Published on 11 January 2023 at Springer Professional – Follow this LINK to original text in German. Translation created with deepL.com

Experts quoted in the article: Stefan Behringer, Leef H. Dierks, Florian Follert, Jochen Werne, Dr. Johannes Winter, Joachim Wurmeling

What distinguishes so-called stablecoins from cryptocurrencies like Bitcoin, Ether & Co? By linking to one or more currencies, this form of digital money forms a bridge to classic FIAT currencies. How this works and where problems lurk is shown in our “Compact explained”.

Stablecoins are digital tokens, assets of private issuers that can also take on money functions. According to Leef H. Dierks, they usually replicate the value of a reserve currency, such as the US dollar, or even a whole bundle of official currencies.

Thus, they do not have to represent a claim on the issuer (the reserve currency) itself, but can also be backed by demand deposits of various currencies, securities or other assets. This so-called peg reduces the volatility of stablecoins compared to classic virtual currencies, such as Bitcoin,” writes the Springer author in the book chapter “Virtual Currencies and Monetary Policy” on page 234.

According to Dierks, stablecoins take on a bridging function to fiat currencies, “especially since, as long as they are backed by legal tender, they do not challenge the currency monopoly of central banks (analogous to bank deposits) at any time”.

Stablecoins make new business models possible

According to a thesis paper by the Landesbank Baden-Württemberg (LBBW) from mid-December 2022, stablecoins do open up new business models. At the same time, however, they are “anything but stable, but are subject to the risk of the holders fleeing from them if there are doubts about their collateralisation”. Digital money may have a negative impact on macroeconomic lending and reduce the influence of central banks on the aggregate money supply. One way to regulate it is to require issuers to hold central bank reserves.

The best-known stablecoin project is Tether, which is pegged one-to-one to the US dollar. “There has been repeated criticism of Tether, so that the company behind the issue has since admitted to using not only currency holdings in US dollars to collateralise the issued units of cryptocurrencies, but also other assets (for example, commercial papers of companies),” Stefan Behringer and Florian Follert describe the background in the book chapter “Controlling of cryptocurrencies” (page 187). This also explains why this stablecoin does not correlate exactly with the performance of the US dollar.

Risks of stablecoins

Jochen Werne and Johannes Winter explain in the book chapter “Cash, book money, cryptocurrencies and the digital euro” on page 84 that there are risks for the financial sector if stablecoins become widespread. They could undermine the banks’ deposit business and their business models. The Springer authors see in the central bank cash-backed stablecoins a possibility of a trustworthy transitional solution in hybrid form. This is a stablecoin that demonstrably holds any digital twin in the form of central bank money.

“Due to the tradability of the tokens, the flexibility of book money is paired with the guarantee of physical central bank money. Even the expected damage from a successful attack on the underlying blockchain could thus be minimised, since an unlawful acquisition of power of disposal over assets is quickly restricted in its usability. A regulated expert function guarantees that only central bank money or a digital twin is traded and thus the central supervisory function always lies with the central bank,” say Werne and Winter.

MiCA forms future legal framework

With the Markets in Crypto Assets (MiCA) regulation, the European Union has sewn a legal garment for the crypto industry in the 26 EU states. The new EU regulation is to enter into force by the beginning of 2023 and become effective 18 months later vis-à-vis all market participants.

“MiCA responds to the growth of the cryptoasset ecosystem and integrates a large number of new players into the European supervisory space,” explains Joachim Wurmeling, member of the Executive Board of the Deutsche Bundesbank, in a guest article on the occasion of the Bundesbank Symposium in November 2022. “In future, crypto service providers and issuers of crypto assets will not only have to ensure that the risks arising from the cryptoasset business are adequately managed; they will also have to apply for authorisation to issue crypto assets or to provide crypto services and be subject to ongoing supervision.”

In addition, he said, the regulation also applies to traditional financial institutions that provide services around cryptoassets. The regulatory approach for MiCA is new and is emerging alongside the traditional structure.

In their historical-social debate “Cash, book money, cryptocurrencies and the digital euro“ on money in the digital age in the book “Praxisbeispiele der Digitalisierung” (Practical Examples of Digitalisation) published by Springer Gabler Verlag, the co-authors Jochen Werne and Johannes Winter use historical examples to show the interconnectedness of various actors in the cycle of our money today.

Read an excerpt of chapter 9.3.1. on the historical role of CIT – cash in transit here:

Making money available and the central role of cash-in-transit logistics

In the case of cash, the person concerned has direct, unrestricted physical power of disposal over his money in the form of coins or banknotes. However, the fact that this is not yet given when the money is minted or printed in bank vaults, but only when it is delivered to the owner, is of crucial importance. To illustrate the importance of this step and thus also the role of the transport of money and valuables, a historical event from the Rotschild Archives can be used.

„The Rothschilds supplied the Duke of Wellington with gold during the Napoleonic Wars and saved Wellington’s armies from almost certain defeat. Between 1793 and 1815, Britain was almost continuously at war with France, which placed an enormous burden on the British treasury. By 1813, Wellington’s armies had managed to push the French back as far as the Pyrenees, but the financial situation had become critical. Wellington desperately needed gold and silver coins that he could exchange locally to pay and feed his troops and thus maintain morale. J.C. Herries, the British government’s chief commissioner, was responsible for financing and equipping the British armies in the field. Herries was looking for a middleman who could secretly procure large quantities of gold without alerting the French. In January 1814 he officially engaged Nathan Mayer Rothschild. Over the previous five years Nathan had built up an extensive network of couriers, dealers, brokers and bankers to facilitate his gold trading activities. Over time, he had established a dominant position as a gold broker in the City of London. After receiving the commission from Herries, Nathan instructed his brothers on the Continent to buy gold wherever they could, secretly and in small quantities so as not to disturb the market. Once the gold was gathered, it was shipped and forwarded to Wellington in the south of France so that he could pay his troops” (Rothschild Archives 2021).

Alongside many small and medium-sized players, the three corporations Prosegur, Brinks and Loomis dominate the main part of the consolidating world market for cash and cash-in-transit. By supplying retailers, banks and private individuals via ATMs and branches, as well as repatriating funds, the industry ensures that the cash cycle is maintained and that each individual’s power of disposal over cash is upheld.

It was a pleasure contributing in co-authorship with the AI-expert and friend Dr. Johannes Winter / Jochen Werne to this new Springer Gabler publication ”Praxisbeispiele der Digitalisierung” (Best Practice of Digitilisation) which is available now as e-book and paperback at https://link.springer.com/book/10.1007/978-3-658-37903-2

Cash, Book Money, Crypto Currencies and the Digital Euro

The aim of the chapter in the book is a contribution to the debate of money in the digital age. It combines historical insights into the meaning of money with the latest technological developments, to compare visions of the financial industry with realities and to develop options for action to shape the digital transformation of money.

Abstract: In a world where tech companies are leading campaigns to create a new cryptocurrency and bitcoin is surpassing the US$50,000 mark because a visionary electric car maker wants to recognise the cryptocurrency as a means of payment, some fundamental questions arise: how must money be defined in a digital world to reliably fulfil the characteristics of a universally recognised store of value and medium of exchange? And what changes are in store for the financial industry when so-called stablecoins proliferate and challenge the banks’ classic deposit business and their outdated business models? The aim of this contribution to the debate is to combine historical insights into the meaning of money with the latest technological developments in the digital age, to compare visions of the financial industry with realities and to develop options for action for shaping the digital transformation of money.

Thomas Apitzsch, Michael Pfleger, Frederike HaberlandPages 309-325

About Springer Gabler

Springer Gabler Verlag is the leading specialist publisher for the business sector. Its classic and digital teaching materials and specialist media address current business questions and provide reliable, practical solutions.

A plea for trust in a time of mistrust. Trust is the foundation on which monetary systems are built. Trust forms the basis of international diplomatic relations and is the foundation for all progress.

But what happens once trust is shaken?

The diplomatic dispute over a multibillion-dollar submarine treaty – which took place three months before the Russian – Ukrainian war, concerns about a new cold war, and the collapse of the Bretton Woods system exactly 50 years ago are the manuscript for this maritime-themed French-American story about money and trust. It is an object lesson for our times, where we are witnessing the emergence of crypto-financial markets and thus stand on the threshold of a new form of money.

TIME OF MISTRUST

by Jochen Werne

After the traditional long summer vacation, France awakens in September from its brief self-created slumber, as it does every year. Life begins to take its usual course, even if some are still reminiscing, perhaps enjoying the first harbingers of post-Covid worry-free life. Not so Philippe Étienne. For him, on the other side of the Atlantic, in Washington, which is actually picturesque at this time of year, autumn begins with a diplomatic thunderstorm. A storm that must have been new even for the 65-year-old gray-haired eloquent ambassador of France. 6160 kilometers away, at the Élysée Palace, Président de la République Emmanuel Macron decides to call his top diplomat in the United States, along with his Australian counterpart Jean-Pierre Thebault, to Paris for consultations. The unprecedented act in Franco-American history is justified by Foreign Minister Jean-Yves Le Drian with the “exceptional gravity” of an Australian-British-American announcement, and impressively underlined with the words “lie,” “duplicity,” “disrespect” and “serious crisis.”

At the heart of this crisis is the surprise announcement by the aforementioned countries to enter into a strategic trilateral security alliance (AUKUS) with immediate effect. An alliance that also provides for the procurement of nuclear-powered submarines for Australia, effectively putting to rest a 56-billion-euro French-Australian submarine order already initiated in 2016. The conclusion of the agreement comes at a time when U.S. President Joe Biden has asserted to the UN General Assembly, “We do not seek – I repeat, we do not seek – a new cold war or a world divided into rigid blocs.” However, experts, such as renowned historian Niall Ferguson, have been talking about this so-called “new cold war” between the U.S. and China since 2019, and it is not about nuclear arms races, but rather about technology supremacy in cyber security, artificial intelligence and quantum computing. Even though nuclear-powered submarines are at the center of the diplomatic dispute, one is quick to note in the AUKUS agreement that cooperation in the aforementioned fields is one of the most important components of the treaty. An objective that is perhaps also congruent with French interests. But the dispute between the old friends is less about the “what” than about the diplomatic “how” – that is, about the breach of trust that is triggered when close allies are simply presented with a fait accompli. Facts that also affect them financially and personally.

Because money and trust are closely interwoven. The trust of a bank that the creditor will repay its debts. A citizen’s trust that the currency in which he or she is paid their salaries is stable. A state’s trust in a currency system that the agreements made there will be honored by all. Georg Simmel, in his “Philosophy of Money,” sums it up this way: “Money is perhaps the most concentrated and pointed form and expression of trust in the social-state order.”

Last year marked the 50th anniversary of another French-American trust-busting melodrama with a maritime backdrop. Benn Steil, senior fellow at the Council on Foreign Relations, describes the moving events of August 6, 1971, in his book, The Battle of Bretton Woods, as follows: “…a congressional subcommittee issued a report entitled ‘Action Now to Strengthen the U.S. Dollar` that concluded, paradoxically, that the dollar needed to be weakened. Dollar dumping accelerated and France sent a warship to pick up French gold from the vaults of the New York Fed.”

At first glance, this dramatic gesture by then French President Georges Pompidou in the final act of the collapse of the Bretton Woods system seems as strange as the withdrawal of ambassadors today. The basis, however, is similar and lay then as now in an equally shaken trust between the great nations that were nevertheless so closely intertwined. Without going deeper into the new monetary order created after World War II, with the U.S. dollar as the anchor currency, it is important to understand the reason for the French revolt evident in the “White Plan.” The plan provided that the U.S. guaranteed the Bretton Woods participating countries the right to buy and sell gold indefinitely at the fixed rate of $35 per ounce. The dilemma of this arrangement became apparent early on. For by the end of the 1950s, dollar holdings at foreign central banks already exceeded U.S. gold reserves. When French President Charles de Gaulle asked the U.S. to exchange French dollar reserves for gold in 1966, the FED’s gold reserves were only enough for about half that amount. The ever more deeply anchored loss of confidence forced the American president Richard Nixon on August 15, 1971 to cancel the nominal gold peg and the so-called “Nixon shock” ended the system as it was.

And where something ends something new can or will inevitably begin.

Today we live in a world where the stability of our currency is based on our confidence in government fiscal policy, the economic strength of our country, and the good work of an independent central bank. However, we also live in a time when new currency systems are already looming on the dense horizon. The basis for this was laid in 2008, not surprisingly, by one of the most serious crises of confidence in the international banking system that modern times have seen. And the new systems are being implemented with the help of cutting-edge distributed ledger blockchain technology. The new, with its decentralized nature, is challenging the old. While many of the new currencies in the crypto world, such as bitcoin, are subject to large fluctuations, stablecoins promise a link and fixed exchangeability to an existing value, such as the US dollar or even gold. However, the old Bretton Woods challenge of being able to keep this promise at all times remains in the new world. Millions of dollars in penalties imposed by the New York Attorney General’s Office on the largest U.S. dollar stablecoin, Tether, for not being fully verifiable do little to help trust, especially when less than 3 percent of the market capitalization is actually deposited in U.S. dollar cash. As always with new ones, trust has to be built up. This can be done privately, perhaps with a stablecoin backed 100% by central bank money, or by the state, with well thought-out central bank digital currencies, such as the digital euro planned by the European Central Bank.

We live in a world of perpetual rapid change and trust is, as Osterloh describes it, “the will to be vulnerable.” Without trust, there are no alliances, no togetherness, no progress.

Philippe Étienne was back in autumnal Washington after just a few days and has since been working again on what diplomats are best trained for – building trust.

Sources

Billon-Gallan, A., Kundnani, H. (2021): The UK must cooperate with France in the Indo-Pacific. A Chatham House expert comment. https://www.chathamhouse.org/2021/09/uk-must-cooperate-france-indo-pacific (Retrieved 24.9.2021)

Brien, J. (2021): “Stablecoin without stability”: Tether and Bitfinex pay $18.5 million fine. URL: https://t3n.de/news/stablecoin-tether-bitfinex-strafe-1358197/?utm_source=rss&utm_medium=feed&utm_campaign=news (Retrieved: 9/30/2021).

Corbet, S. (2021): France recalls ambassadors to U.S., Australia over submarine deal. URL: https://www.pressherald.com/2021/09/17/france-recalls-ambassadors-to-u-s-australia-over-submarine-deal/ (Retrieved 9/25/2021).

Ferguson N. (2019): The New Cold War? It’s With China. And It Has Already Begun. URL: https://www.nytimes.com/2019/12/02/opinion/china-cold-war.html (Retrieved: 9/30/2021).

Graetz, M., Briffault, O. (2016): A “Barbarous Relic”: The French, Gold , and the Demise of Bretton Woods. URL: https://scholarship.law.columbia.edu/cgi/viewcontent.cgi?article=3545&context=faculty_scholarship p. 17 (Retrieved 9/25/2021).

Osterloh, M., Weibel, A. (2006): Investing trust. Processes of trust development in organizations, Gabler: Wiesbaden.

Steil, B. (2020): The Battle of Bretton Woods: John Maynard Keynes, Harry Dexter White, and the new world, p. 377.

Stolze, D. (1966): Does de Gaulle defeat the dollar? In ZEIT No. 36/1966. URL: (https://www.zeit.de/1966/36/besiegt-de-gaulle-den-dollar/komplettansicht (Retrieved: 9/26/2021)

The Guardian Editorial (2021): The Guardian view on Biden’s UN speech: cooperation not competition URL: https://www.theguardian.com/commentisfree/2021/sep/22/the-guardian-view-on-bidens-un-speech-cooperation-not-competition(Retrieved: 9/29/2021)

Unal, B., Brown, K., Lewis, P., Jie, Y. (2021): Is the AUKUS alliance meaningful or merely a provocation – A Chatham House expert comment. URL: https://www.chathamhouse.org/2021/09/aukus-alliance-meaningful-or-merely-provocation (Retrieved: 9/24/2021).

Time Online (2021): France sees relationship in NATO strained. URL: https://www.zeit.de/politik/ausland/2021-09/u-boot-deal-frankreich-australien-usa-streit-nato-jean-yves-le-drian?utm_referrer=https%3A%2F%2Fmeine.zeit.de%2F (Retrieved: 9/25/2021)

SECURITY BRIEFING. The battlefields of the past as a lesson for the protection of crypto assets today.

COLD HISTORY. HOT REALITY is a contribution to The Yearbook 2022 “Treasury and Private Banking”, edited by Roland Eller. The book is a well-known platform for building the bridge from the traditional to the new decentralised financial world.

COLD HISTORY. HOT REALITY by Jochen Werne is a plea for openness to new technologies, embedded in a historical-social security briefing on money, power and the indispensable need to protect assets. The battlefields of the past provide the framework for lessons on protecting crypto assets in our technology-dominated world and help us gain a basic understanding of the opportunities and threats in our new cyber reality.

COLD HISTORY – HOT REALITY was particularly inspired by conversations and articles from the following thought leaders, to whom I am deeply indebted.

Raimundo Castilla – CEO Prosegur Custodia Digitales, Ghislain D’Hoop – Ambassador of Belgium to Austria, Slovakia, Slovenia and Bosnia and Herzegovina, Permanent Representative to the United Nations, Roland Eller – Founder and CEO of Roland Eller Consulting, Niall Ferguson – Milbank Family Senior Fellow at the Hoover Institution at Stanford University, Christoph Impekoven – Co-Founder micobo GmbH, Benon Janos – CFO flatexDEGIRO Bank AG, Lior Lamesh – Founder & CEO of GK8, Bernd Lehmann – Historian, Commander of the German Navy (ret.), Rakesh Sharma – Author, Thomas Vartanian – Author and Counselor, Heath White – CEO Prosegur Germany, Johannes Winter – Managing Director of the Platform „Learning Systems“ – Germany‘s AI-platform

Preview and excerpt from Chapter I of “COLD HISTORY – HOT REALITY”

WHAT IS PAST IS PROLOGUE

Impressive and powerful, the words “What is past is prologue” are chiselled in white marble at the foot of the statue in front of the National Archives in Washington D.C.. The famous quote from William Shakespeare’s “The Tempest” is a haunting reminder to everyone that history provides the context for the present.

We live in a present that is changing at breathtaking speed. This fact concerns us daily, but if we do not take the time for a little history lesson, we are doomed to painfully repeat the mistakes of the past. More than aware of this realisation is the former CEO of tech giant Alphabet, Google’s parent company. He dedicated the following note to the New York Times bestseller, “The Square and the Tower: Networks and Power, from the Freemasons to Facebook”: “Niall Ferguson … brilliantly illuminates the great power struggle between networks and hierarchies that rages around the world today. As a software engineer familiar with the theory and practice of networks, I was deeply impressed by the insights of this book. Silicon Valley needed a history lesson and Ferguson delivered.” Not only is Eric Schmidt impressed, but many of the thoughts in this article are inspired by Niall Ferguson’s illuminating papers and lectures.

The beauty of the past is that everything that has already happened, successes and failures, can always be explained in detail and serve as lessons for future challenges. Successful leaders use this knowledge to develop solutions to the problems of the future and to develop communication strategies to make their visions understood by others.

This article was written at a time when humanity is in the final stages of a global pandemic that is saddling countries with an unprecedented debt burden. At the same time, a “New Cold War” is emerging and an arms race for technological supremacy has begun. With new possibilities, the old equilibrium is shaken and a new, albeit familiar, competition for power and money begins. All this at a time when crypto-blockchain-based monetary systems are rapidly becoming a new reality.

The article, with its historical analogies, aims to give the reader a better understanding of how money, power and security are closely intertwined. This helps to put quite complex issues into perspective and gives a clear view of the dangers and opportunities of our changing reality.

The world and change are not to be feared, but understood.

Jochen Werne

The new YEARBOOK will be available in Spring 2022. Find out more HERE

The aim of this contribution to the debate is to combine historical insights into the meaning of money with the latest technological developments in the digital age, to compare visions with realities and to develop options for action for shaping the digital transformation of money.

The 10 most successful bank robberies in human history, in which the equivalent of US$1.62 billion was taken at sometimes massive expense, seem like the work of amateurs compared to the US$3.78 billion taken by cybercriminals in 2020 alone. In a world where tech companies are spearheading campaigns to create a new cryptocurrency and bitcoin is surpassing the US$50,000 mark because a visionary electric car maker wants to recognise the cryptocurrency as a means of payment, some fundamental questions arise: How must money be defined in a digital world to reliably fulfil the characteristics of a universally recognised store of value and medium of exchange? And what changes will result if so-called stablecoins challenge the banks’ classic deposit business and their traditional business models?

SAVE THE DATE: 29 September 2021 – 11.30 a.m. Berlin Time

It‘s a great pleasure giving a keynote at the VÖB-Service GmbH #VSK2021 Conference and to discuss with financial industry experts fundamental questions about the FUTURE OF MONEY

The ten most successful bank robberies in human history, in which the equivalent of US$1.62 billion was captured at great expense, seem almost like the work of amateurs compared to the US$3.78 billion captured by cybercriminals in 2020 alone. In a world where tech companies are spearheading campaigns to create a new #cryptocurrency, where bitcoin is surpassing the US$50,000 mark because a visionary electric car maker wants to recognise cryptocurrency as a means of payment, Jochen Werne, Member of the Executive Board Prosegur Germany, asks some fundamental questions. “How must money be defined in a digital world in order to fulfil the characteristics of a generally recognised and reliable store of value and medium of exchange?” Or also: “What changes are coming to the financial industry when #Stablecoins spread and challenge the classic deposit business of banks?”

In our stream Digitalisation at #VSK2021, Jochen Werne presents possible answers to these and other questions.

Be there and register today for the #Kreditwirtschaft congress on Wednesday, 29 September! ? https://lnkd.in/gMe2g59

Reflections by Jochen Werne, Chief Development & Chief Visionary Officer Prosegur Germany (published in Prosegur Express 02/2021)

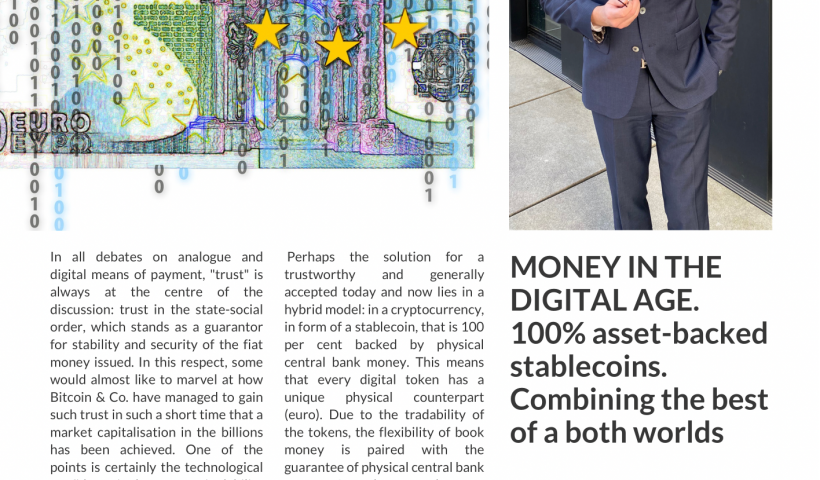

In all debates on analogue and digital means of payment, “trust” is always at the centre of the discussion: trust in the state-social order, which stands as a guarantor for stability and security of the fiat money issued. In this respect, some would almost like to marvel at how Bitcoin & Co. have managed to gain such trust in such a short time that a market capitalisation in the billions has been achieved. One of the points is certainly the technological confidence in the non-manipulability of the blockchain. But is the blockchain really not manipulable, or is it rather a question of time before an attack will succeed? And what conclusions are central banks around the world drawing from this as they look at creating central bank digital currencies? Currencies designed to bridge the gap between the stability of analogue central bank money and the demands of our digital age.

Perhaps the solution for a trustworthy and generally accepted today and now lies in a hybrid model: in a cryptocurrency, in form of a stablecoin, that is 100 per cent backed by physical central bank money. This means that every digital token has a unique physical counterpart (euro). Due to the tradability of the tokens, the flexibility of book money is paired with the guarantee of physical central bank money. Last but not least, a regulated trustee function guarantees that the existing and securely stored central bank money is always paired with its digital twin. Thus. the best of both worlds is firmly united.

by JOCHEN WERNE published in DER BANK BLOG (30 October 2020) – For the original version in German please follow this LINK – English version translated by Deepl.com

“Disposal power” or “authority to dispose” are legal terms which are of great importance in the discussions on cash and book money. It also concerns the freedom of choice of citizens. The German language today is much more extensive than the 100,000 words used by Goethe in his time. We hardly use many of these words, which are so characteristic of our language, despite their meaning. Perhaps some readers feel the same way about the word “Verfügungsmacht” as I did when I consciously read it for the first time in a quotation from the former president of the Federal Constitutional Court, Prof. Dr. Udo Di Fabio. And perhaps it is like with many things in life that one only realises the deeper meaning at the moment when one deals with it in more detail. In our modern times, hardly anyone will visit the university library to quickly get to grips with a topic. Instead, people google the library to get an overview. And while less than 20 years ago we would have found our first little research happiness about the term “power of disposal” or also “authority to dispose of property” in the library of the law faculty, Internet research reveals in seconds a glance at a litany of legal forums.

Definition of power of disposal What is striking here is that the focus is not on the definition of control, but that the topic of regaining control dominates the first page on Google. Inevitably, this reminds me of my first visit to the Munich Google office many years ago. Almost rapturously in his remarks about the power of the algorithm, a sales employee of the world’s most powerful search engine asked the group if we knew where on the Internet they hid a body. With a glance into his head-shaking auditorium, he solved the riddle with a smile and said: “On the second page of Google search. Inevitably, of course, one then asks oneself – albeit only rhetorically – whether the Google business model works in particular because many have simply relinquished control over their data. The power of disposal or also power of disposition is defined as the “legal power to dispose of an object”. Which is banal, meaning that I should also have the power of disposal over what belongs to me – in other words, what is legally my property. However, the success of my own research on the first Google page suggests one thing above all else to the reader: that the power to dispose of property can be lost. For example, also of your own money? In order to answer this question, one should basically distinguish between cash and book money.

Cash, book money and the power of disposal With cash, I have direct unlimited physical control over my money in the form of coins or notes. This power of disposal can of course be lost if I am robbed or simply lose my wallet. Without entering into the legal depths of “normal” debt and the right to dispose of money, citizens have in principle all the means guaranteed by the state at their disposal to recover their property. The same applies to book money, if, for example, money is lost through credit card fraud when shopping online. The limits of non-physical power of disposal would, however, quickly become apparent if a bank went bankrupt and the money parked in the account in excess of the deposit guarantee was no longer available. Cash, book money and free availability It is utopian and not at all sensible to hoard all one’s “money” as cash. But it is certainly important to make clear what it means to no longer have the freedom of choice between cash and book money and thus to completely give up one’s right to physical availability of money. In the concluding sentence of his speech at the 2018 Cash Symposium of the Deutsche Bundesbank, Udo Di Fabio underlined what is probably the most important point in the current discussion surrounding this election. He said that it should not be “disregarded” in principle that every citizen should be able to freely dispose of his money – his “exchangeable assets”. He further added that this was particularly true when “financial privacy” was considered a legal requirement. This means that a society whose entire assets would only be managed digitally in book money could also only exercise limited individual power of disposal over its money and would have to face the question “whether the state, through its central bank, would be entitled to carry out a controlled devaluation through negative interest rates, booking discounts or fees on credit balances”. Prof. Di Fabio further points out that this would then not only be an encroachment on ownership but, as a result, possibly also the imposition of a special levy, which is only permitted under strict conditions in the German legal system.

Conflicts of interest and trust It is easy to see that this issue can give rise to considerable conflicts of interest in the triangular relationship between citizens (- how can I protect and increase my money), government (- how can public debt be reduced) and central bank (- how can economic and monetary stability be ensured). This is particularly true in the light of the continuing challenges posed by the Corona pandemic. It is thanks to the excellent work of the Deutsche Bundesbank since the Federal Republic of Germany came into existence and the confidence it has built up in our currency that the confidence of the public in both cash and book money is so high in this country. Freedom of choice between cash and book money Of course, another decisive aspect of this trust is the freedom of choice between cash and book money, which the Bundesbank also advocates. This freedom of choice also offers banks the opportunity to deal flexibly with the funds. For example, instead of charging 100 percent negative interest on book money to citizens or companies, banks could also physically hold it or have it held in safekeeping as cash. Since it is not part of a bank’s core competence to operate high-security systems and one certainly does not want to expose one’s own employees to the risk of a robbery or the blackmailing abduction of a family member, there is of course the possibility of outsourcing such a service in a LCR-compatible and MaRisk-compliant manner. A service that supports the customer in parts of his liquidity management and does not make it difficult for him to possibly maintain his own safe in his own four walls and without a security concept and thus endanger himself and his family. “Money is coined freedom” In his prose work “Records from a House of the Dead”, the Russian writer Fyodor Mikhailovich Dostoevsky describes his own experiences in Siberian captivity and formulates the later much quoted sentence: “Money is coined freedom”, thereby describing the vital relevance of a free exchange of goods in an unfree environment – and this through coined cash money. For the young Dostoyevsky, the changeover to a pure book money system in Siberian prison would have meant the withdrawal of his individual power of disposal over money, so that in reverse he would no longer have any assets which he could have used for the exchange of goods and other things. He describes this situation in the quintessence as follows: The suffering of prisoners who do not have money is “10 times greater”. It is therefore reasonable to assume that the intellectual, serious discussions about the freedom of choice between cash and book money and the freedom of citizens in a constitutional state, which is freely consolidated in its constitution, would please Dostoevsky with his experiences in an unfree society. And it is characteristic of our open society that, especially in a crisis like the present one, we are conducting and continuing the debate on freedom of choice and power of disposal at this level, and not only with regard to our money.

Does cash have a future? An article by Dunja Koelwel, editor in chief of gi Geldinstitute | 20.10.2020 – 13:02

Please follow this LINK for the original source in German. Translation made by DeepL.com

Cashless payment is on the advance worldwide, only the Germans hang on to cash. gi Geldinstitute therefore wanted to know from Ralf-Christoph Arnoldt (Bundesverband der Deutschen Volksbanken und Raiffeisenbanken BVR), Jochen Werne (Prosegur Germany), Dr. Harald Olschok (BDSW) and Leif Wienecke (Solarisbank) Does cash still have a future?

Signs such as “Cash only” should be a thing of the past in Germany, according to the digital association Bitkom. Wherever customers can pay, at least one digital payment option that can be used throughout Europe should be offered on a mandatory basis, according to the “Bitkom theses on freedom of choice in payment”.

“Cash shows itself to be an anchor of trust in uncertain times. With increasing concern about the corona virus, the amount of physical cash in circulation in the USA, for example, has risen,” says Jochen Werne, member of the management of Prosegur Cash Services Germany. gi geldinstitute therefore asked: What is the current situation regarding ‘war on cash’?

Since the Corona crisis, more and more people have been paying with cards or smartphones instead of with coins or notes. Is this a trend that is slowly eliminating cash? What is your perception?

Ralf-Christoph Arnoldt: Indeed, in recent months we have seen gains in card payments, especially in payments with Girocard. In the first half of 2020, transaction figures have increased by 20.7 percent compared to the same period last year. However, cash still plays an important role in everyday life in Germany, even if this love is eroding.

According to the Eurohandelsinstitut (EHI), the share of cash in turnover in 2019 was still 45.5 percent. Cash offers some advantages from the customer’s point of view. Paying with cash is convenient for the customer, anonymous, immediately final. Cash is freedom for customers. Regulators and business circles involved in the cash circle should accept this as a fact and not force them to change it.

Dr. Harald Olschok: Without doubt, a new phase of “war on cash” began during the Corona crisis. 75 percent of the member companies of the BDGW expect sales next year to be up to 20 percent lower than in the past. We assume that the proportion of cash payments in the retail sector will fall from around 48 percent at the beginning of 2020 to well below 40 percent. However, the crisis has also shown that Germans continue to have great confidence in cash as a secure means of payment and store of value. According to a survey by YouGov, Germans also cannot imagine living in a cashless society.

Leif Wienecke: Since the Corona crisis, we have seen an acceleration of many trend developments, some of which were already foreseeable before. This also includes contactless payment. This customer behaviour, which is relatively new in Germany, fits in well with corona-related hygiene measures. Basically, it can be said that, in addition to hygiene considerations, end customers are primarily looking for speed when choosing a means of payment. This is where digital and contactless payment methods come into play. Over the next few years, we will see a further decline in cash payments and an increasing use of digital payment methods such as mobile wallets.

Jochen Werne: What is important to people when it comes to their money – the “fruits of their labour”? Certainly its unlimited availability. If they can have confidence that they can get their money at any time, people choose the payment option that is most convenient for each individual. Some prefer to pay by smartphone, while for others it’s “only cash is true”. It is fundamental that we as consumers are free to decide from which means of payment we can freely choose. Freedom of choice is the key word.

A “per cash” argument often made is that technology is vulnerable and that in a crisis the value of security is always the highest good. This is why many people have been hoarding cash at the beginning of the lockdown. Do you believe that this money will now come back into circulation? And what do you think about the technological error potential of digital payment options?

Ralf-Christoph Arnoldt: The fact that cash was hoarded at the beginning of the lockdown was more due to the fact that people thought the cash supply could be endangered because of the Corona crisis. But that quickly proved to be incorrect. In the meantime, the hoardings have been continuously disbanded. We can see this, among other things, in the fact that the payout volumes at ATMs are still about 25 percent below the pre-corona level. If you want to compare the security of cash with card payments or digital payment options, you don’t get very far. If cash is stolen, for example, it is gone for good. If a payment card is stolen, the bank is usually liable.

Jochen Werne: It is undeniable that cash is seen by many as an anchor of trust in uncertain times. Electronic payment methods always risk a loss of trust due to technical failures. One of the last of these incidents was not long ago: during the pre-Christmas business on 23 December 2019, of all days, EC card payments were not accepted at many terminals. Many consumers who rely solely on digital payments have probably already had similar experiences of lesser consequence. Such situations can be observed time and again at the cash desks in department shops and supermarkets – for example, when the NFC chip on a card or simply the card reader does not work. Soon the eyes of the people standing around in the shopping queue turn to the payer, impatient and interested, trying to find out the name on the card of the supposedly insolvent unlucky person. Nevertheless, modern technologies are becoming more and more stable over time and a balance will be established between the various payment methods. Just as the “hoarded” will be returned to consumption or investment after the crisis. A cycle that, soberly, has always existed historically.

It became apparent that banks would no longer be able to offer free cash withdrawals from ATMs in the long term. This affects in particular people on low incomes, the elderly and, in general, all those who do not have access to digital forms of payment. Which solution do you think makes the most sense?

Leif Wienecke: Indeed, an accelerated dismantling of bank branches has been observed in recent months, but also before. The cost-benefit ratios seem to be out of proportion. Many end customers, especially older people, are suffering as a result. At the same time, however, one can also read about the creative solutions that savings banks, for example, are using to offer customers in rural areas the service they are used to (e.g. branch on wheels, transfer bus). I believe that other companies will fill the gap left by the banks. For some years now, supermarkets and petrol stations, for example, have been offering free “withdrawal” of cash. This trend to integrate banking services into the context of everyday life is known as contextual banking. The end customer wants to have access to cash or transactions wherever he or she is. As Solarisbank, we see the future in banking here.

Jochen Werne: Making an individual’s assets available as cash causes costs, just as paying with a card costs consumers money. The latest evaluation of 294 account models of 125 credit institutions in Germany by Stiftung Warentest shows that 55 models already charge fees for payment with the Girocard. It is the task of the institutions not only to manage their customers’ money, but also to meet the customer’s wish to make these assets available to them again in the form of cash or book money. The current practice of offering cash or accounts without fees and cross-subsidising them in return is a German phenomenon. The former head of BaFin, Dr. Elke König, already raised the question critically more than five years ago at the “Bank of the Future” event.

Today’s pressure on margins at banks now demands this adjustment. It is undisputed that, according to the German Bundesbank, ATMs are the most popular source of cash, accounting for 84 per cent of all cash withdrawals. Their number has risen by a good 18 per cent in Germany in recent years. On average, there is one ATM per 1,415 inhabitants. ATMs are therefore of enormous social and economic importance. It is not surprising that the area of “cash supply” is expressly listed as a “critical service” in Section 7 of the Critical Service Ordinance of the Federal Office for Information Security (BSI-KritisV), as a “service for the supply of the general public (…), the failure or impairment of which would lead to considerable supply bottlenecks or to threats to public security”. The fact that banks have to provide cash and cards to their customers, but are generally not able to do so profitably without charging is a long-term problem and needs to be improved. However, there is room for debate as to whether charges are the right way forward for consumers.

For US economics professor Kenneth Rogoff, the abolition of large banknotes is a first step. According to Rogoff, cash is synonymous with crime and the shadow economy – and in this respect it is a threat to the general public. Is cash really more “crime-sensitive” than digital payment methods?

Dr. Harald Olschok: As a “learned” Freiburg economist, I am always appalled by the populist and simplistic theses of the former chief economist of the IMF. It is much worse than you suggest. For Rogoff, “there is no question that cash plays a vital role in criminal activities, including drug trafficking, organised crime, extortion, corruption of authorities, trafficking in human beings and money laundering. (Der Fluch des Geldes, Munich 2016, p. 11). Oh yes, and undeclared work and illegal immigration are also owed to cash. Unfortunately, it has also been heard in the euro area. The 500 euro banknote has already been abolished. At the heart of the Rogoffian theses is the abolition of cash in order to impose negative interest rates. People should not save, but spend their money. This ignores the fact that fraud with non-cash means of payment, such as crypto-currencies, is booming. I expect that these forms of fraud will continue to increase. We must therefore assume the opposite.

Ralf-Christoph Arnoldt: Passing on a USB stick with millions of dollars in crypto-currencies, for example, is as easy as passing on a banknote. Criminals and the black economy are also part of the trend towards digitalisation, unfortunately sometimes even ahead of the investigating authorities.

Leif Wienecke: There is a lot of discussion on this topic and also conflicting studies. The Federal Government’s decision to tighten the reporting requirements for notaries, for example in real estate transactions, underlines Rogoff’s thesis. Nevertheless, I believe that it is not possible to generalise. Certainly, the anonymity of cash brings some advantages for criminals and money laundering can be curbed by switching to more strongly regulated, digital payment procedures.

And what about security? With cash, the problem is counterfeiting, with digital payments, for example, the tapping of identities and data. What is easier to protect?

Ralf-Christoph Arnoldt: I don’t see a big difference. It is always a mutual arms race. New security features for cash require more know-how and greater investment for counterfeiters. It is becoming more difficult, the number of offenders is getting smaller, but the sums that a counterfeiter puts on the market are bigger. The situation is similar for digital payments. As a financial group, we are doing everything we can to stay one step ahead of criminals through new cryptographic procedures, hardened systems and so on. It is not without reason that our experts are already working on cryptographic solutions that will be able to withstand the coming era of quantum computers. The challenge here is to maintain the convenience for the customers.

Jochen Werne: By its very nature, cash is without doubt the most robust payment method. This is regularly demonstrated in extreme scenarios such as disasters, failure of a digital infrastructure due to cyber attacks, natural disasters or technical failure. Cash is not tied to electricity, digital infrastructure, passwords or other technical features. In addition, the introduction of the second series of euro banknotes has enhanced security features and made banknotes more secure and more counterfeit-proof. As the Bundesbank reported at the beginning of the year, the number of counterfeit banknotes has fallen by a further five percent. With digital payment methods, consumers themselves have a responsibility to protect themselves. At the beginning of the Corona crisis, for example, the payment limit for contactless payments, such as in supermarkets, was increased. At first glance, this sounds harmless. But as a result, anyone can use a card – and it does not have to be their own – to pay for higher-priced goods without further security checks, such as by entering a PIN. And as far as data protection is concerned: with every cashless payment, consumers disclose personal information. Data that many companies use commercially.

Dr Harald Olschok: The risk of coming into contact with counterfeit money in Germany is still low. Most counterfeits are easy to detect. The security features of the current Euro series make it difficult for criminals. However, if digital payment methods are attacked, consumers should be aware that they lose much more than just their money.

China wants to take a step in this direction from 2021 onward at the state level as well. The aim is to link the Alipay payment solution with all private and state databases, including those in which cashless payment transactions are stored. The aim is to record and evaluate consumer behaviour. Subsequently, either rewards are offered or sanctions are threatened. Anyone who accumulates too much debt or fails to pay it back is no longer allowed to use express trains or planes in China. Although such a development is completely out of the question in European democracies in the foreseeable future, do you also expect consumer behaviour to play a much greater role in credit rating in the future?

Jochen Werne: Harvard history professor Niall Ferguson coined the term “new cold war” over a year ago. This “Cold War” is mainly about one technology leadership in artificial intelligence and takes place between the United States and China. Technologies are not good or bad, but how and for what purpose they are used by us humans, determines the outcome. Just because something is now technically possible, it does not necessarily make sense for a society. It is a great value of liberal democracies that these issues are discussed, that privacy is protected and that the state cannot act on its own authority.

On the question of creditworthiness, it can be said that the better a credit institution knows the borrower, the better a risk assessment can be made in order to quantify credit default risks. When assessing creditworthiness, the institution is required to use all relevant and available data for the decision. Today, it is technically possible to enrich the data provided by the future borrower with information about him/her from the Internet and social media and to round off the data with the help of AI algorithms and peer group comparisons. However, there is a high risk that private personal data may be processed here if inadvertently and the protection of privacy may be violated. This must be prevented. However, it remains to be seen how this will be dealt with in the future.

Leif Wienecke: First and foremost, it is a matter of making sensible use of the many possibilities of generated data to create added value. Companies such as banks primarily face the challenge of preparing their customers’ data in a meaningful way and integrating it for new applications. The ecosystems of the “GAFAs” or Alipay are “data first” companies which are integrated into the everyday life of their users. In principle, they only make decisions based on data and empirical findings. The above description from China, however, does not go hand in hand with our understanding of data or consumer protection, so we do not see this coming either.

On the other hand, it is of course essential to pursue data-driven innovation. Even the credit rating system that exists today can certainly be extended via relevant, contextual data points, in the interests of consumers and credit institutions. The topic of “social scoring”, i.e. the use of customer data from social networks, is controversial in Germany and is discussed above all in the context of consumer protection. This is correct, because the consumer should not only have to give his consent for such scoring, but should also be able to understand the algorithm and complain in case of discrimination.

Recently, initiatives have been heard repeatedly to make a CBDC (Central Bank Digital Currency) accessible to all citizens and not to limit an e-euro to institutional participants in the financial markets. What do you think about this?

Leif Wienecke: The CBDC issue is still in its infancy and has many facets. It is mostly about increasing the efficiency of payment transactions. End customers also benefit from this. In principle, innovation processes and initiatives to transform the financial industry are to be seen as positive. As with all topics with a European or international scope, it is important to create a uniform regulatory framework. Precisely because the introduction of a digital central bank currency for the public would not be accompanied by a change in the existing monetary system. At Solarisbank, we have been dealing with the block chain and crypto currency industry for over two years. Last year, we founded the subsidiary Solaris Digital Assets to realise our vision of the broad use of digital assets.

Ralf-Christoph Arnoldt: Unfortunately, very different things are mixed up here. Firstly, there is the technology on which most crypto currencies are based: the block chain. It is highly interesting because rights (to money, benefits from contracts, etc.) can be transferred securely and traceably. This technology has its use cases and will increase in importance. To issue a currency based on this digital solution is certainly forward-looking but not without risks. The speed with which sums of money can be transferred would in itself increase the speed at which money circulates to an extent at which we lack economic experience. Questions also remain to be answered about the security of the currency and who is responsible for the counter-value. It is therefore to be welcomed that we are dealing with this issue at an early stage so that we can learn with manageable and calculated risk.

The concept of the euro, on the other hand, suggests a digital currency as a means of payment. In my view, it is still too early for that. Not only because the overall economic effects can only be estimated to a limited extent at present, but also because this technology is geared to the security and distribution of data, not to transaction efficiency. The number of transactions is technically limited. There are concepts such as the Lightning technology to circumvent this and allow more transactions. However, the latter again functions as an intermediary according to principles similar to those of traditional payment transactions. Transactions are executed and then “booked” in the block chain – similar to a central bank transfer.

Likewise, too little attention is paid to the ecological aspect. According to estimates, Bitcoin alone consumed around 74 terawatt hours in one month at the end of 2019. By way of comparison, Germany’s total electricity consumption over the same period was around 47 terawatt hours.

And now the crucial question at the end: How do you make cashless payments?

Ralf-Christoph Arnoldt: With the Girocard – as far as possible contactless of course, and with pleasure also by mobile phone.

Leif Wienecke: I use Google Pay with my debit cards from our partners Tomorrow, Vivid Money and Bitwala. Offline I use the corresponding Visa cards. And online I also use PayPal.

Jochen Werne: Of course with cash and cashless.

Dr. Harald Olschok: In food retailing and gastronomy regularly with cash. For larger expenses, including refuelling, with credit cards.