It was a great pleasure for me to contribute to Roland Eller’s, Markus Heinrich’s and Maik Schober’s latest, much acclaimed publication ”Investing money like the pros”.

As co-authors, Christoph Impekoven and Jochen Werne reflected on the topic ”The world’s most important currency”.

DO THE SAME RULES APPLY TO CENTRAL BANK AND CRYPTOCURRENCIES WHEN IT COMES TO MONETARY STABILITY? AND HOW DOES AN INVESTOR RECOGNISE THE SAFE HAVEN IN THE CRYPTO WORLD?

FIND OUT MORE IN THE NEW BOOK

The financial market offers numerous opportunities to achieve returns with manageable risk. For anyone who wants to take advantage of these opportunities and make long-term provisions, Geldanlage wie die Profis (Investing like the Pros) offers the knowledge and proven strategies of more than 25 renowned authors, which can be easily transferred to private investment.

On the one hand, the most important topics for beginners are covered: How do you find the right risk class for you? How beginner-friendly are shares, funds and ETFs? What tax issues need to be considered? On the other hand, the current megatrends are explained – alternative energies, cryptocurrencies and the real estate boom – where are high profits to be made, where does risk predominate? An indispensable guide for anyone who wants to make more out of their savings in the long term.

Published on 11 January 2023 at Springer Professional – Follow this LINK to original text in German. Translation created with deepL.com

Experts quoted in the article: Stefan Behringer, Leef H. Dierks, Florian Follert, Jochen Werne, Dr. Johannes Winter, Joachim Wurmeling

What distinguishes so-called stablecoins from cryptocurrencies like Bitcoin, Ether & Co? By linking to one or more currencies, this form of digital money forms a bridge to classic FIAT currencies. How this works and where problems lurk is shown in our “Compact explained”.

Stablecoins are digital tokens, assets of private issuers that can also take on money functions. According to Leef H. Dierks, they usually replicate the value of a reserve currency, such as the US dollar, or even a whole bundle of official currencies.

Thus, they do not have to represent a claim on the issuer (the reserve currency) itself, but can also be backed by demand deposits of various currencies, securities or other assets. This so-called peg reduces the volatility of stablecoins compared to classic virtual currencies, such as Bitcoin,” writes the Springer author in the book chapter “Virtual Currencies and Monetary Policy” on page 234.

According to Dierks, stablecoins take on a bridging function to fiat currencies, “especially since, as long as they are backed by legal tender, they do not challenge the currency monopoly of central banks (analogous to bank deposits) at any time”.

Stablecoins make new business models possible

According to a thesis paper by the Landesbank Baden-Württemberg (LBBW) from mid-December 2022, stablecoins do open up new business models. At the same time, however, they are “anything but stable, but are subject to the risk of the holders fleeing from them if there are doubts about their collateralisation”. Digital money may have a negative impact on macroeconomic lending and reduce the influence of central banks on the aggregate money supply. One way to regulate it is to require issuers to hold central bank reserves.

The best-known stablecoin project is Tether, which is pegged one-to-one to the US dollar. “There has been repeated criticism of Tether, so that the company behind the issue has since admitted to using not only currency holdings in US dollars to collateralise the issued units of cryptocurrencies, but also other assets (for example, commercial papers of companies),” Stefan Behringer and Florian Follert describe the background in the book chapter “Controlling of cryptocurrencies” (page 187). This also explains why this stablecoin does not correlate exactly with the performance of the US dollar.

Risks of stablecoins

Jochen Werne and Johannes Winter explain in the book chapter “Cash, book money, cryptocurrencies and the digital euro” on page 84 that there are risks for the financial sector if stablecoins become widespread. They could undermine the banks’ deposit business and their business models. The Springer authors see in the central bank cash-backed stablecoins a possibility of a trustworthy transitional solution in hybrid form. This is a stablecoin that demonstrably holds any digital twin in the form of central bank money.

“Due to the tradability of the tokens, the flexibility of book money is paired with the guarantee of physical central bank money. Even the expected damage from a successful attack on the underlying blockchain could thus be minimised, since an unlawful acquisition of power of disposal over assets is quickly restricted in its usability. A regulated expert function guarantees that only central bank money or a digital twin is traded and thus the central supervisory function always lies with the central bank,” say Werne and Winter.

MiCA forms future legal framework

With the Markets in Crypto Assets (MiCA) regulation, the European Union has sewn a legal garment for the crypto industry in the 26 EU states. The new EU regulation is to enter into force by the beginning of 2023 and become effective 18 months later vis-à-vis all market participants.

“MiCA responds to the growth of the cryptoasset ecosystem and integrates a large number of new players into the European supervisory space,” explains Joachim Wurmeling, member of the Executive Board of the Deutsche Bundesbank, in a guest article on the occasion of the Bundesbank Symposium in November 2022. “In future, crypto service providers and issuers of crypto assets will not only have to ensure that the risks arising from the cryptoasset business are adequately managed; they will also have to apply for authorisation to issue crypto assets or to provide crypto services and be subject to ongoing supervision.”

In addition, he said, the regulation also applies to traditional financial institutions that provide services around cryptoassets. The regulatory approach for MiCA is new and is emerging alongside the traditional structure.

It was a pleasure contributing in co-authorship with the AI-expert and friend Dr. Johannes Winter / Jochen Werne to this new Springer Gabler publication ”Praxisbeispiele der Digitalisierung” (Best Practice of Digitilisation) which is available now as e-book and paperback at https://link.springer.com/book/10.1007/978-3-658-37903-2

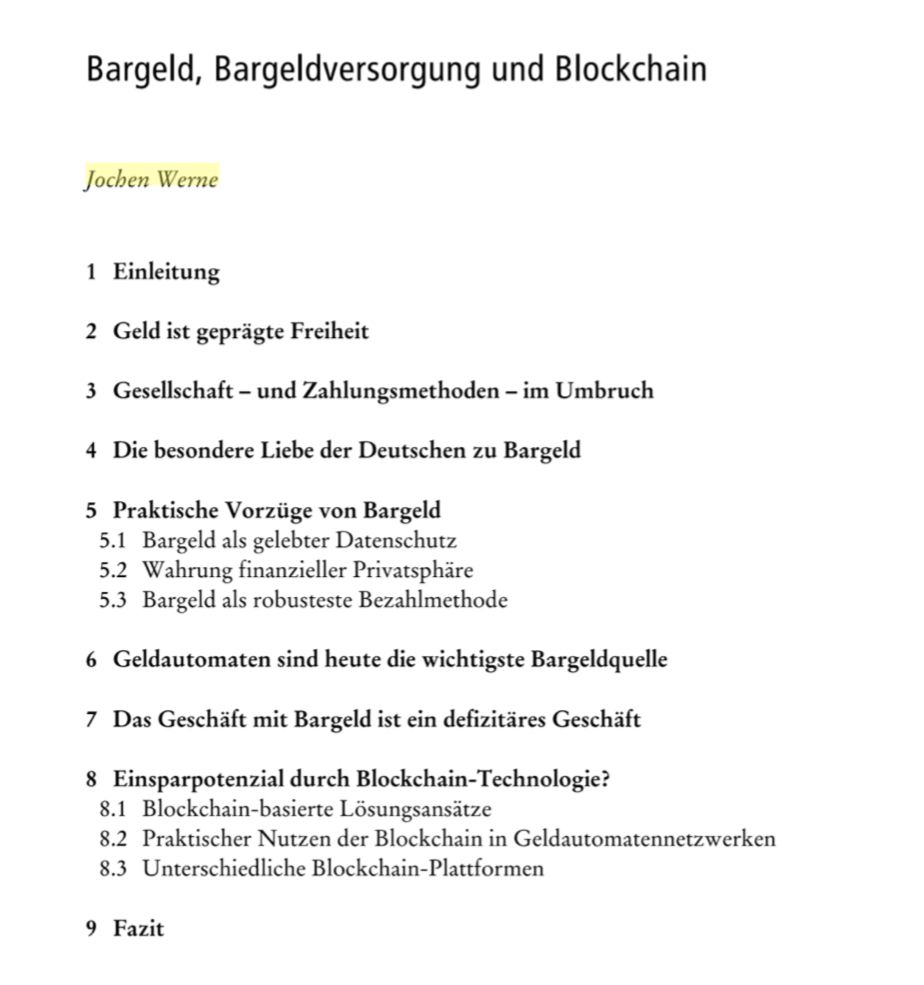

Cash, Book Money, Crypto Currencies and the Digital Euro

The aim of the chapter in the book is a contribution to the debate of money in the digital age. It combines historical insights into the meaning of money with the latest technological developments, to compare visions of the financial industry with realities and to develop options for action to shape the digital transformation of money.

Abstract: In a world where tech companies are leading campaigns to create a new cryptocurrency and bitcoin is surpassing the US$50,000 mark because a visionary electric car maker wants to recognise the cryptocurrency as a means of payment, some fundamental questions arise: how must money be defined in a digital world to reliably fulfil the characteristics of a universally recognised store of value and medium of exchange? And what changes are in store for the financial industry when so-called stablecoins proliferate and challenge the banks’ classic deposit business and their outdated business models? The aim of this contribution to the debate is to combine historical insights into the meaning of money with the latest technological developments in the digital age, to compare visions of the financial industry with realities and to develop options for action for shaping the digital transformation of money.

Thomas Apitzsch, Michael Pfleger, Frederike HaberlandPages 309-325

About Springer Gabler

Springer Gabler Verlag is the leading specialist publisher for the business sector. Its classic and digital teaching materials and specialist media address current business questions and provide reliable, practical solutions.

Source: Die Welt – original language German | Translated by deepl.com

International security company Prosegur stores cryptocurrencies in super-secret locations without internet access. Partner O₂ Telefónica makes the communication possible and ensures that it is secure.

Looking at money, it quickly becomes clear that times have changed. In the ten biggest bank robberies, around 1.5 billion euros were taken, all told. In crypto hacks, it was around 3.9 billion euros in 2021 alone, according to the analysis company Crystal.

Jochen Werne is not surprised. “Anything of value arouses covetousness.” Werne is Chief Development Officer and Chief Visionary Officer Prosegur Germany. He develops new services for the German subsidiary of the international security group. Prosegur Crypto GmbH offers such a service, Werne is managing director: a custodian for digital assets – without an internet connection.

New money, new risks, new security concepts

Security world market leader Prosegur is famous for its yellow money carriers and became big in the cash business. With the boom of cryptocurrencies, new demands came to the company with headquarters in Madrid. The goal: to be able to offer the world’s most secure storage method for cryptocurrencies. In Germany, Prosegur works together with the business customer division of O2 Telefónica. Together, they are setting themselves up at a new level of security – the highest level, because billions in Bitcoin, Ethereum and other digital currencies are at stake.

“Our goal is to help give the new ecosystem the trust it deserves through security components,” says Werne. “Our history is closely intertwined with the security of any asset. Crypto custody is a logical evolution of our business.”

O2 networks vaults and money

O2 Telefónica is taking over the communication for Prosegur Germany, and completely. Karsten Pradel, Director B2B at O2 Telefónica, explains: “It starts with the mobile phone service for 3300 employees. In addition, around 1,000 of Prosegur’s yellow armoured cars and networked safes are equipped with a Global SIM from O2 Telefónica. In this way, the armoured vans and the security boxes are directly and securely connected to Prosegur’s company network. Via GPS, the routes of cash transporters can be documented and secured.”

O2 also provides fast fibre-optic access and secures internal communication against external access with VPN (Virtual Private Network) access. A completely new feature is a software-controlled data network (SD-WAN): this allows the Prosegur data traffic to be controlled intelligently and quickly.

In this way, the environment at the site can be secured against threats – where the internet traffic originates. An intelligent component links all communication paths and always selects the best one. This has three advantages, says Sören Jahnke, Global Solutions Engineer at O2 Telefónica: “A lot of bandwidth at a low price, more redundancy and thus communication security (because copper cable, fibre or mobile are used depending on availability and demand) and a better user experience because the services work better: ‘Everything runs much faster'”.

Where it gets critical is when people and the internet come into play

Prosegur aims to offer the ultimate crypto custody method. Yet transactions in cryptocurrencies are actually secure. Their cash book is the blockchain. That’s where the crypto money is stored. The blockchain is a digital document; digital copies of this document are stored simultaneously on a large number of computers – this makes it forgery-proof. When a transaction is made, the data chain contained in the document is supplemented in all copies by a data block that can never be deleted again.

However, it becomes critical when people and the internet come into play. Anyone who trades in cryptocurrencies needs a wallet. This is a kind of digital wallet. The wallet software in turn creates a digital signature and processes a transaction with the owner’s private key. Only in this way does the owner gain access to his crypto treasures stored in the blockchain and can use them. “You can always trace every step, what happened when and where,” says Jochen Werne.

Danger for assets and for people

This wallet can be made available in an app or on a computer and is usually connected to the internet. This is called a “hot wallet” – it is convenient because transactions can be made quickly, but it is vulnerable to hacker attacks. A “cold wallet” (also called “cold storage”) works without direct internet access – this can be a USB stick, for example. This form of asset storage has two problems. Firstly, a cold wallet can be the target of an extortionist or robber, just like a gold bar or large amounts of cash stored at home. Secondly, cold wallets are only secure as long as they are disconnected from the internet.

“For us, cold storage is not enough,” says Jochen Werne. “Because having large assets at the disposal of only one person not only endangers the assets, but also the person who has that power of disposal. Here, criminals not only resort to direct threats of violence on this person, but they often also threaten family members.” Prosegur Crypto therefore takes a different approach. The company stores customer data in a hardware security module (HSM). The technology works in much the same way as we would expect in an agent film.

No chance for “Ocean’s Eleven”

“This is a computer in a military-standard shielded case that is kept in one of our high-security facilities and is not connected to the internet,” Werne explains. If, contrary to all expectations, such a device should fall into the wrong hands, it deletes the stored data. Security protocols then stipulate that the data can be reconstructed via a highly complex system equipped with appropriate codes. Prosegur has a whole range of high-security facilities. The locations of the crypto-bunkers are, of course, secret.

“The entire security is fully electronically monitored with various modules and security protocols on several levels. These are smart fences, for example, where possible threats are analysed by artificial intelligence,” says Werne. Even an attack like in the film “Ocean’s Eleven” – George Clooney’s crew simply turns off the power there – would not work.

“WE BELIEVE WE CAN OFFER THE MOST SECURE CUSTODY METHOD FOR CRYPTO ASSETS IN THE WORLD”

JOCHEN WERNE Chief Development Officer and Chief Visionary Officer Prosegur Germany

And yet Prosegur customers can initiate blockchain transactions online – what follows is a sophisticated process. In the process, the hardware security module connects to a computer network that makes blockchain transactions possible.

The technology comes from GK8, a company specialising in crypto technology; the method used here is so-called multi-party computing (MPC). The transaction is transferred to the user’s blockchain via several security instances, using a patented technology that does not require a direct connection to the internet. This secures the critical moment of the transaction. “Everything else stays in cold storage” – most of the time the crypto assets are in the Prosegur high-security vault, without an internet connection. Jochen Werne: “We believe that we can offer the most secure custody method for crypto assets in the world. Currently, we are preparing to launch this service with the appropriate licensing in the strictly regulated German market as well.”

Digital assets are as safe as their encryption? Unfortunately not. After all, the dangers do not only come from hackers. Security must be thought of more broadly, as examples of state-of-the-art crypto custody solutions show.

The protection of crypto assets can only be guaranteed if there is a clear awareness of the dangers. Attacks on digital assets such as cryptocurrencies or asstes no longer end with the numerous attack vectors of cyberattacks, but unfortunately already extend to the use of physical force against their owners. It is therefore important to raise awareness of possible dangers, as shown by examples of the state of today’s state-of-the-art crypto custody solutions.

According to Investing.com, the total number of cryptocurrencies as of 12 December 2021 is 9,004 with a total market capitalisation of US$2.24 trillion. After Bitcoin, Ether, XRP, Litecoin and co, the Libra Coin initiated by Facebook received unprecedented media attention, triggered by the announcement of the project alone. And the emotionality and sharpness with which the discussion was conducted shows how seriously the topic is taken internationally at the state level. It is about reputation, influence, control, responsibility and only in the last instance about technology. And for every investor, it is first and foremost about protecting his assets.

The right sense of danger

In the future, protecting our assets will not just mean keeping our wallet in the deepest pocket of our jacket or handbag or turning the key to our flat twice in the lock. In the future, we will have invested part of the fruits of our labour, our fortunes, in crypto investments and cryptocurrencies. This part of our wealth needs to be kept safe, and we need to understand exactly where and how. This requires that we understand the risks. The sense of danger must therefore adapt, as must the lure of the new opportunities. For this, it is of utmost importance to understand the real dangers and to take appropriate protective measures.

As yet, however, this sense does not seem to be all that pronounced. According to Slowmist Hacked , which specialises in aggregating information on detected attacks on blockchain projects, apps and tokens, the total amount of crypto assets stolen in 122 different attacks in 2020 is $3.78 billion. Even though the evaluation is based on the Bitcoin peaks of January 2021, it clearly shows the importance of greater efficiency in security.

In comparison, only 1.63 billion US dollars were captured in the ten largest bank robberies of all time. Considering that the largest robbery took place when dictator Saddam Hussein ordered his son Qusay to withdraw nearly US$1 billion from Iraq’s central bank with a handwritten note, and the tenth largest robbery netted the perpetrators just US$18.9 million, crypto-cybercrime has become an extremely lucrative business.

Crypto custody: Do hot and cold wallets offer sufficient security?

The famous military scientist Carl von Clausewitz argued in the early 19th century: “An army on the defensive, without fortifications, has a hundred vulnerable points; it is a body without armour”. “We must always retain sufficient forces beyond the garrisons to be a match for the enemy in the open field, unless we can rely on the arrival of an ally to relieve our fortresses and free our army.” In cryptocurrencies, the wallet is the fortress and the blockchain – the distributed ledger – is the army in the open field. It is the job of modern crypto custodians – as guardians of their clients’ assets – to ask themselves daily what additional measures can be taken to best protect cryptocurrencies and crypto assets.

Crypto custody solutions typically involve a combination of hot storage or crypto custody that is connected to the internet and cold storage or crypto custody that is not. Rakesh Sharma comments on Investopia, “Both types of storage have advantages and disadvantages. For example, hot storage is connected to the internet and therefore offers better liquidity. But hot storage options can be vulnerable to hacks due to online presence. Cold storage solutions offer more security. However, it can be difficult to generate liquidity from crypto holdings in the short term because they are offline. Vaulting is a combination of both types of cryptocurrency custody solutions, where the majority of funds are stored offline and can only be accessed with a private key.”

The risk of becoming a victim of physical violence in private crypto custody

The risk of theft of crypto assets is no longer solely about digital robbery in cyberattacks and hacks. Physical violence against the owner of crypto assets or threats to family members is already sadly present. In November 2021, for example, the American co-founder of Tuenti, once billed as the Spanish Facebook, Zaryn Dentzel, was the victim of such an attack in his private Madrid flat.

Dentzel stated on record that the gangsters beat him and stabbed him in the chest with a knife while shooting him several times with a Taser.

Thus it becomes clear that the protection of crypto-assets must also go hand in hand with the fact that a perpetrator who is prepared to use physical force understands in advance that his alleged victim does not readily have power of disposal over his total crypto-assets. Cold storage not at home, but in a cold space, for example a high-security facility, can provide the necessary protection.

State of the art crypto storage meets high security facilities

In July 2021, Prosegur Crypto – the crypto custody subsidiary of Prosegur, one of the largest security companies in the world – announced the creation of the world’s first “digital asset custody bunker”. The consistent combination of a physically and digitally inaccessible environment here is unique to date.

In collaboration with cybersecurity company GK8, Prosegur Crypto brings together all the infrastructure, facilities, technologies and security protocols required to minimise all risk areas identified in the digital asset custody chain.

The solution consists of state-of-the-art cyber security systems provided by GK8’s patented technology and the highest level of a military-grade secured protection environment. It is based on a “360° inaccessibility” approach, mapping over 100 protection measures into 6 integrated layers of security. This ensures the highest possible protection against physical and cyber attacks.

The HSM (hardware security module, a device that generates, stores and protects cryptographic keys) is housed in a military grade briefcase within the high security vault. This vault is only accessible to a limited number of people who manage the data manually and offline. Staff have restricted access to the information they handle to avoid any risk of internal theft and work from a secure facility where there is no risk of physical attack, copying or theft of systems or passwords. In the event of an unauthorised attempt to access the HSM, its contents are permanently deleted. Immediately, a recovery plan is activated, including a protocol for recovering private keys using seeds located in various other vaults.

The module is connected to an MPC (Multi-party Computation) system, which provides a fast signature process on a state-of-the-art computer network and generates transactions on the blockchain without a direct internet connection. This minimises the possibility of fraudulent access and eliminates any potential vector for cyber attacks. These system features are patented and represent a highly differentiated offering in the market.

Plea for openness: danger recognised – danger averted

The analysis shows that from Clausewitz to the latest developments in cyber security and crypto-custody, the security perspective has hardly changed. The more you rely on a single system or fortress, the more vulnerable you are. It’s all about layered security, which makes it time-consuming and very costly for attackers to get what they desperately want.

We are still only at the beginning of a new era for our monetary systems. An era driven by technology in which it is increasingly important for every actor to develop a good understanding of it in order to build sustainable ones. Technology has never been right or wrong, only the way we humans use it can make it so.

New technologies offer the opportunity to make our world more prosperous for all – let’s use it!

Ein Plädoyer für Vertrauen in einer Zeit des Misstrauens. Vertrauen ist die Grundlage, auf der Währungssysteme aufgebaut sind. Vertrauen bildet die Basis internationaler diplomatischer Beziehungen und ist die Grundlage für jeden Fortschritt.

Doch was passiert, wenn das Vertrauen einmal erschüttert ist?

Der aktuelle diplomatische Streit um einen milliardenschweren U-Boot-Vertrag, die Sorge um einen neuen kalten Krieg und der Zusammenbruch des Bretton-Woods-Systems vor genau 50 Jahren sind das Manuskript für diese maritim angehauchte französisch-amerikanische Geschichte über Geld und Vertrauen. Sie ist ein Lehrstück für unsere heutige Zeit, wo wir das Entstehen von Kryptofinanzmärkten miterleben und somit an der Schwelle zu einer neuen Form des Geldes stehen.

Nach dem traditionellen langen Sommerurlaub, erwacht Frankreich im September wie jedes Jahr aus dem kurzen selbst kreierten Dornröschenschlaf. Das Leben beginnt seinen gewohnten Gang zu nehmen, auch wenn manch einer noch in Erinnerungen schwelgt und dabei vielleicht die ersten Vorboten post-Covid-sorgenfreien Lebens genießt. Nicht so Philippe Étienne. Für ihn beginnt auf der anderen Seite des Atlantik, im für diese Zeit eigentlich malerischen Washington, der Herbst mit einem diplomatischen Gewittersturm. Ein Unwetter, das selbst für den 65-jährigen grau-melierten eloquenten Botschafter Frankreichs neu gewesen sein dürfte. 6 160 Kilometer entfernt beschließt im Élysée-Palast Président de la République Emmanuel Macron seinen Spitzendiplomaten in den USA, samt seines australischen Amtskollegen Jean-Pierre Thebault, zu Konsultationen nach Paris abzuberufen. Der in der französisch-amerikanischen Geschichte einmalige Akt wird von Außenminister Jean-Yves Le Drian mit der „außergewöhnlichen Schwere“ einer australisch-britisch-amerikanischen Ankündigung gerechtfertigt und mit den Worten „Lüge“, „Doppelzüngigkeit“, „Missachtung“ und „ernste Krise“ eindrucksvoll unterstrichen.

Im Mittelpunkt dieser Krise steht die überraschende Ankündigung der genannten Länder ab sofort ein strategisches trilaterales Sicherheitsbündnis (AUKUS) einzugehen. Ein Bündnis, welches auch die Beschaffung atomgetriebener U-Boote für Australien vorsieht und somit einen bereits 2016 initiierten 56 Milliarden Euro schweren französisch-australischen U-Boot- Auftrag quasi ad acta legt. Der Abschluss des Abkommens fällt in einen Zeitraum in welchem US-Präsident Joe Biden vor der UN-Generalversammlung beteuert: „Wir streben nicht – ich wiederhole: wir streben nicht – einen neuen kalten Krieg oder eine in starre Blöcke geteilte Welt an“. Über diesen sogenannten „neuen kalten Krieg“ zwischen den USA und China sprechen Experten, wie der bekannte Historiker Niall Ferguson jedoch bereits seit 2019. Es geht hierbei nicht um atomares Wettrüsten, sondern vielmehr um die Technologievorherrschaft in Cyber Security, Künstlicher Intelligenz und Quantum Computing. Auch wenn nukleargetriebene U-Boote im Zentrum des diplomatischen Disputs stehen, so stellt man im AUKUS-Abkommen doch schnell fest, dass die Zusammenarbeit in den oben genannten Feldern einer der wichtigsten Bestandteile des Vertrags ist. Ein Ziel, welches vielleicht auch mit französischen Interessen kongruent ist. Doch geht es im Streit zwischen den alten Freunden im ersten Moment weniger um das „Was“, sondern viel mehr um das diplomatische „Wie“ – das heißt, um den Vertrauensbruch, der ausgelöst wird, wenn man enge Bündnispartner einfach vor vollendete Tatsachen stellt. Tatsachen, die sie auch finanziell und persönlich betreffen.

Denn Geld und Vertrauen sind eng verwoben. Das Vertrauen einer Bank, dass der Gläubiger seine Schulden zurückbezahlt. Das Vertrauen eines Bürgers, dass die Währung, in der er oder sie ihre Gehälter ausbezahlt bekommt, stabil ist. Das Vertrauen eines Staates in ein Währungssystem, dass die dort getroffenen Vereinbarungen von allen eingehalten werden. Georg Simmel bringt es in seiner „Philosophie des Geldes” so auf den Punkt: „Geld ist die vielleicht konzentrierteste und zugespitzteste Form und Äußerung des Vertrauens in die gesellschaftlich-staatliche Ordnung.“

Eine weiteres französisch-amerikanisches Vertrauensbruchsmelodrama mit maritimer Untermalung jährt sich in diesem Jahr zum 50. Mal. Die bewegenden Ereignisse des 6. August 1971 beschreibt Benn Steil, Senior Fellow des Council on Foreign Relations, in seinem Buch „The Battle of Bretton Woods“ wie folgt: „…ein Unterausschuss des Kongresses gab einen Bericht mit dem Titel ´Action Now to Strengthen the US-Dollar` heraus, der paradoxerweise zu dem Schluss kam, dass der Dollar geschwächt werden müsse. Das Dollar-Dumping beschleunigte sich und Frankreich schickte ein Kriegsschiff, um französisches Gold aus den Tresoren der New Yorker Fed abzuholen.“

Diese dramatisch anmutende Geste des damaligen französischen Präsidenten Georges Pompidou im finalen Akt des Zusammenbruchs des Bretton-Woods Systems wirkt auf den ersten Blick genauso befremdlich wie der Abzug der Botschafter heute. Die Basis jedoch ähnelt sich und lag damals wie heute in einem ebenfalls erschütterten Vertrauen zwischen den doch so eng verwobenen großen Nationen. Ohne tiefer auf die nach dem Zweiten Weltkrieg geschaffene neue Währungsordnung mit dem US-Dollar als Ankerwährung eingehen zu wollen, ist es wichtig den im „White Plan“ offensichtlichen Grund des französischen Aufbegehrens zu verstehen. Der Plan sah vor, dass die USA den Bretton-Woods-Teilnehmerstaaten garantierten, Gold auf unbestimmte Zeit zum festen Kurs von 35 US-Dollar pro Unze kaufen und verkaufen zu dürfen. Das Dilemma dieser Regelung wurde früh sichtbar. Denn bereits Ende der 1950er Jahren überstiegen die bei ausländischen Zentralbanken befindlichen Dollarbestände die Goldreserven der USA. Als der französische Präsident Charles de Gaulle 1966 die USA aufforderte die französischen Dollarreserven gegen Gold zu tauschen, reichten die Goldvorräte der FED, nur für etwa die Hälfte. Der immer tiefer sich verankernde Vertrauensverlust zwang den amerikanische Präsidenten Richard Nixon am 15. August 1971 die nominale Goldbindung aufzukündigen und der sogenannte „Nixon-Schock“ beendete das System wie es war.

Und dort wo etwas endet kann oder wird zwangsläufig etwas Neues beginnen.

Heute leben wir in einer Welt, in der die Stabilität unserer Währung auf unserem Vertrauen in die staatliche Finanzpolitik, der Wirtschaftskraft unseres Landes und auf der guten Arbeit einer unabhängigen Zentralbank beruht. Wir leben jedoch auch in einer Zeit in der sich am dichten Horizont bereits neue Währungssysteme abzeichnen. Die Basis dafür legte 2008 nicht überraschend eine der schwersten Vertrauenskrisen in das internationale Bankensystem, die die Neuzeit erlebete. Und umgesetzt werden die neuen Systeme mit Hilfe modernster Distributed-Ledger Blockchain Technologie. Das Neue mit seinem dezentralen Charakter fordert das Alte heraus. Während viele der neuen Währungen in der Kryptowelt, wie etwa der Bitcoin, großen Schwankungen unterworfen sind, versprechen Stablecoins eine Bindung und fixe Umtauschbarkeit an einen vorhandenen Wert, wie beispielsweise den US-Dollar oder auch Gold. Die alte Bretton-Woods-Herausforderung, dieses Versprechen auch jederzeit einhalten zu können, bleibt jedoch auch in der neuen Welt bestehen. Von der New Yorker Generalstaatsanwaltschaft verhängte Strafen in Millionenhöhe gegen den größten US-Dollar Stablecoin Tether wegen nicht lückenloser Nachweisbarkeit helfen dem Vertrauen wenig, besonders wenn weniger als 3 Prozent der Marktkapitalisierung auch wirklich in US-Dollar Cash hinterlegt ist. Es gilt wie immer bei neuem, Vertrauen aufzubauen. Sei es privatwirtschaftlich durch eventuell einen zu 100% mit Zentralbankgeld hinterlegten Stablecoin oder staatlich, mit durchdachten Central Bank Digital Currencies, wie dem von der Europäischen Zentralbank geplanten digitalen Euro.

Wir leben in einer Welt immer währenden schnellen Wandels und Vertrauen ist, wie Osterloh es beschreibt, „der Wille sich verletzlich zu zeigen“. Ohne Vertrauen gibt es keine Bündnisse, kein Miteinander, keinen Fortschritt.

Philippe Étienne war bereits nach ein paar Tagen zurück im herbstlichen Washington und arbeitet seither wieder daran wofür Diplomaten bestens ausgebildet sind – Vertrauen zu schaffen.

Es war ein großes Privileg zum sechsten Mal als Co-Autor an einem anerkannten und angesehenen Fachbuch mitwirken zu können.

Finanzdienstleister der nächsten Generation

Das Buch stellt den digitalen Transformationsprozess in der Finanzbranche vor und beschreibt verschiedene digitale Dienstleistungen und Business Cases. Etablierte Anbieter erörtern ihre digitale Strategie, arrivierte Fintechs schildern ihre Geschäftsmodelle und neue Start-ups präsentieren ihre innovativen Produkte und Dienstleistungen. Das Buch gibt somit einen profunden Überblick über den Status quo sowie über den weiteren Fortschritt der Digitalisierung in der Finanzindustrie.

Die Autoren stammen aus der Finanzdienstleistungsbranche, von Fintechs, aus Beratungsunternehmen und der Wissenschaft. Sie geben dem Buch eine hohe Aktualität und Praxisrelevanz. Das Buch richtet sich an diejenigen in der Branche, die sich mit der digitalen Strategie- und Produktentwicklung befassen und die die digitale Transformation der Finanzindustrie maßgeblich vorantreiben.

First published in German at LinkedIn Pulse on July 20, 2019. Please find article and sources in this link. Publication in English language pleas find below

On the role of cash in a modern society between technological progress and freedom

Fyodor Mikhailovich Dostoyevsky, one of the most important writers of the 19th century, impressively describes in his works the great existential and spiritual conflicts in which mankind was caught at the dawn of modernity. Not only his observations during the turbulent times of the upheaval of the Russian Empire in the 19th century, but also his personal experiences are an essential part of his work.

Fyodor Mikhailovich Dostoyevsky

At the age of 28 and at the beginning of a promising career as a writer, Dostoevsky was sentenced to four years in a Siberian prison camp. The reason for this was his participation in meetings of the Petraschwezen, an intellectual circle that spoke out against tsarist despotism and serfdom. In his novel, “The House of the Dead”, which also describes Dostoyevsky’s own experiences in Siberian captivity, he formulates the sentence that was later much quoted: “Money is coined liberty”. The sentence describes the vital relevance of the possibility of a free exchange of goods in an unfree environment – and this through coined cash money.

More than 150 years have passed since the first publication of the work. Europe needed to go through the age of Enlightenment, the experiences of two world wars and a long cold war to become a peaceful and very liberal place for its citizens. A place which is putting the dignity and freedom of the individual first.

The freedom in our payment options has also multiplied thanks to technological progress. It is part of our everydays life to pay the morning croissant at the bakery, the new monthly ticket for the subway or even the use of public toilets – even without cash. Technological progress, the smartphone revolution and also our user behaviour made this evolution in payments possible. “Digital payments” have become part of our progressive society. However, the aspect of not having money physically tangible sometimes entails interesting and also unwanted aspects.

Society in upheaval

Like Dostoevsky, we also live in a time of extreme social, economic and political upheaval. An age in which exponential technology developments, industries and business models are changing radically and countries competing for dominance in areas such as artificial intelligence. It is a time when transformation is the new normality and an agile corporate culture is the key to success. In these times, for many it became clear that, “Everything that can be digitized will be digitized.” And thus the question inevitably arises whether this also applies to the first “Instant Payment” solution humans invented, one of the earliest and most sustainable achievements of civilization – cash.

Germans love affair with cash

If we look at Germany, cash is still one of the most popular payment methods and – culturally speaking – will probably remain for quite some time to come. According to a survey by the Bundesbank, 88 percent of German citizens continue to regard cash as their preferred means of payment. This cultural imprint can certainly also be traced back to modern history and the personal experiences of the Germans with their money. Beginning with the traumatic experience of hyperinflation during the Great Depression of 1923 and the resulting deep-rooted German understanding of the importance of a central bank independent from politics.

A painful experience, which states even today – like Venezuela – live through again and again and whose causes are often identical. In Reinhard and Rogoff’s bestseller book “This time is different”, this phenomenon is brilliantly explained using an analysis of 800 years of international economic history.

The positive image of (cash) money in Germany was impressively advanced after the end of the 2nd World War. From the currency reform of 1948 and the beginning of the economic miracle with 40 D-Mark, which every German was allowed to hold physically in his hands, to the 100 D-Mark welcome money at the reunification in 1989. These personal experiences paired with a consistently brillant independent work by the German Bundesbank – which always gave the population the feeling of having a strong, stable and secure own currency – are all German experiences, which were literally “obvious” and shaped the cultural reference of the country and its citizens.

The current freedom of our payment options is certainly good, as long as we consumers are free to decide which means of payment we pay with. Discussions about a possible restriction of citizens’ freedom of choice, for example through the abolition of cash, regularly call on intellectuals to take a warning position. The poet Hans Magnus Enzensberger, for example, has the following opinion on the subject of “restriction”: “Those who abolish cash abolish freedom”. Also former Deutsche Bundesbank board member Carl-Ludwig Thiele said at a conference in 2015: “Abolishing cash would hurt consumer sovereignty — the free choice of citizens about their payment instruments“ and “Government agencies do not have the right to tell citizens how they should pay.”

Having “physical power of disposal” over money, i.e. holding the banknote in one’s hands, immediately establishes a much stronger relationship for the value of something than a number on a display. More than ten years ago, the US scientists Raghubir and Srivastava in their essay for the “Journal if Experimental Psychology: Applied” described that the degree of abstraction often poses a problem when it comes to means of payment. They found a correlation between the indebtedness of individuals and the use of credit cards.

In Germany, the trend towards digital payment became apparent for the first time last year. In this period consumers in the stationary retail sector spent more money on checking and credit cards than in cash, as the trade research institute EHI recently announced.

Source: Deutsche Bundesbank

However, this does not mean that customers will soon only pay by card or smartphone, the experts emphasized at the same time. Three-quarters of all retail purchases continue to be settled in cash. When it comes to the highly sensitive issue of “money”, many consumers continue to find it difficult to trust the comprehensive healing promises of an omnipresent digital world.

In order to ensure that cash and book money continue to be equally available, the players involved in the cash cycle, such as CIT companies like Prosegur, ATM operators like IC-Cash, banks like Bankhaus August Lenz et al., are working concentrated to make the provision of cash at all locations even more efficient and cost-effective. Both the providers of cash solutions and those of digital solutions experiment therefore with the latest blockchain and AI technologies to reach the before mentioned goals.

Technological vulnerability and fall-back option

Especially in extreme scenarios, such as catastrophes or other failures of a digital infrastructure due to cyberattacks, natural events or simply technical failure, it becomes clear how cash – by its very nature – proves to be actually the most robust payment method. Ultimately, it is not tied to electricity, digital infrastructures, passwords or other technical features – it is simply available. An interesting recent anecdote occurred in Sweden, which is one of the most advanced countries in cashless payment. A country where even the traditional church collection is now equipped with a card reader. At the Bråvalla music festival 2014, for example, the memory chips on the admission tickets went on strike. Thousands of thirsty fans sat on dry land and had to write out promissory notes for their drinks by hand. An experience that can be observed again and again when paying at the checkout, when the magnetic stripe of a card or simply the card reader does not work and the views of the people standing around in the queue are impatiently looking at the payer and trying to catch a glimpse of the name on the card of the supposedly non-solvent unlucky fellow.

Data Protection Best Practice

In an interview with Rheinische Post in February 2017, Klaus Müller, head of the Federal Association of Consumer Groups (Bundesverband der Verbraucherzentralen), said “Cash is data protection in practice”. He added: “Unbarred figures leave traces of data that can be used commercially to create a consumer profile. This data may be illegally “fished” by third parties.” Now Müller points to nothing new here and opponents of cash, use the argumentation to underline that the supposed anonymity of cash can be used for illegal business and transactions and that the suppression of cash stands above the protection of privacy. But since the first publication of the interview, the introduction of the EU General Data Protection Regulation (GDPR), the recently imposed $5 billion fine against Facebook for the Cambridge Analytica scandal and similar events, the sensitivity of the European population with regard to data protection and privacy has grown substantially.

Financial privacy

In the closing sentence of his speech at the Cash Symposium 2018 of the Deutsche Bundesbank, the former judge of the German Federal Constitutional Court, Prof. Dr. Udo Di Fabio, underlined the probably most important point in the current discussion about cash. He said that in principle it is “not to be underestimated” that every citizen has the souvereignity of the free disposal of his money – of his personal “exchangeable assets”. He further added that this is particularly true when “financial privacy” is considered legally imperative. In other words, a society whose entire assets would be managed in digital form only, could also exercise only limited individual control over its money and would have to ask itself, “whether the state would be entitled via its central bank to carry out a controlled devaluation through negative interest rates, accounting discounts or fees on credit balances”. Prof. Di Fabio further points out that this would then not only be a property encroachment, but as a result possibly also the imposition of a special levy, which is permitted in the German legal system only under narrow conditions.

For young Fjodor Mikhailovich Dostoyevsky the conversion to book money in the Siberian prison would have meant the withdrawal of his individual sovereignity over money, so that he would not have had any more the fortune of using cash for the exchange of goods and other things. He describes the quintessence of this situation as follows: The suffering of prisoners who don’t have money is 10 times greater.

Thus, it is reasonable to assume that the intellectual serious discussions about cash and civil liberty rights would delight Dostoyevsky, with his experiences in an unfree society.

Our open and liberal society is characterised by the fact that we have and continue the discussion about “Coined Liberty 2.0” at this level.

Artificial intelligence is finding its way into the highly regulated world of banking. And not only GAFA Silicon Valley high-tech companies see it as the technology of the future, but also FinTechs and established banks. How it came to this, what possibilities and limits there are at the moment and why humans will remain irreplaceable not only when it comes to money – the commentary

by Jochen Werne, innovation and transformation expert Munich private bank Bankhaus August Lenz

Original published in German in the IT-Finanzmagazin (31 July 2018). Translation by DeepL

After “FinTech”, “Blockchain” and “Crypto”, “AI” is the new buzzword in the banking world. Whether chatbots in the digital customer center or self-learning algorithms for highly complex investment strategies are being discussed – the omnipresence of the term suggests that the integration of artificial intelligence into one’s own business model seems to be virtually vital.

Artificial intelligence and big data are currently the strongest and most vibrant innovation trends in the financial sector …

… was also one of the guiding principles of Prof. Joachim Wuermeling, board member of the Deutsche Bundesbank, in his speech on “Artificial Intelligence” at the second annual FinTech and Digital Innovation Conference in February 2018 in Brussels.

The choice of the conference venue, which like rarely any other city combines both a belief in progress and a deeply rooted European tradition, can hardly be more symbolic of the forthcoming change. In fact, the topic is by no means new: the development towards an increased use of so-called non-human intelligence is based on approaches from the 1940s – with the invention of the first computers

Artificial intelligence: revolution as a reaction to mountains of data?

But what is now possible in times of exponential technologies is in fact nothing less than a revolution. The financial industry is sitting on a valuable mountain of data, the extent of which is currently difficult to estimate. The maturing AI systems would not only make the preparation and processing of this data easier, but also much more cost-effective, faster and more targeted. Data already collected could become the most valuable raw material and a resource due to the technological leaps in the field of AI, which, in combination with the enrichment of external, non-structured data, must be “usable” in a meaningful way.

The industry is asked to use private data in a sensitive way for the benefit of the customer, – a goal that should certainly apply to all AI-based approaches.

To find meaningful regulations for the handling and the effects of the use of AI on society, economy and thus on our life and the work of tomorrow is the task of politics. The fact that this topic is taken very seriously is evident not only in national initiatives such as the German Platform for Artificial Intelligence “Learning Systems”, but also in the European Artifical Intelligence shoulder-to-shoulder approach, which is being pushed forward by France and Germany.

“Digital hand holding” in the event of a financial crash is not enough

At present, it is still too early to say which operational areas of the financial world will sooner or later be supported – in part or even entirely – by the use of AI systems. However, the financial crises of the past have shown this time and again:

Trust is crucial when it comes to money. Trust in the markets, the banking system and the human contact as an intermediary in a complex issue”.

However, the banking industry knows very well from its own experience how easy it is to loose customer’s trust. An experience that Mark Zuckerberg and Facebook recently also had to make in connection with the Cambridge-Analytica scandal. As with every new technology and every new approach, the same applies to the topic of “intelligent” systems: a lot of trust, coupled with half-knowledge and a big dash of emotionality results in a popular trend cocktail, which, however, bears a certain risk of headaches on the following day.

Jochen Werne

Jochen Werne is the authorized signatory responsible for Marketing, Business Development, Product Management, Treasury and Payment Services at Bankhaus August Lenz & Co. After two years as navigator of the sailing training ship ‘Gorch Fock’, the international marketing and banking specialist completed his studies as client coverage analyst at Bankers Trust Alex. Brown International and in Global Investment Banking at Deutsche Bank AG, he has worked on numerous projects in other European and American countries. In 2001, he joined Accenture as a Customer Relationship Management Expert in the Financial Services Division before joining Bankhaus August Lenz & Co. AG in Munich, where he has since been responsible for various areas of the institute. As part of the Innovation Leadership Team of the Mediolanum Banking Group, a member of the expert council of Management Circle and the IBM Banking Innovation Council, Jochen Werne is a keynote speaker at numerous banking and innovation conferences.