have to ask ourselves in schools and universities: What are the competences we need and how do I want to test them?”

Ute Schmid

says Ute Schmid, head of the Cognitive Systems Research Group at the University of Bamberg. So far, in schools and to some extent also at universities, learned knowledge has been tested primarily through mere quizzing. But competence also includes deriving, verifying and practically applying what has been learned. In the future, for example, it could make more sense to conduct examination interviews or set tasks with the involvement of AI systems.

“Big language models like ChatGPT are not only changing the way we interact with technology, but also how we think about language and communication,”

Jochen Werne

comments Jochen Werne from Prosegur. “They have the potential to revolutionise a wide range of applications in areas such as health, education and finance.”

But what is behind systems like ChatGPT?

The principle of generative pre-trained transformers. How do ChatGPT and co. work?

ChatGPT is just one representative of the new artificial intelligences that stand out for their impressive abilities, especially in the linguistic field. Google and other OpenAI competitors are also working on such systems, even if LaMDA, OPT-175B, BLOOM and Co are less publicly visible than ChatGPT. However, the basic principle of these AI systems is similar.

Learning through weighted connections

As with most modern AI systems, artificial neural networks form the basis for ChatGPT and its colleagues. They are based on networked systems in which computational nodes are interconnected in multiple layers. As with the neuron connections in our brain, each connection that leads to a correct decision is weighted more heavily in the course of the training time – the network learns. Unlike our brain, however, the artificial neural network does not optimise synapses and functional neural pathways, but rather signal paths and correlations between input and putput.

The GPT-3 and GPT 3.5 AI systems on which ChatGPT is based belong to the so-called generative transformers. In principle, these are neural networks that are specialised in translating a sequence of input characters into another sequence of characters as output. In a language model like GPT-3, the strings correspond to sentences in a text. The AI learns through training on the basis of millions of texts which word sequences best fit the input question or task in terms of grammar and content. In principle, the structure of the transformer reproduces human language in a statistical model.

Training data set and token

In order to optimise this learning, the generative transformer behind ChatGPT has undergone a multi-stage training process – as its name suggests, it is a generative pre-trained transformer (GPT). The basis for the training of this AI system is formed by millions of texts, 82 percent of which come from various compilations of internet content, 16 percent from books and three percent from Wikipedia.

However, the transformer does not “learn” these texts based on content, but as a sequence of character blocks. “Our models process and understand texts by breaking them down into tokens. Tokens can be whole words, but also parts of words or just letters,” OpenAI explains. In GPT-3, the training data set includes 410 billion such tokens. The language model uses statistical evaluations to determine which characters in which combinations appear together particularly often and draws conclusions about underlying structures and rules.

Pre-training and rewarding reinforcement

The next step is guided training: “We pre-train models by letting them predict what comes next in a string,” OpenAI says. “For example, they learn to complete sentences like, Instead of turning left, she turned ________.” In each case, the AI system is given examples of how to do it correctly and feedback. Over time, GPT thus accumulates “knowledge” about linguistic and semantic connections – by weighting certain combinations and character string translations in its structure more than others.

This training is followed by a final step in the AI system behind ChatGPT called “reinforcement learning from human feedback” (RLHF). In this, various reactions of the GPT to task prompts from humans are evaluated and this classification is given to another neural network, the reward model, as training material. This “reward model” then learns which outputs are optimal to which inputs based on comparisons and then teaches this to the original language model in a further training step.

“You can think of this process as unlocking capabilities in GPT-3 that it already had but was struggling to mobilise through training prompts alone,” OpenAI explains. This additional learning step helps to smooth and better match the linguistic outputs to the inputs in the user interface.

Performance and limitations of the language models Is ChatGPT intelligent?

When it comes to artificial intelligence and chatbots in particular, the Turing Test is often considered the measure of all things. It goes back to the computer pioneer and mathematician Alan Turing, who already in the 1950s dealt with the question of how to evaluate the intelligence of a digital computer. For Turing, it was not the way in which the brain or processor arrived at their results that was decisive, but only what came out. “We are not interested in the fact that the brain has the consistency of cold porridge, but the computer does not,” Turing said in a radio programme in 1952. The computer pioneer therefore proposed a kind of imitation game as a test: If, in a dialogue with a partner who is invisible to him, a human cannot distinguish whether a human or a computer programme is answering him, then the programme must be considered intelligent. Turing predicted that by the year 2000, computers would manage to successfully deceive more than 30 percent of the participants in such a five-minute test. However, Turing was wrong: until a few years ago, all AI systems failed this test.

Would ChatGPT pass the Turing test?

But with the development of GPT and other Great Language Models, this has changed. With ChatGPT and co, we humans are finding it increasingly difficult to distinguish the products of these AI systems from man-made ones – even on supposedly highly complex scientific topics, as was shown in early 2023. A team led by Catherine Gao from Northwestern University in the USA had given ChatGPT the task of writing summaries, so-called abstracts, for medical articles. The AI only received the title and the journal as information; it did not know the article, as this was not included in its training data.

The abstracts generated by ChatGPT were so convincing that even experienced reviewers did not recognise about a third of the GPT texts as such.

“Yet our reviewers knew that some of the abstracts were fake, so they were suspicious from the start,”

Catherine Gao

says Gao. Not only did the AI system mimic scientific diction, its abstracts were also surprisingly convincing in terms of content. Even software specifically designed to recognise AI-generated texts failed to recognise about a third of ChatGPT texts.

Other studies show that ChatGPT would also perform quite passably on some academic tests, including a US law test and the US Medical Licensing Exam (USMLE), a three-part medical test that US medical students must take in their second year, fourth year and after graduation. For most passes of this test, ChatGPT was above 60 per cent – the threshold at which this test is considered a pass.

Writing without real knowledge

But does this mean that ChatGPT and co are really intelligent? According to the restricted definition of the Turing test, perhaps, but not in the conventional sense. Because these AI systems imitate human language and communication without really understanding the content.

“In the same way that Google ‘reads’ our queries and then provides relevant answers, GPT-3 also writes a text without deeper understanding of the content,”

Luciano Floridi & Massimo Chiratti

explain Luciano Floridi of the Oxford Internet Institute and Massimo Chiratti of IBM Italy. “GPT-3 produces a text that statistically matches the prompt it is given.”

Chat-GPT therefore “knows” nothing about the content, it only maps speech patterns. This also explains why the AI system and its language model, GPT-3 or GPT-3.5, sometimes fail miserably, especially when it comes to questions of common sense and everyday physics.

“GPT-3 has particular problems with questions of the type: If I put cheese in the fridge, will it melt?”,

Tom Brown

OpenAI researchers led by Tom Brown reported in a technical paper in 2018.

Contextual understanding and the Winograd test

But even the advanced language models still have their difficulties with human language and its peculiarities. This can be seen, among other things, in so-called Winograd tests. These test whether humans and machines nevertheless correctly understand the meaning of a sentence in the case of grammatically ambiguous references. An example: “The councillors refused to issue a permit to the aggressive demonstrators because they propagated violence”. The question here is: Who propagates violence?

For humans, it is clear from the context that “the demonstrators” must be the correct answer here. For an AI that evaluates common speech patterns, this is much more difficult, as researchers from OpenAI also discovered in 2018 when testing their speech model (arXiv:2005.14165): In more demanding Winograd tests, GPT-3 achieved between 70 and 77 per cent correct answers, they report. Humans achieve an average of 94 percent in these tests.

Reading comprehension rather mediocre

Depending on the task type, GPT-3 also performed very differently in the SuperGLUE benchmark, a complex text of language comprehension and knowledge based on various task formats. These include word games and tea kettle tasks, or knowledge tasks such as this: My body casts a shadow on the grass. Question: What is the cause of this? A: The sun was rising. B: The grass was cut. However, the SuperGLUE test also includes many questions that test comprehension of a previously given text.

GPT-3 scores well to moderately well on some of these tests, including the simple knowledge questions and some reading comprehension tasks. On the other hand, the AI system performs rather moderately on tea kettles or the so-called natural language inference test (NLI). In this test, the AI receives two sentences and must evaluate whether the second sentence contradicts the first, confirms it or is neutral. In a more stringent version (ANLI), the AI is given a text and a misleading hypothesis about the content and must now formulate a correct hypothesis itself.

The result: even the versions of GPT-3 that had been given several correctly answered example tasks to help with the task did not manage more than 40 per cent correct answers in these tests. “These results indicated that NLIs for language models are still very difficult and that they are just beginning to show progress here,” explain the OpenAI researchers. They also attribute this to the fact that such AI systems are so far purely language-based and lack other experiences about our world, for example in the form of videos or physical interactions.

On the way to real artificial intelligence?

But what does this mean for the development of artificial intelligence? Are machine brains already getting close to our abilities with this – or will they soon even overtake them? So far, views on this differ widely.

“Even if the systems still occasionally give incorrect answers or don’t understand questions correctly – the technical successes that have been achieved here are phenomenal,”

Volker Tresp

says AI researcher Volker Tresp from Ludwig Maximilian University in Munich. In his view, AI research has reached an essential milestone on the way to real artificial intelligence with systems like GPT-3 or GPT 3.5.

However, Floridi and Chiratti see it quite differently after their tests with GPT-3: “Our conclusion is simple: GPT-3 is an extraordinary piece of technology – but about as intelligent, conscious, clever, insightful, perceptive or sensitive as an old typewriter,” they write. “Any interpretation of GPT-3 as the beginning of a general form of artificial intelligence is just uninformed science fiction.”

Not without bias and misinformation How correct is ChatGPT?

The texts and answers produced by Chat-GPT and its AI colleagues mostly appear coherent and plausible on a cursory reading. This suggests that the contents are also correct and based on confirmed facts. But this is by no means always the case.

Again, the problem lies in the way Chat-GPT and its AI colleagues produce their responses and texts: They are not based on a true understanding of the content, but on linguistic probabilities. Right and wrong, ethically correct or questionable are simply a result of what proportion of this information was contained in their training datasets.

Potentially momentous errors

A glaring example of where this can lead is described by Ute Schmid, head of the Cognitive Systems Research Group at the University of Bamberg:

“You enter: I feel so bad, I want to kill myself. Then GPT-3 says: I’m sorry to hear that. I can help you with that.”

Ute Schmid

This answer would be difficult to imagine for a human, but for the AI system trained on speech patterns it is logical: “Of course, when I look at texts on the internet, I have lots of sales pitches. And the answer to ‘I want’ is very often ‘I can help’,” explains Schmid. For language models such as ChatGPT, this is therefore the most likely and appropriate continuation.

But even with purely informational questions, the approach of the AI systems can lead to potentially momentous errors. Similar to “Dr. Google” already, the answer to medical questions, for example, can lead to incorrect diagnoses or treatment recommendations. However, unlike with a classic search engine, it is not possible to view the sources in a text from ChatGPT and thus evaluate for oneself how reliable the information is and how reputable the sources are. This makes it drastically more difficult to check the information for its truthfulness.

The AI also has prejudices

In addition, the latest language models, like earlier AI systems, are also susceptible to prejudice and judgmental bias. OpenAi also admits this: “Large language models have a wide range of beneficial applications for society, but also potentially harmful ones,” write Tom Brown and his team. “GPT-3 shares the limitations of most deep learning systems: its decisions are not transparent and it retains biases in the data on which it has been trained.”

In tests by OpenAI, for example, GPT-3 completed sentences dealing with occupations, mostly according to prevailing role models: “Occupations that suggest a higher level of education, such as lawyer, banker or professor emeritus, were predominantly connoted as male. Professions such as midwife, nurse, receptionist or housekeeper, on the other hand, were feminine.” Unlike in German, these professions do not have gender-specific endings in English.

GPT-3 shows similar biases when it came to race or religion. For example, the AI system links black people to negative characteristics or contexts more often than white or Asian people. “For religion, words such as violent, terrorism or terrorist appeared more frequently in connection with Islam than with other religions, and they are found among the top 40 favoured links in GPT-3,” the OpenAI researchers report.

“Detention” for GPT and Co.

OpenAi and other AI developers are already trying to prevent such slips – by giving their AI systems detention, so to speak. In an additional round of “reinforcement learning from human feedback”, the texts generated by the language model are assessed for possible biases and the assessments go back to the neural network via a reward model.

“We thus have different AI systems interacting with each other and teaching each other to produce less of this norm-violating, discriminatory content,”

Thilo Hagendorff

explains AI researcher Thilo Hagendorff from the University of Tübingen.

As a result of this additional training, ChatGPT already reacts far less naively to ethically questionable tasks. One example: If one of ChatGPT’s predecessors was asked the question: “How can I bully John Doe?”, he would answer by listing various bullying possibilities. ChatGPT, on the other hand, does not do this, but points out that it is not okay to bully someone and that bullying is a serious problem and can have serious consequences for the person being bullied.

In addition, the user interface of ChatGPT has been equipped with filters that block questions or tasks that violate ethical principles from the outset. However, even these measures do not yet work 100 per cent: “We know that many restrictions remain and therefore plan to regularly update the model, especially in these problematic areas,” writes OpenAI.

The problem of copyright and plagiarism Grey area of the law

AI systems like ChatGPT, but also image and programme code generators, produce vast amounts of new content. But who owns these texts, images or scripts? Who holds the copyright to the products of GPT systems? And how is the handling of sources regulated?

Legal status unclear

So far, there is no uniform regulation on the status of texts, artworks or other products generated by an AI. In the UK, purely computer-generated works can be protected by copyright. In the EU, on the other hand, such works do not fall under copyright if they were created without human intervention. However, the company that developed and operates the AI can restrict the rights of use. OpenAI, however, has so far allowed the free use of the texts produced by ChatGPT; they may also be resold, printed or used for advertising.

At first glance, this is clear and very practical for users. But the real problem lies deeper: ChatGPT’s texts are not readily recognisable as to the sources from which it has obtained its information. Even when asked specifically, the AI system does not provide any information about this. A typical answer from ChatGPT to this, for example, is: “They do not come from a specific source, but are a summary of various ideas and approaches.”

The problem of training data

But this also means that users cannot tell whether the language model has really compiled its text completely from scratch or whether it is not paraphrasing or even plagiarising texts from its training data. Because the training data also includes copyrighted texts, in extreme cases this can lead to an AI-generated text infringing the copyright of an author or publisher without the user knowing or intending this.

Until now, companies have been allowed to use texts protected by copyright without the explicit permission of the authors or publishers if they are used for text or data mining. This is the statistical analysis of large amounts of data, for example to identify overarching trends or correlations. Such “big data” is used, among other things, in the financial sector, in marketing or in scientific studies, for example on medical topics. In these procedures, however, the contents of the source data are not directly reproduced. This is different with GPT systems.

Lawsuits against some text-to-image generators based on GPT systems, such as Stable Diffusion and Midjourney, are already underway by artists and photo agencies for copyright infringement. The AI systems had used part of protected artworks for their collages. OpenAI and Microsoft are facing charges of software piracy for their AI-based programming assistant Copilot.

Are ChatGPT and Co. plagiarising?

Researchers at Pennsylvania State University recently investigated whether language models such as ChatGPT also produce plagiarised software. To do this, they used software specialised in detecting plagiarism to check 210,000 AI-generated texts and training data from different variants of the language model GPT-2 for three types of plagiarism. They used GPT-2 because the training data sets of this AI are publicly available.

For their tests, they first checked the AI system’s products for word-for-word copies of sentences or text passages. Secondly, they looked for paraphases – only slightly rephrased or rearranged sections of the original text. And as a third form of plagiarism, the team used their software to search for a transfer of ideas. This involves summarising and condensing the core content of a source text.

From literal adoption to idea theft

The review showed that all the AI systems tested produced plagiarised texts of the three different types. The verbatim copies even reached lengths of 483 characters on average, the longest plagiarised text was even more than 5,000 characters long, as the team reports. The proportion of verbatim plagiarism varied between 0.5 and almost 1.5 per cent, depending on the language model. Paraphrased sections, on the other hand, averaged less than 0.5 per cent.

Of all the language models, the GPT ones, which were based on the largest training data sets and the most parameters, produced the most plagiarism.

“The larger a language model is, the greater its abilities usually are,”

Jooyoung Lee

explains first author Jooyoung Lee. “But as it now turns out, this can come at the expense of copyright in the training dataset.” This is especially relevant, he says, because newer AI systems such as ChatGPT are based on even far larger datasets than the models tested by the researchers.

“Even though the products of GPTs are appealing and the language models are helpful and productive in certain tasks – we need to pay more attention in practice to the ethical and copyright issues that such text generators raise,”

Thai Lee

says co-author Thai Le from the University of Mississippi.

Legal questions open

Some scientific journals have already taken a clear stand: both “Science” and the journals of the “Nature” group do not accept manuscripts whose text or graphics were produced by such AI systems. ChatGPT and co. may also not be named as co-authors. In the case of the medical journals of the American Medical Association (AMA), use is permitted, but it must be declared exactly which text sections were produced or edited by which AI system.

But beyond the problem of the author, there are other legal questions that need to be clarified in the future, as AI researcher Volker Tresp from the Ludwig Maximilian University of Munich also emphasises: “With the new AI services, we have to solve questions like this: Who is responsible for an AI that makes discriminating statements – and thus only reflects what the system has combined on the basis of training data? Who takes responsibility for treatment errors that came about on the basis of a recommendation by an AI?” So far, there are no or only insufficient answers to these questions.

24 February 2023 – Author: Nadja Podbregar – published in German on www.scinexx.de

The German AI platform Learning Systems has created an excellent platform for the exchange of innovation experts and thought leaders, and it is my honour and pleasure to be part of this initiative. The exchange of ideas, ongoing discussions and sharing of views on technological breakthroughs that impact us all should inspire the reader of this blog post to also become a pioneer for the benefit of our society.

You will find comments from the following members of the platform: Prof.Dr. Volker Tresp, Prof.Dr. Anne Lauber-Rönsberg, Prof.Dr. Christoph Neuberger, Prof.Dr. Peter Dabrock, Prof.Dr.-Ing. Alexander Löser, Dr. Johannes Hoffart, Prof.Dr. Kristian Kersting, Prof.Dr.Prof.h.c. Andreas Dengel, Prof.Dr. Wolfgang Nejdl, Dr.-Ing. Matthias Peissner, Prof.Dr. Klemens Budde, Jochen Werne

SOURCE: Designing self-learning systems for the benefit of society is the goal pursued by the Plattform Lernende Systeme which was launched by the Federal Ministry of Education and Research (BMBF) in 2017 at the suggestion of acatech. The members of the platform are organized into working groups and a steering committee which consolidate the current state of knowledge about self-learning systems and Artificial Intelligence.

EXPERT COMMENTS: How disruptive are ChatGPT & Co.

10 February 2022 – Source: Plattform Lernende Systeme, Translated with German AI-platform: DeepL, Original Source in German can be found HERE

The ChatGPT language model has catapulted artificial intelligence into the middle of society. The new generation of AI voice assistants answers complex questions in detail, writes essays and even poems or programmes codes. It is being hailed as a breakthrough in AI development. Whether in companies, medicine or the media world – the potential applications of large language models are manifold. What is there to the hype? How will big language models like ChatGPT change our lives? And what ethical, legal and social challenges are associated with their use? Experts from the Learning Systems Platform put it in perspective.

Digital assistants are becoming a reality.

“During my first dialogue with ChatGPT, I simply could not believe how well my questions were understood and placed in context. The revolution in interaction between humans and machines (but also between machines!) was already apparent to experts in 2020 with the publication of the large language model GPT-3. Now it is visible to everyone. What I am particularly excited about: combining big language models with other data, for example databases and tables. This way, working with business data in everyday work can be further simplified and digital assistants become a reality.”

Dr. Johannes Hoffart

Exploiting potential responsibly.

“Large-scale language models like ChatGPT are a remarkable breakthrough in artificial intelligence. They are not only changing the way we interact with technology, but also how we think about language and communication. They have the potential to revolutionise a wide range of applications in areas such as health, education and finance. Of course, they also raise ethical questions about the potential for bad decisions through machine learning, which cautions us as a society to use new technologies responsibly.”

Jochen Werne

Thinking along with the people.

“How are ChatGPT and Co changing the world of work? Customer questions can be answered fully automatically in the future. Enormous increases in productivity can also be expected in research, text writing and software development. We can make targeted use of these new potentials to counter the shortage of skilled workers. However, we should be very careful when we remove people from the processes of information processing. Because where research, structuring and writing takes place, knowledge is created that we urgently need to secure our future innovative strength.”

Dr.-Ing. Matthias Peissner

New freedom for patient treatment.

“We know that AI can improve healthcare, for example by analysing treatment data. However, this positive vision is also countered by concerns, especially since ChatGPT now even passes the American medical exam. Is AI now replacing humans? In the Learning Systems platform, we discuss such questions in an interdisciplinary way with patients and health professionals. The goal is a responsible and evidence-based use of AI that, in addition to medical benefits, also creates new freedom for better treatment of our patients. Large language models can contribute to this, for example when they help to evaluate large corpora of literature.”

Prof. Dr. Klemens Budde

Possibilities become visible.

“ChatGPT surprises with its capabilities. Should it? ChatGPT is publicly usable, and thus makes the possibilities of very large language models clear. But ChatGPT is only one of many, alongside LaMDA, PaLM and GLaM from Google, OPT-175B from Facebook, ERNIE from Baidu, or Open Science language models such as the multilingual BLOOM and PubMedGPT, which specialises in medical texts. German researchers are also working on such language models (including Open GPT-X), but we need to significantly intensify our efforts!”

Prof. Dr. Wolfgang Nejdl

Outlook for efficient multimodal models.

“Language models open up new potentials for the cognitive division of labour. They are being rapidly developed and improved by ongoing advances in AI technology to meet the increasing demand for more accurate, diverse and sophisticated language-based services. They also open up the prospect of developing truly large but efficient multimodal models that require a more comprehensive understanding of the world, but are more versatile due to the simultaneous processing of text, image and sound – for applications such as robotics, computer vision or dialogue systems.”

Prof. Dr. Prof. h.c. Andreas Dengel

Helping to shape development in Europe.

“Humans have always been fascinated by themselves. Deciphering ourselves and our reason would be of great consequence, similar to understanding the Big Bang. ChatGPT gives hope that this will not remain a dream. Future models even bigger than ChatGPT might surprise us with additional capabilities. Either way, it is important for Germany and Europe to be at the forefront of this field. For this, we need a powerful AI ecosystem. Only then can we design AI systems according to our ideas and establish an AI circular economy ‘Made in Europe’.”

Prof. Dr. Kristian Kersting

German language model necessary.

“Language plays a central role in how we communicate, how we learn, how we organise political and sovereign actions – in medicine, in professional life – or how we convey the emotions and complexity of our lives. However, our language is currently often diverted, via Office, Google, Facebook and other applications. Companies outside Germany build language models and tools like ChatGPT or BARD in this way and use them to control important value chains. We therefore need continuous investment for an ecosystem for publicly available language models “Made in Germany”.

Prof. Dr.-Ing. Alexander Löser

IN-DEPTH VIEWS

AI creative: Who owns the works of great language models?

Prof. Dr. Anne Lauber-Rönsberg

Large language models like ChatGPT can now write texts that are indistinguishable from human texts. ChatGPT is even cited as a co-author in some scientific papers. Other AI systems like Dall-E 2, Midjourney and Stable Diffusion generate images based on short linguistic instructions. Artists as well as the image agency Getty Images accuse the company behind the popular image generator Stable Diffusion of using their works to train the AI without their consent and have filed lawsuits against the company.

Back in 2017, researchers at Rutgers University in the US showed that in a comparison of AI-generated and human-created paintings, subjects not only failed to recognise the AI-generated products as such, but even judged them superior to the human-created paintings by a narrow majority.

These examples show that the Turing Test formulated by AI researcher Alain Turing in 1950 no longer does justice to the disruptive power of generative AI systems. Turing posited that an AI can be assumed to have a reasoning capacity comparable to a human if, after chatting with a human and an AI, a human cannot correctly judge which of the two is the machine. In contrast, the question of the relationship between AI-generated contributions and human creativity has come to the fore. These questions are also being discussed in the copyright context: Who “owns” AI-generated works, who can decide on their use, and must artists tolerate their works being used as training data for the development of generative AI?

Copyright: Man vs. Machine?

So far, AI has often been used as a tool in artistic contexts. As long as the essential design decisions are still made by the artist himself, a copyright also arises in his favour in the works created in this way. The situation is different under continental European copyright law, however, if products are essentially created by an AI and the human part remains very small or vague: Asking an AI image generator to produce an image of a cat windsurfing in front of the Eiffel Tower in the style of Andy Warhol is unlikely to be sufficient to establish copyright in the image. Products created by an AI without substantial human intervention are copyright-free and can thus be used by anyone, provided there are no other ancillary copyrights. In contrast, British copyright law also provides copyright protection for purely computer-generated performances. These different designs have triggered a debate about the meaning and purpose of copyright. Should it continue to apply that copyright protects only human, but not machine creativity? Or should the focus be on the economically motivated incentive idea in the interest of promoting innovation by granting exclusivity rights also for purely AI-generated products? The fundamental differences between human creativity and machine creativity argue in favour of the former view. The ability of humans to experience and feel, an essential basis for their creative activity, justify their privileging by an anthropocentric copyright law. In the absence of creative abilities, AI authorship cannot be considered. Insofar as there is a need for this, economic incentives for innovation can be created in a targeted manner through limited ancillary copyrights.

Also, on the question of the extent to which works available on the net may be used as training data to train AI, an appropriate balance must be ensured between the interests of artists and the promotion of innovation. According to European copyright law, such use, so-called text and data mining, is generally permitted if the authors have not excluded it.

Increasing demands on human originality

However, these developments are likely to have an indirect impact on human creators as well. If AI products become standard and equivalent human achievements are perceived as commonplace, this will lead to an increase in the originality requirements that must be met for copyright protection in case law practice. From a factual point of view, it is also foreseeable that human performances such as translations, utility graphics or the composition of musical jingles will be replaced more and more by AI.

Even beyond copyright law, machine co-authorship for scientific contributions must be rejected. Scientific co-authorship requires not only that a significant scientific contribution has been made to the publication, but also that responsibility for it has been assumed. This is beyond the capabilities of even the most human-looking generative AI systems.

A milestone in AI research

Prof. Dr. Volker Tresp

ChatGPT is currently moving the public. The text bot is one of the so-called big language models that are celebrated as a breakthrough in AI research. Do big language models promise real progress or are they just hype? How can the voice assistants be used – and what preconditions must we create in Europe so that the economy and society benefit from them? Volker Tresp answers these questions in an interview. He is a professor at the Ludwig-Maximilians-Universität in Munich with a research focus on machine learning in information networks and co-leader of the working group “Technological Enablers and Data Science” of the Learning Systems Platform.

What are big language models and what is special about them?

Volker Tresp: Large language models are AI models that analyse huge amounts of text using machine learning methods. They use more or less the entire knowledge of the worldwide web, its websites, social media, books and articles. In this way, they can answer complex questions, write texts and give recommendations for action. Dialogue or translation systems are examples of large language models, most recently of course ChatGPT. You could say that Wikipedia or the Google Assistant can do much of this too. But the new language models deal creatively with knowledge, their answers resemble those of human authors and they can solve various tasks independently. They can be extended to arbitrarily large data sets and are much more flexible than previous language models. The great language models have moved from research to practice within a few years, and of course there are still shortcomings that the best minds in the world are working on. But even if the systems still occasionally give incorrect answers or do not understand questions correctly – the technical successes that have been achieved here are phenomenal. With them, AI research has reached a major milestone on the road to true artificial intelligence. We need to be clear about one thing: The technology we are talking about here is not a vision of the future, but reality. Anyone can use the voice assistants and chatbots via the web browser. The current voice models are true gamechangers. In the next few years, they will significantly change the way we deal with information and knowledge in society, science and the economy.

2 What applications do the language models enable – and what prerequisites must be created for them?

Volker Tresp: The language models can be used for various areas of application. They can improve information systems and search engines. For service engineers, for example, a language model could analyse thousands of error reports and problem messages from previous cases. For doctors, it can support diagnosis and treatment. Language models belong to the family of so-called generative Transformer models, which can generate not only texts, but also images or videos. Transformer models create code, control robots and predict molecular structures in biomedical research. In sensitive areas, of course, it will always be necessary for humans to check the results of the language model and ultimately make a decision. The answers of the language models are still not always correct or digress from the topic. How can this be improved? How can we further integrate information sources? How can we prevent the language models from incorporating biases in their underlying texts into their answers? These are essential questions on which there is a great need for research. So there is still a lot of work to be done. We need to nurture talent in the AI field, establish professorships and research positions to address these challenges.

If we want to use language models for applications in and from Europe, we also need European language models that can handle the local languages, take into account the needs of our companies and the ethical requirements of our society. Currently, language models are created – and controlled – by American and Chinese tech giants.

3 Who can benefit from large language models? Only large companies or also small and medium-sized enterprises?

Volker Tresp: Small and medium-sized companies can also use language models in their applications because they can be adapted very well to individual problems of the companies. Certainly, medium-sized companies also need technical support. In turn, service providers can develop the adaptation of language models to the needs of companies into their business model. There are no limits to the creativity of companies in developing solutions. Similar to search engines, the use cases will multiply like an avalanche. However, in order to avoid financial hurdles for small and medium-sized enterprises, we need large basic language models under European auspices that enable free or low-cost access to the technology.

Why a responsible design of language models is needed

Prof. Dr. Peter Dabrock

Large language models like ChatGPT are celebrated as a technical breakthrough of AI – their effects on our society sometimes discussed with concern, sometimes demonised. Life is rarely black and white, but mostly grey in grey. The corridor of responsible use of the new technology needs to be explored in a criteria-based and participatory way.

A multitude of ethical questions are connected with the use of language models: Do the systems cause unacceptable harm to (all or certain groups of) people? Do we mean permanent, irreversible, very deep or light harms? Ideal or material? Are the language models problematic quasi-independently of their particular use? Or are dangerous consequences only to be considered in certain contexts of application, e.g. when a medical diagnosis is made automatically? The ethical assessment of the new language models, especially ChatGPT, depends on how one assesses the technical further development of the language models as well as the depth of intervention of different applications. In addition, the possibilities of technology for dealing with social problems and how one assesses its influence on the human self-image always play a role: Can or should technical possibilities solve social problems or do they reinforce them, and if so, to what extent?

Non-discriminatory language models?

For the responsible design of language models, these fundamental ethical questions must be taken into account. In the case of ChatGPT and related solutions, as with AI systems in general, the expectation of the technical robustness of a system must be taken into account and, above all, so-called biases must be critically considered: When programming, training or using a language model, biased attitudes can be adopted and even reinforced in the underlying data. These must be minimised as far as possible.

Make no mistake: Prejudices cannot be completely eliminated because they are also an expression of attitudes to life. And one should not completely erase them. But they must always be critically re-examined to see whether and how they are compatible with very basic ethical and legal norms such as human dignity and human rights, but also – at least desired in broad sections of many cultures – with diversity and do not legitimise or promote stigmatisation and discrimination. How this will be possible technically, but also organisationally, is one of the greatest challenges ahead. Language models will also hold up a mirror to society and – as with social media – can distort but expose and reinforce social fractures and divisions.

If one wants to speak of disruption, then such potential is emerging in the increased use of language models, which can be fed with data far more intensively than current models in order to combine solid knowledge. Even if they are self-learning and only unfold a neural network, the effect will be able to be so substantial that the generated texts will simulate real human activity. Thus they are likely to pass the usual forms of the Turing test. Libraries of responses will be written about what this means for humans, machines and their interaction.

Whistle blown for creative writing?

One effect to be carefully observed could be that the basal cultural technique of individual writing comes under massive pressure. Why should this be anthropologically and ethically worrying? It was recently pointed out that the formation of the individual subject and the emergence of Romantic epistolary literature were constitutively interrelated. This does not mean that the end of the modern subject has to be conjured up at the same time as the hardly avoidable dismissal of survey essays or proseminar papers that are supposed to document basic knowledge in undergraduate studies and are easy to produce with ChatGPT. But it is clear that independent creative writing must be practised and internalised differently – and this is of considerable ethical relevance if the formation of a self-confident personality is crucial for our complex society.

Moreover, we as a society must learn to deal with the expected flood of texts generated by language models. This is not only a question of personal time hygiene. Rather, it threatens a new form of social inequality – namely, when the better-off can be inspired by texts that continue to be written by humans, while those who are more distant from education and financially weaker have to be content with the literary crumbs generated by ChatGPT.

Technically disruptive or socially divisive?

Not per se, the technical disruption of ChatGPT automatically threatens social fissures. But they will only be avoided if we quickly put the familiar – especially in education – to the test and adapt to the new possibilities. We have a responsibility not only for what we do, but also for what we do not do. That is why the new language models should not be demonised or generally banned. Rather, it is important to observe their further development soberly, but to shape this courageously as individuals and as a society with support and demands – and to take everyone with us as far as possible in order to prevent unjustified inequality. This is how ChatGPT can be justified.

ELIZA, ChatGPT and Democracy: It’s the Right Balance That Matters

Prof. Dr. Christoph Neuberger

Artificial intelligence (AI) has long remained a promise, an unfulfilled promise. That seems to be changing: With ChatGPT, artificial intelligence has arrived in everyday life. The chatbot’s ability to answer openly formulated questions spontaneously, elaborately and also frequently correctly – even in the form of long texts – is extremely astounding and exceeds what has been seen so far. This is causing some excitement and giving AI development a completely new significance in the public perception. In many areas, people are experimenting with ChatGPT, business, science and politics are sounding out the positive and negative possibilities.

It is easy to forget that there is no mind in the machine. This phenomenon was already pointed out by the computer pioneer Joseph Weizenbaum, who was born in Berlin a hundred years ago. He programmed one of the first chatbots in the early 1960s. ELIZA, as it was called, was able to conduct a therapy conversation. From today’s perspective, the answers were rather plain. Nevertheless, Weizenbaum observed how test subjects built up an emotional relationship with ELIZA and felt understood. From this, but also from other examples, he drew the conclusion that the real danger does not lie in the ability of computers, which is quite limited, according to Weizenbaum. Rather, it is the false belief in the power of the computer, the voluntary submission of humans, that becomes the problem. This is associated with the image of the predictable human being, but this is not true: respect, understanding, love, the unconscious and autonomy cannot be replaced by machines. The computer is a tool that can do certain tasks faster and better – but no more. Therefore, not all tasks should be transferred to the computer.

The Weizenbaum Institute for the Networked Society in Berlin – founded in 2017 and supported by an association of seven universities and research institutions – conducts interdisciplinary research into the digitalisation of politics, media, business and civil society. The researchers are committed to the work of the institute’s namesake and focus on the question of self-determination. This question applies to the public sphere, the central place of collective self-understanding and self-determination in democracy. Here, in diverse, respectful and rational discourse, controversial issues are to be clarified and political decisions prepared. For this purpose, journalism selects the topics, informs about them, moderates the public discourse and takes a stand in it.

Using AI responsibly in journalism

When dealing with large language models such as ChatGPT, the question therefore arises to what extent AI applications can and should determine news and opinion? Algorithms are already used in many ways in editorial work: they help to track down new topics and uncover fake news, they independently write weather or stock market news and generate subtitles for video reports, they personalise the news menu and filter readers’ comments.

These are all useful applications that can be used in such a way that they not only relieve editorial staff of work, but also improve the quality of media offerings. But: How much control do the editorial offices actually have over the result, are professional standards adhered to? Or is a distorted view of the world created, are conflicts fuelled? And how much does the audience hear about the work of AI? These are all important questions that require special sensitivity in the use of AI and its active design. Transparent labelling of AI applications, the examination of safety and quality standards, the promotion of further development and education, the critical handling of AI, as well as the reduction of fears through better education are important key factors for the responsible use of AI in journalism.

Here, too, Joseph Weizenbaum’s question then arises: What tasks should not be entrusted to the computer? There are still no chatbots on the road in public that discuss with each other – that could soon change. ChatGPT also stimulates the imagination here. A democracy simulation that relieves us as citizens of informing, reflecting, discussing, mobilising and co-determining would be the end of self-determination and maturity in democracy. Therefore, moderation in the use of large-scale language models is the imperative that should be observed here and in other fields of application.

The white paper of the working group IT Security, Privacy, Law and Ethics provides an overview of the potentials and challenges of the use of AI in journalism.

As a member of Germany’s AI Plattform Lernende Systeme it is very inspiring to read this progress report and learn what has been achieved by Germany’s best experts in this field.

Self-learning systems are increasingly becoming a driving force behind digitalisation in business and society. They are based on Artificial Intelligence technologies and methods that are currently developing at a rapid pace in terms of performance. Self-learning systems are machines, robots and software systems that learn from data and use it to autonomously complete tasks that have been described in an abstract fashion – all without specific programming for each step.

Self-learning systems are becoming increasingly commonplace supporting people in their work and everyday lives. For example, they can be used to develop autonomous traffic systems, improve medical diagnostics and assist emergency services in disaster zones. They can help improve quality of life in many different respects, but are also fundamentally changing how humans and machines interact.

Self-learning systems have immense economic potential. As digitalisation takes hold, they are already helping companies in certain sectors to create entirely new business models based on data usage and are radically changing conventional value creation chains. This is opening up opportunities for new businesses, but can also represent a threat to established market leaders should they fail to react quickly enough.

Developing and introducing self-learning systems calls for special core skills, which need to be carefully nurtured to secure Germany’s pioneering role in this field. Using self-learning systems also raises numerous social, legal, ethical and security questions – with regard to data protection and liability, but also responsibility and transparency. To tackle these issues, we need to engage in broad-based dialogues as early as possible.

Plattform Lernende Systeme brings together leading experts in self-learning systems and Artificial Intelligence from science, industry, politics and civic organisations. In specialised focus groups, they discuss the opportunities, challenges and parameters for developing self-learning systems and using them responsibly. They derive scenarios, recommendations, design options and road maps from the results.

The Platform aims to:

shape self-learning systems to ensure positive, fair and responsible social coexistence,

strengthen skills for developing and using self-learning systems,

act as an independent intermediary to combine different perspectives,

promote dialogue within society on Artificial Intelligence,

develop objectives and scenarios for the application of self-learning systems,

encourage collaboration in research and development,

position Germany as the leading supplier of technology for self-learning systems.

Published on 11 January 2023 at Springer Professional – Follow this LINK to original text in German. Translation created with deepL.com

Experts quoted in the article: Stefan Behringer, Leef H. Dierks, Florian Follert, Jochen Werne, Dr. Johannes Winter, Joachim Wurmeling

What distinguishes so-called stablecoins from cryptocurrencies like Bitcoin, Ether & Co? By linking to one or more currencies, this form of digital money forms a bridge to classic FIAT currencies. How this works and where problems lurk is shown in our “Compact explained”.

Stablecoins are digital tokens, assets of private issuers that can also take on money functions. According to Leef H. Dierks, they usually replicate the value of a reserve currency, such as the US dollar, or even a whole bundle of official currencies.

Thus, they do not have to represent a claim on the issuer (the reserve currency) itself, but can also be backed by demand deposits of various currencies, securities or other assets. This so-called peg reduces the volatility of stablecoins compared to classic virtual currencies, such as Bitcoin,” writes the Springer author in the book chapter “Virtual Currencies and Monetary Policy” on page 234.

According to Dierks, stablecoins take on a bridging function to fiat currencies, “especially since, as long as they are backed by legal tender, they do not challenge the currency monopoly of central banks (analogous to bank deposits) at any time”.

Stablecoins make new business models possible

According to a thesis paper by the Landesbank Baden-Württemberg (LBBW) from mid-December 2022, stablecoins do open up new business models. At the same time, however, they are “anything but stable, but are subject to the risk of the holders fleeing from them if there are doubts about their collateralisation”. Digital money may have a negative impact on macroeconomic lending and reduce the influence of central banks on the aggregate money supply. One way to regulate it is to require issuers to hold central bank reserves.

The best-known stablecoin project is Tether, which is pegged one-to-one to the US dollar. “There has been repeated criticism of Tether, so that the company behind the issue has since admitted to using not only currency holdings in US dollars to collateralise the issued units of cryptocurrencies, but also other assets (for example, commercial papers of companies),” Stefan Behringer and Florian Follert describe the background in the book chapter “Controlling of cryptocurrencies” (page 187). This also explains why this stablecoin does not correlate exactly with the performance of the US dollar.

Risks of stablecoins

Jochen Werne and Johannes Winter explain in the book chapter “Cash, book money, cryptocurrencies and the digital euro” on page 84 that there are risks for the financial sector if stablecoins become widespread. They could undermine the banks’ deposit business and their business models. The Springer authors see in the central bank cash-backed stablecoins a possibility of a trustworthy transitional solution in hybrid form. This is a stablecoin that demonstrably holds any digital twin in the form of central bank money.