It was a pleasure contributing in co-authorship with the AI-expert and friend Dr. Johannes Winter / Jochen Werne to this new Springer Gabler publication ”Praxisbeispiele der Digitalisierung” (Best Practice of Digitilisation) which is available now as e-book and paperback at https://link.springer.com/book/10.1007/978-3-658-37903-2

Cash, Book Money, Crypto Currencies and the Digital Euro

The aim of the chapter in the book is a contribution to the debate of money in the digital age. It combines historical insights into the meaning of money with the latest technological developments, to compare visions of the financial industry with realities and to develop options for action to shape the digital transformation of money.

Abstract: In a world where tech companies are leading campaigns to create a new cryptocurrency and bitcoin is surpassing the US$50,000 mark because a visionary electric car maker wants to recognise the cryptocurrency as a means of payment, some fundamental questions arise: how must money be defined in a digital world to reliably fulfil the characteristics of a universally recognised store of value and medium of exchange? And what changes are in store for the financial industry when so-called stablecoins proliferate and challenge the banks’ classic deposit business and their outdated business models? The aim of this contribution to the debate is to combine historical insights into the meaning of money with the latest technological developments in the digital age, to compare visions of the financial industry with realities and to develop options for action for shaping the digital transformation of money.

Thomas Apitzsch, Michael Pfleger, Frederike HaberlandPages 309-325

About Springer Gabler

Springer Gabler Verlag is the leading specialist publisher for the business sector. Its classic and digital teaching materials and specialist media address current business questions and provide reliable, practical solutions.

Reflections by Jochen Werne, Chief Development & Chief Visionary Officer Prosegur Germany (published in Prosegur Express 02/2021)

In all debates on analogue and digital means of payment, “trust” is always at the centre of the discussion: trust in the state-social order, which stands as a guarantor for stability and security of the fiat money issued. In this respect, some would almost like to marvel at how Bitcoin & Co. have managed to gain such trust in such a short time that a market capitalisation in the billions has been achieved. One of the points is certainly the technological confidence in the non-manipulability of the blockchain. But is the blockchain really not manipulable, or is it rather a question of time before an attack will succeed? And what conclusions are central banks around the world drawing from this as they look at creating central bank digital currencies? Currencies designed to bridge the gap between the stability of analogue central bank money and the demands of our digital age.

Perhaps the solution for a trustworthy and generally accepted today and now lies in a hybrid model: in a cryptocurrency, in form of a stablecoin, that is 100 per cent backed by physical central bank money. This means that every digital token has a unique physical counterpart (euro). Due to the tradability of the tokens, the flexibility of book money is paired with the guarantee of physical central bank money. Last but not least, a regulated trustee function guarantees that the existing and securely stored central bank money is always paired with its digital twin. Thus. the best of both worlds is firmly united.

gi-Geldinstitute published „For the good of all – Why standards are so important“, A plea for future-oriented minimum standards in the CIT industry, underlining Prosegur‘s frontrunner role as resilient infrastructure provider in the security and cash management industry.

Find Original in German HERE. Translation generated with deepL.com

A plea for future-oriented minimum standards in the CIT industry. The neighbouring banking industry (and often the customers of CIT companies) is already protected by standards such as MaRisk and BAIT. However, cash-in-transit companies that work closely with their customers (banks) have less high standards in IT, whereby the industry is becoming increasingly digitalised. Prosegur argues for higher standards across the CIT industry.

Emeritus professor of literature Hans-Dieter Gelfert, who has spent many years researching German, British and American mentalities, expressed in an interview with Deutsche Welle that the orderly society of modern Germany has a long genesis. “Order is one of the sacred words in Germany, and that has something to do with the German emphasis on security as opposed to freedom,” he said. “For the last thousand years, security has always been the supreme value and order is a mainstay of security.” Part of Germany’s success is built on norms. It is not without reason that the encyclopaedia “Brands of the Century” lists more than 200 German brands such as Hipp or Tempo as examples of entire product categories. The entire title is: “German Standards – Brands of the Century”. Aha, standards then – a coincidence?

Without rules, norms or minimum standards, a modern society would be almost inconceivable. They structure, make things comparable and act as a control mechanism. Cultural imprints and regional differences come into play in their design. For example, many an EU citizen groans about the General Data Protection Regulation when a form has to be filled out for consent to the use of personal data. On the other side of the Atlantic, people certainly pay respect to the GDPR for the standards it sets. Standards that reflect the values of an enlightened Europe.

Own rules in the business world

Beyond social norms and local legislation, there are other rules in the business world. There is hardly an industry that has not already given itself a catalogue of minimum standards. This is an advantage for many, because the complexity on the supply side is often reduced for those asking. But the question must be allowed whether minimum standards are sufficient and whether they all focus on the well-being of customers and society. Too often the focus is on the providers. Yet there are standards that need to be established today in order to prepare for future challenges.

Prosegur is committed to more than minimum standards to position the entire industry for the future and to ensure society’s trust in this system-critical industry. An industry that does nothing less than ensure the unrestricted supply of central bank money to the population and the safe return of several million euros of cash income daily to the accounts of businesses to ensure their liquidity.

A look at the customer environment reveals that the related banking industry is leading the way: with MaRisk (Minimum Requirements for Risk Management) or BAIT (Bank Supervisory Requirements for IT), credit institutions have positioned themselves for the future. Since banks usually cooperate with a cash-in-transit company, it is only logical for Prosegur to apply these already existing requirements in an identical manner to its own business operations today and consequently to demand rapid implementation from all providers of cash and valuables transport.

All players operating in such an important part of our economic life must keep their eyes on the future and never cling to the status quo. Today, topics such as digitalisation and environmental protection naturally belong in the programmes of sustainably oriented companies. Every organisation needs courage, creativity and a willingness to invest in finding a digital language for analogue solutions. This fact is of particular importance in the Corona pandemic, because it acts as an accelerator for the global digital transformation.

Politicians underlined that they have recognised this on 9 December 2020 with the BMI’s draft bill for a second law to increase the security of information technology systems. But even before the draft becomes law, the following applies to Prosegur: the further development of current standards, investment in sustainable technologies and personnel as well as in the certification of processes and models must absolutely be in the interest of every serious money and value service provider already today.

Resilience through standards and digitalisation

It is essential to arm oneself against all kinds of threat scenarios – known and new, present and future – and to become resilient against external shocks. To be resilient so that, as a critical infrastructure, citizens can access money even in crises or exceptional situations. And to offer support to other critical infrastructures to also become resilient in order to avert supply bottlenecks for the population in cooperation. Prosegur consistently pursues this maxim, among other things with the smart cash procedure, in which cash receipts, for example in the supermarket or pharmacy, are deposited in a smart safe, where they can be credited to the business account via Early Value. Independent of the physical collection of the money, the company can use it to do business. A lack of liquidity does not become a showstopper for supermarkets and pharmacies in times of crisis. They remain open and the supply of goods and medicines is maintained. In the impulse paper “Resilient pioneers from business and society” of the German Academy of Science and Engineering (acatech), Prosegur Smart Cash was presented in December 2020 as a resilient concept for success.

Standards create resilience. So what standards should the cash and cash-in-transit industry additionally orient itself to? In Prosegur’s opinion, the standards of the credit institutions with which the cash and valuables transport industry cooperates on a daily basis. Not only in terms of their own resilience, but also in order to be a true partner for customers with their very own challenges in the low and negative interest rate environment, in the digital transformation and in the climate crisis. Then the players in this industry not only transport, process and store values, they also embody them and prepare to take on even greater responsibility in the “cash cycle” value chain.

HOT OFF THE TAPE: Business Transformation in the Digital Age – Insight into Practice from an Expert’s Perspective

It was a great pleasure being invited as guest to the brand new podcast format POLEDIFY. With Poledify, Felix Gehm offers insights into the routines, mindsets and habits of experts and thought leaders from a wide range of disciplines.

Jochen Werne is Chief Development Officer and Chief Visionary Officer of Prosegur Germany. Prosegur Group is one of the leading security service providers worldwide with over 175,000 employees on five continents. Jochen Werne is, among other things, a member of the Learning Systems Platform, which advises the German government on artificial intelligence, and of the Royal Institute of International Affairs Chatham House, one of the most important think tanks in the world. Jochen was listed as one of the AI experts in Germany by Focus magazine. He is also an author, keynote speaker, internationally awarded NGO founder and specialist in business development and transformation, and international diplomacy. In 2020, the Tyto Tech Power List named him one of the 50 most influential people in the tech scene in Germany.

Topics of this episode:

What does digital transformation mean for “traditional” business sectors? How Prosegur plans to master digital transformation How not to be deterred by big challenges The most important characteristics of a leader in the face of such challenges

Links and other things from the episode: The interview between Bill Gates and Warren Buffet: shorturl.at/mGPYZ Books: Utopias for Realists by Rutger Bregman Mordern Monopolies by Alex Moazed and Nicholas L. Johnson Here you can find Jochen Werne and everything about Prosegur: Jochen Werne LinkedIn: https://www.linkedin.com/in/jochenwerne/ Jochen Werne Website: http://jochenwerne.com/ Prosegur LinkedIn: https://www.linkedin.com/company/prosegur/ Prosegur website: https://www.prosegur.com/en/jobs Platform Learning Systems: https://www.plattform-lernende-systeme.de/home-en.html

Questions, criticism, suggestions or anything else? Write to me! Instagram: https://www.instagram.com/poledify/ Twitter: https://twitter.com/ThisIsFelixGehm or simply send an email to poledify@gmail.com Where does the fine music (intro & outro) come from? The fine music in the intro and outro is produced by pads. Behind the artist name is Patrick, who has finally decided to record all his little songs. You can find it all here: YouTube: bit.ly/33TOFcN Instagram: https://bit.ly/2XWFDIm Soundcloud: https://bit.ly/3oYQA8k

Interview mit Jochen Werne, CDO/CVO Prosegur Germany, zu effizienteren Prozessen nach dem Lockdown

In seinem Experten-Interview beleuchtet Jochen Werne zentrale Aspekte aus Sicht von Gastronomie und Handel für effizientere Prozesse nach dem Lockdown

Publiziert von Prosegur Deutschland: LINK HIER

Herr Werne, was sind Ihre persönlichen Beobachtungen in Bezug auf Wirtschaft und Gesellschaft nach einem Jahr der Krise?

Jede Krise bringt natürlich zunächst einmal Leid mit sich und eine Pandemie selbstverständlich Leid für den Einzelnen und seine Angehörigen, wenn ihn das Schicksal, der durch das Virus ausgelösten Krankheit ereilt. Alles Weitere ist wie eine Kettenreaktion. Beginnend vom Staat, der die hoheitliche Aufgabe hat seine Bürger zu schützen und dies im Falle einer Pandemie auch mit dem Herunterfahren des gesellschaftlichen Lebens durchsetzt. Dies wiederum hat bei geschlossenen Unternehmen die Folge drastischer Einkommenseinbußen bei weiterlaufenden Kosten. Bei nicht ausreichender Liquidität führt dies dann zu Insolvenzen, Arbeitsplatzverlusten und im schlimmsten Fall zu einer Wirtschaftskrise. Geschichtlich gesehen hat jedoch auch jede Krise – und diese ist keine Ausnahme – dazu geführt, dass die Wirtschaft effizienter wird und technologische Trends eine Beschleunigung erfahren.

Im Moment – in dieser für viele so schwierigen Situation – beobachte ich eine unglaubliche und inspirierende Kreativität. Sie beginnt bei den kleinen und mittelständischen Unternehmen, die sich versuchen agil, der gefühlt täglich neuen Lage anzupassen, sich zu verbessern, Kosten zu optimieren und sich optimal für die Zeit nach der Krise aufzustellen. Das stimmt hoffnungsfroh für die Zeit nach der Krise und es ist eine große Motivation mit einem fantastischen Team den eigenen Teil dazu beitragen zu können.

Jede Krise fordert von Unternehmen eine gewisse Resilienz.Die nationale Akademie der Technikwissenschaften (acatech), hat zum Digitalgipfel der Bundesregierung im November ein Impulspapier mit dem Titel „Resiliente Vorreiter“ vorgestellt. Darin wird Prosegur mit deiner digitalen Smart Cash Lösung als Best Practice Besipiel für ein zukunftsgerichtetes und kostenoptiertes Cash Managment für den Handel und die Gastronomie genannt. Wie funktioniert Prosegur Smart Cash?

Mit Prosegur Smart Cash können Gastronomen, Einzel- oder Großhändler Bargelder zur sicheren Verwahrung direkt in das Smart Cash Gerät einführen. Das Besondere – im Gegensatz zu einem einfachen Tresor ist es, dass einmal eingeführt, das Gerät automatisch das tägliche Zählen und Abrechnen des Bargeldes übernimmt. Die Zeit- und somit Kostenersparnis in den internen Prozessen bei unseren Kunden ist teilweise beträchtlich. Das Gerät verfügt über ein Kommunikationsprotokoll, das die Überweisung des Wertes der Abholung auf das Bankkonto des Kunden innerhalb von 24 Stunden ermöglicht. Sobald sich das Geld im Gerät befindet, liegt die Verantwortung und Verwaltung bei dem spezialisierten Team von Prosegur Cash, das für den Transport und die Verwahrung des Geldes zur Bankfiliale verantwortlich ist. Somit entfällt auch der teilweise tägliche und nicht ungefährliche Gang zur Bankfiliale.

Was sind die Vorteile von Prosegur Smart Cash?

Zusammengefasst spart es unseren Kunden Zeit und Geld und schafft mehr Transparenz und Sicherheit. Die Kunden von Prosegur Smart Cash können ihr Bargeld schnell und sicher aufbewahren und so unbekannte Verluste reduzieren. Prosegur Smart Cash ermöglicht eine Zeitersparnis durch die Automatisierung des Zählens und bei der täglichen Abrechnung des Bargeldes. Darüber hinaus muss der Kunde dank Prosegur Smart Cash nicht zur Bank gehen, um das Bargeld einzuzahlen, da Prosegur für die Sicherheit bei der Verwaltung und Übergabe des gesamten Bargelds an die Bank sorgt, was gefährliche Situationen für den Kunden vermeidet und ihm hilft, Zeit zu sparen, damit er sich voll und ganz seinem Geschäft widmen kann. Außerdem reduziert eine Smart Cash Lösung das häufige und teure Phänomen des sogenannten „unbekannten Verlustes“.

Was ist „Unbekannter Verlust“?

Jochen Werne: Hierbei handelt sich um den Verlust von Inventar oder anderen Geschäftsressourcen, der auf eine Vielzahl von Faktoren zurückzuführen ist, wie z. B. interner und externer Diebstahl, Verwaltungsversagen, Betrug oder Fehler im Cashflow. Diese Situation stellt für Gastronomen und Einzelhändler oftmals ein zentrales Problem dar.

Was beobachten Sie, in Bezug auf ihre Kunden und wie sich diese auf die Zeit nach dem Lockdown vorbereiten?

Jochen Werne: Es ist eine unglaubliche Sehnsucht zu beobachten, endlich wieder mit seinen Kunden in Kontakt treten zu dürfen, um Ihnen wieder leidenschaftlich die eigenen Leistungen und Services bieten zu dürfen. Viele Kleine und mittelständische Unternehmen, von den großen ganz abgesehen, haben massiv in Hygienekonzepte investiert und versucht die Zeit zu nutzen um die eigenen Prozesse zu kostenoptimieren.

Wir selbst haben noch nie so viele Beratungsgespräche in Bezug auf smarte Bargeldlösungen geführt wie heute. Dies hat sich noch einmal erhöht, nachdem deutliche Aussagen und Studien der Weltgesundheitsorganisation (WHO) und der Bundesbank darauf hinwiesen, dass die hygienische Sauberkeit vom Bargeld mindestens gleich dem von Kartenzahlungen ist und eine Ansteckungsgefahr in Bezug auf unsere täglichen Bezahlmethoden in beiden Fällen geringst ist.

Interessanterweise haben wir auch eine hohe Nachfrage nach Effizienzhebung bei Unternehmen mit kleinem Bargeldaufkommen festgestellt und die Zeit genutzt um als erstes Unternehmen in Deutschland auch für diese Gruppe eine entsprechende sehr kostengünstige digitalte Lösungen zu entwickeln. Eine Krise zwingt immer alle effizienter zu werden und es gibt meiner Meinung nach nichts besseres, als dies gemeinsam zu tun. Nur so schafft man es gemeinsam aus einer Krise gestärkt hervor zu gehen.

The possibility to buy Bitcoins with cash in a regulated process at a designated ATM intelligently combines the best of both worlds. As Germany’s market leader in cash transport and processing, Prosegur guarantees secure cash handling for Europe’s largest operator of Bitcoin ATMs.

Find details about the project in this article from t3n, translated with Deepl.com. Find original HERE

Sutor Bank has announced a number of cooperations in the fintech sector in recent years. In the future, the tradition-rich bank will set up Bitcoin ATMs in Germany. The project will be implemented as a cooperation with the Hamburg-based Sutor-Bank, the Austrian Kurant, which claims to be Europe’s largest operator of Bitcoin ATMs, as well as the startup Spot9 with the participation of IDnow, Coinfirm and Prosegur. According to the participants, this is a unique cooperation that meets all the requirements of the German banking supervisory authority Bafin – and the number of participants already suggests how high they are. Their rules include, for example, compliance with money laundering guidelines and the secure identification process of customers, which IDnow takes over. Finally, Prosegur is involved as a security service provider in the area of cash transport and processing and is supposed to guarantee secure cash handling.

Last week, the first machine was set up in Berlin – in the medium term, a nationwide network of Bitcoin machines is to be set up. “Spot9’s vision is to enable everyone, even without extensive prior knowledge, to use our Bitcoin ATMs. That is why it is very important for us to understand exactly how customers behave at the vending machine before we open the additional locations,” says Johannes Gorski, CEO of Spot9.

Vending machine solution: Easier than buying bitcoin via an exchange

The vending machine solution is intended to be a safe and easy-to-understand alternative to buying online and carries fewer risks than buying cryptocurrencies on Bitcoin exchanges, the parties involved explain. The purchase process works via cash and is similar to the operation of a conventional ATM. Thus, the offer is aimed at customers who want to buy cryptocurrencies in their normal everyday life.

After the first vending machine has been set up in Berlin, but can be used by a selected test group for the time being, the primary goal is to get to know the user behaviour of the customers better and thus ensure an optimal user experience. The opening of further locations is to take place in the course of the first quarter of 2021, whereby the Corona Factor will of course still have an impact.

It should be possible to use the Bitcoin ATMs with any digital Bitcoin wallet. The user is thus independent of an ATM-specific wallet. However, in order to use the Bitcoin ATMs, the customer must first go through the registration process with verification on the Spot9 website.

by JOCHEN WERNE published in DER BANK BLOG (30 October 2020) – For the original version in German please follow this LINK – English version translated by Deepl.com

“Disposal power” or “authority to dispose” are legal terms which are of great importance in the discussions on cash and book money. It also concerns the freedom of choice of citizens. The German language today is much more extensive than the 100,000 words used by Goethe in his time. We hardly use many of these words, which are so characteristic of our language, despite their meaning. Perhaps some readers feel the same way about the word “Verfügungsmacht” as I did when I consciously read it for the first time in a quotation from the former president of the Federal Constitutional Court, Prof. Dr. Udo Di Fabio. And perhaps it is like with many things in life that one only realises the deeper meaning at the moment when one deals with it in more detail. In our modern times, hardly anyone will visit the university library to quickly get to grips with a topic. Instead, people google the library to get an overview. And while less than 20 years ago we would have found our first little research happiness about the term “power of disposal” or also “authority to dispose of property” in the library of the law faculty, Internet research reveals in seconds a glance at a litany of legal forums.

Definition of power of disposal What is striking here is that the focus is not on the definition of control, but that the topic of regaining control dominates the first page on Google. Inevitably, this reminds me of my first visit to the Munich Google office many years ago. Almost rapturously in his remarks about the power of the algorithm, a sales employee of the world’s most powerful search engine asked the group if we knew where on the Internet they hid a body. With a glance into his head-shaking auditorium, he solved the riddle with a smile and said: “On the second page of Google search. Inevitably, of course, one then asks oneself – albeit only rhetorically – whether the Google business model works in particular because many have simply relinquished control over their data. The power of disposal or also power of disposition is defined as the “legal power to dispose of an object”. Which is banal, meaning that I should also have the power of disposal over what belongs to me – in other words, what is legally my property. However, the success of my own research on the first Google page suggests one thing above all else to the reader: that the power to dispose of property can be lost. For example, also of your own money? In order to answer this question, one should basically distinguish between cash and book money.

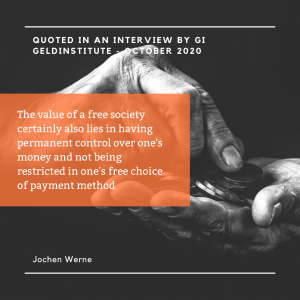

Cash, book money and the power of disposal With cash, I have direct unlimited physical control over my money in the form of coins or notes. This power of disposal can of course be lost if I am robbed or simply lose my wallet. Without entering into the legal depths of “normal” debt and the right to dispose of money, citizens have in principle all the means guaranteed by the state at their disposal to recover their property. The same applies to book money, if, for example, money is lost through credit card fraud when shopping online. The limits of non-physical power of disposal would, however, quickly become apparent if a bank went bankrupt and the money parked in the account in excess of the deposit guarantee was no longer available. Cash, book money and free availability It is utopian and not at all sensible to hoard all one’s “money” as cash. But it is certainly important to make clear what it means to no longer have the freedom of choice between cash and book money and thus to completely give up one’s right to physical availability of money. In the concluding sentence of his speech at the 2018 Cash Symposium of the Deutsche Bundesbank, Udo Di Fabio underlined what is probably the most important point in the current discussion surrounding this election. He said that it should not be “disregarded” in principle that every citizen should be able to freely dispose of his money – his “exchangeable assets”. He further added that this was particularly true when “financial privacy” was considered a legal requirement. This means that a society whose entire assets would only be managed digitally in book money could also only exercise limited individual power of disposal over its money and would have to face the question “whether the state, through its central bank, would be entitled to carry out a controlled devaluation through negative interest rates, booking discounts or fees on credit balances”. Prof. Di Fabio further points out that this would then not only be an encroachment on ownership but, as a result, possibly also the imposition of a special levy, which is only permitted under strict conditions in the German legal system.

Conflicts of interest and trust It is easy to see that this issue can give rise to considerable conflicts of interest in the triangular relationship between citizens (- how can I protect and increase my money), government (- how can public debt be reduced) and central bank (- how can economic and monetary stability be ensured). This is particularly true in the light of the continuing challenges posed by the Corona pandemic. It is thanks to the excellent work of the Deutsche Bundesbank since the Federal Republic of Germany came into existence and the confidence it has built up in our currency that the confidence of the public in both cash and book money is so high in this country. Freedom of choice between cash and book money Of course, another decisive aspect of this trust is the freedom of choice between cash and book money, which the Bundesbank also advocates. This freedom of choice also offers banks the opportunity to deal flexibly with the funds. For example, instead of charging 100 percent negative interest on book money to citizens or companies, banks could also physically hold it or have it held in safekeeping as cash. Since it is not part of a bank’s core competence to operate high-security systems and one certainly does not want to expose one’s own employees to the risk of a robbery or the blackmailing abduction of a family member, there is of course the possibility of outsourcing such a service in a LCR-compatible and MaRisk-compliant manner. A service that supports the customer in parts of his liquidity management and does not make it difficult for him to possibly maintain his own safe in his own four walls and without a security concept and thus endanger himself and his family. “Money is coined freedom” In his prose work “Records from a House of the Dead”, the Russian writer Fyodor Mikhailovich Dostoevsky describes his own experiences in Siberian captivity and formulates the later much quoted sentence: “Money is coined freedom”, thereby describing the vital relevance of a free exchange of goods in an unfree environment – and this through coined cash money. For the young Dostoyevsky, the changeover to a pure book money system in Siberian prison would have meant the withdrawal of his individual power of disposal over money, so that in reverse he would no longer have any assets which he could have used for the exchange of goods and other things. He describes this situation in the quintessence as follows: The suffering of prisoners who do not have money is “10 times greater”. It is therefore reasonable to assume that the intellectual, serious discussions about the freedom of choice between cash and book money and the freedom of citizens in a constitutional state, which is freely consolidated in its constitution, would please Dostoevsky with his experiences in an unfree society. And it is characteristic of our open society that, especially in a crisis like the present one, we are conducting and continuing the debate on freedom of choice and power of disposal at this level, and not only with regard to our money.

Does cash have a future? An article by Dunja Koelwel, editor in chief of gi Geldinstitute | 20.10.2020 – 13:02

Please follow this LINK for the original source in German. Translation made by DeepL.com

Cashless payment is on the advance worldwide, only the Germans hang on to cash. gi Geldinstitute therefore wanted to know from Ralf-Christoph Arnoldt (Bundesverband der Deutschen Volksbanken und Raiffeisenbanken BVR), Jochen Werne (Prosegur Germany), Dr. Harald Olschok (BDSW) and Leif Wienecke (Solarisbank) Does cash still have a future?

Signs such as “Cash only” should be a thing of the past in Germany, according to the digital association Bitkom. Wherever customers can pay, at least one digital payment option that can be used throughout Europe should be offered on a mandatory basis, according to the “Bitkom theses on freedom of choice in payment”.

“Cash shows itself to be an anchor of trust in uncertain times. With increasing concern about the corona virus, the amount of physical cash in circulation in the USA, for example, has risen,” says Jochen Werne, member of the management of Prosegur Cash Services Germany. gi geldinstitute therefore asked: What is the current situation regarding ‘war on cash’?

Since the Corona crisis, more and more people have been paying with cards or smartphones instead of with coins or notes. Is this a trend that is slowly eliminating cash? What is your perception?

Ralf-Christoph Arnoldt: Indeed, in recent months we have seen gains in card payments, especially in payments with Girocard. In the first half of 2020, transaction figures have increased by 20.7 percent compared to the same period last year. However, cash still plays an important role in everyday life in Germany, even if this love is eroding.

According to the Eurohandelsinstitut (EHI), the share of cash in turnover in 2019 was still 45.5 percent. Cash offers some advantages from the customer’s point of view. Paying with cash is convenient for the customer, anonymous, immediately final. Cash is freedom for customers. Regulators and business circles involved in the cash circle should accept this as a fact and not force them to change it.

Dr. Harald Olschok: Without doubt, a new phase of “war on cash” began during the Corona crisis. 75 percent of the member companies of the BDGW expect sales next year to be up to 20 percent lower than in the past. We assume that the proportion of cash payments in the retail sector will fall from around 48 percent at the beginning of 2020 to well below 40 percent. However, the crisis has also shown that Germans continue to have great confidence in cash as a secure means of payment and store of value. According to a survey by YouGov, Germans also cannot imagine living in a cashless society.

Leif Wienecke: Since the Corona crisis, we have seen an acceleration of many trend developments, some of which were already foreseeable before. This also includes contactless payment. This customer behaviour, which is relatively new in Germany, fits in well with corona-related hygiene measures. Basically, it can be said that, in addition to hygiene considerations, end customers are primarily looking for speed when choosing a means of payment. This is where digital and contactless payment methods come into play. Over the next few years, we will see a further decline in cash payments and an increasing use of digital payment methods such as mobile wallets.

Jochen Werne: What is important to people when it comes to their money – the “fruits of their labour”? Certainly its unlimited availability. If they can have confidence that they can get their money at any time, people choose the payment option that is most convenient for each individual. Some prefer to pay by smartphone, while for others it’s “only cash is true”. It is fundamental that we as consumers are free to decide from which means of payment we can freely choose. Freedom of choice is the key word.

A “per cash” argument often made is that technology is vulnerable and that in a crisis the value of security is always the highest good. This is why many people have been hoarding cash at the beginning of the lockdown. Do you believe that this money will now come back into circulation? And what do you think about the technological error potential of digital payment options?

Ralf-Christoph Arnoldt: The fact that cash was hoarded at the beginning of the lockdown was more due to the fact that people thought the cash supply could be endangered because of the Corona crisis. But that quickly proved to be incorrect. In the meantime, the hoardings have been continuously disbanded. We can see this, among other things, in the fact that the payout volumes at ATMs are still about 25 percent below the pre-corona level. If you want to compare the security of cash with card payments or digital payment options, you don’t get very far. If cash is stolen, for example, it is gone for good. If a payment card is stolen, the bank is usually liable.

Jochen Werne: It is undeniable that cash is seen by many as an anchor of trust in uncertain times. Electronic payment methods always risk a loss of trust due to technical failures. One of the last of these incidents was not long ago: during the pre-Christmas business on 23 December 2019, of all days, EC card payments were not accepted at many terminals. Many consumers who rely solely on digital payments have probably already had similar experiences of lesser consequence. Such situations can be observed time and again at the cash desks in department shops and supermarkets – for example, when the NFC chip on a card or simply the card reader does not work. Soon the eyes of the people standing around in the shopping queue turn to the payer, impatient and interested, trying to find out the name on the card of the supposedly insolvent unlucky person. Nevertheless, modern technologies are becoming more and more stable over time and a balance will be established between the various payment methods. Just as the “hoarded” will be returned to consumption or investment after the crisis. A cycle that, soberly, has always existed historically.

It became apparent that banks would no longer be able to offer free cash withdrawals from ATMs in the long term. This affects in particular people on low incomes, the elderly and, in general, all those who do not have access to digital forms of payment. Which solution do you think makes the most sense?

Leif Wienecke: Indeed, an accelerated dismantling of bank branches has been observed in recent months, but also before. The cost-benefit ratios seem to be out of proportion. Many end customers, especially older people, are suffering as a result. At the same time, however, one can also read about the creative solutions that savings banks, for example, are using to offer customers in rural areas the service they are used to (e.g. branch on wheels, transfer bus). I believe that other companies will fill the gap left by the banks. For some years now, supermarkets and petrol stations, for example, have been offering free “withdrawal” of cash. This trend to integrate banking services into the context of everyday life is known as contextual banking. The end customer wants to have access to cash or transactions wherever he or she is. As Solarisbank, we see the future in banking here.

Jochen Werne: Making an individual’s assets available as cash causes costs, just as paying with a card costs consumers money. The latest evaluation of 294 account models of 125 credit institutions in Germany by Stiftung Warentest shows that 55 models already charge fees for payment with the Girocard. It is the task of the institutions not only to manage their customers’ money, but also to meet the customer’s wish to make these assets available to them again in the form of cash or book money. The current practice of offering cash or accounts without fees and cross-subsidising them in return is a German phenomenon. The former head of BaFin, Dr. Elke König, already raised the question critically more than five years ago at the “Bank of the Future” event.

Today’s pressure on margins at banks now demands this adjustment. It is undisputed that, according to the German Bundesbank, ATMs are the most popular source of cash, accounting for 84 per cent of all cash withdrawals. Their number has risen by a good 18 per cent in Germany in recent years. On average, there is one ATM per 1,415 inhabitants. ATMs are therefore of enormous social and economic importance. It is not surprising that the area of “cash supply” is expressly listed as a “critical service” in Section 7 of the Critical Service Ordinance of the Federal Office for Information Security (BSI-KritisV), as a “service for the supply of the general public (…), the failure or impairment of which would lead to considerable supply bottlenecks or to threats to public security”. The fact that banks have to provide cash and cards to their customers, but are generally not able to do so profitably without charging is a long-term problem and needs to be improved. However, there is room for debate as to whether charges are the right way forward for consumers.

For US economics professor Kenneth Rogoff, the abolition of large banknotes is a first step. According to Rogoff, cash is synonymous with crime and the shadow economy – and in this respect it is a threat to the general public. Is cash really more “crime-sensitive” than digital payment methods?

Dr. Harald Olschok: As a “learned” Freiburg economist, I am always appalled by the populist and simplistic theses of the former chief economist of the IMF. It is much worse than you suggest. For Rogoff, “there is no question that cash plays a vital role in criminal activities, including drug trafficking, organised crime, extortion, corruption of authorities, trafficking in human beings and money laundering. (Der Fluch des Geldes, Munich 2016, p. 11). Oh yes, and undeclared work and illegal immigration are also owed to cash. Unfortunately, it has also been heard in the euro area. The 500 euro banknote has already been abolished. At the heart of the Rogoffian theses is the abolition of cash in order to impose negative interest rates. People should not save, but spend their money. This ignores the fact that fraud with non-cash means of payment, such as crypto-currencies, is booming. I expect that these forms of fraud will continue to increase. We must therefore assume the opposite.

Ralf-Christoph Arnoldt: Passing on a USB stick with millions of dollars in crypto-currencies, for example, is as easy as passing on a banknote. Criminals and the black economy are also part of the trend towards digitalisation, unfortunately sometimes even ahead of the investigating authorities.

Leif Wienecke: There is a lot of discussion on this topic and also conflicting studies. The Federal Government’s decision to tighten the reporting requirements for notaries, for example in real estate transactions, underlines Rogoff’s thesis. Nevertheless, I believe that it is not possible to generalise. Certainly, the anonymity of cash brings some advantages for criminals and money laundering can be curbed by switching to more strongly regulated, digital payment procedures.

And what about security? With cash, the problem is counterfeiting, with digital payments, for example, the tapping of identities and data. What is easier to protect?

Ralf-Christoph Arnoldt: I don’t see a big difference. It is always a mutual arms race. New security features for cash require more know-how and greater investment for counterfeiters. It is becoming more difficult, the number of offenders is getting smaller, but the sums that a counterfeiter puts on the market are bigger. The situation is similar for digital payments. As a financial group, we are doing everything we can to stay one step ahead of criminals through new cryptographic procedures, hardened systems and so on. It is not without reason that our experts are already working on cryptographic solutions that will be able to withstand the coming era of quantum computers. The challenge here is to maintain the convenience for the customers.

Jochen Werne: By its very nature, cash is without doubt the most robust payment method. This is regularly demonstrated in extreme scenarios such as disasters, failure of a digital infrastructure due to cyber attacks, natural disasters or technical failure. Cash is not tied to electricity, digital infrastructure, passwords or other technical features. In addition, the introduction of the second series of euro banknotes has enhanced security features and made banknotes more secure and more counterfeit-proof. As the Bundesbank reported at the beginning of the year, the number of counterfeit banknotes has fallen by a further five percent. With digital payment methods, consumers themselves have a responsibility to protect themselves. At the beginning of the Corona crisis, for example, the payment limit for contactless payments, such as in supermarkets, was increased. At first glance, this sounds harmless. But as a result, anyone can use a card – and it does not have to be their own – to pay for higher-priced goods without further security checks, such as by entering a PIN. And as far as data protection is concerned: with every cashless payment, consumers disclose personal information. Data that many companies use commercially.

Dr Harald Olschok: The risk of coming into contact with counterfeit money in Germany is still low. Most counterfeits are easy to detect. The security features of the current Euro series make it difficult for criminals. However, if digital payment methods are attacked, consumers should be aware that they lose much more than just their money.

China wants to take a step in this direction from 2021 onward at the state level as well. The aim is to link the Alipay payment solution with all private and state databases, including those in which cashless payment transactions are stored. The aim is to record and evaluate consumer behaviour. Subsequently, either rewards are offered or sanctions are threatened. Anyone who accumulates too much debt or fails to pay it back is no longer allowed to use express trains or planes in China. Although such a development is completely out of the question in European democracies in the foreseeable future, do you also expect consumer behaviour to play a much greater role in credit rating in the future?

Jochen Werne: Harvard history professor Niall Ferguson coined the term “new cold war” over a year ago. This “Cold War” is mainly about one technology leadership in artificial intelligence and takes place between the United States and China. Technologies are not good or bad, but how and for what purpose they are used by us humans, determines the outcome. Just because something is now technically possible, it does not necessarily make sense for a society. It is a great value of liberal democracies that these issues are discussed, that privacy is protected and that the state cannot act on its own authority.

On the question of creditworthiness, it can be said that the better a credit institution knows the borrower, the better a risk assessment can be made in order to quantify credit default risks. When assessing creditworthiness, the institution is required to use all relevant and available data for the decision. Today, it is technically possible to enrich the data provided by the future borrower with information about him/her from the Internet and social media and to round off the data with the help of AI algorithms and peer group comparisons. However, there is a high risk that private personal data may be processed here if inadvertently and the protection of privacy may be violated. This must be prevented. However, it remains to be seen how this will be dealt with in the future.

Leif Wienecke: First and foremost, it is a matter of making sensible use of the many possibilities of generated data to create added value. Companies such as banks primarily face the challenge of preparing their customers’ data in a meaningful way and integrating it for new applications. The ecosystems of the “GAFAs” or Alipay are “data first” companies which are integrated into the everyday life of their users. In principle, they only make decisions based on data and empirical findings. The above description from China, however, does not go hand in hand with our understanding of data or consumer protection, so we do not see this coming either.

On the other hand, it is of course essential to pursue data-driven innovation. Even the credit rating system that exists today can certainly be extended via relevant, contextual data points, in the interests of consumers and credit institutions. The topic of “social scoring”, i.e. the use of customer data from social networks, is controversial in Germany and is discussed above all in the context of consumer protection. This is correct, because the consumer should not only have to give his consent for such scoring, but should also be able to understand the algorithm and complain in case of discrimination.

Recently, initiatives have been heard repeatedly to make a CBDC (Central Bank Digital Currency) accessible to all citizens and not to limit an e-euro to institutional participants in the financial markets. What do you think about this?

Leif Wienecke: The CBDC issue is still in its infancy and has many facets. It is mostly about increasing the efficiency of payment transactions. End customers also benefit from this. In principle, innovation processes and initiatives to transform the financial industry are to be seen as positive. As with all topics with a European or international scope, it is important to create a uniform regulatory framework. Precisely because the introduction of a digital central bank currency for the public would not be accompanied by a change in the existing monetary system. At Solarisbank, we have been dealing with the block chain and crypto currency industry for over two years. Last year, we founded the subsidiary Solaris Digital Assets to realise our vision of the broad use of digital assets.

Ralf-Christoph Arnoldt: Unfortunately, very different things are mixed up here. Firstly, there is the technology on which most crypto currencies are based: the block chain. It is highly interesting because rights (to money, benefits from contracts, etc.) can be transferred securely and traceably. This technology has its use cases and will increase in importance. To issue a currency based on this digital solution is certainly forward-looking but not without risks. The speed with which sums of money can be transferred would in itself increase the speed at which money circulates to an extent at which we lack economic experience. Questions also remain to be answered about the security of the currency and who is responsible for the counter-value. It is therefore to be welcomed that we are dealing with this issue at an early stage so that we can learn with manageable and calculated risk.

The concept of the euro, on the other hand, suggests a digital currency as a means of payment. In my view, it is still too early for that. Not only because the overall economic effects can only be estimated to a limited extent at present, but also because this technology is geared to the security and distribution of data, not to transaction efficiency. The number of transactions is technically limited. There are concepts such as the Lightning technology to circumvent this and allow more transactions. However, the latter again functions as an intermediary according to principles similar to those of traditional payment transactions. Transactions are executed and then “booked” in the block chain – similar to a central bank transfer.

Likewise, too little attention is paid to the ecological aspect. According to estimates, Bitcoin alone consumed around 74 terawatt hours in one month at the end of 2019. By way of comparison, Germany’s total electricity consumption over the same period was around 47 terawatt hours.

And now the crucial question at the end: How do you make cashless payments?

Ralf-Christoph Arnoldt: With the Girocard – as far as possible contactless of course, and with pleasure also by mobile phone.

Leif Wienecke: I use Google Pay with my debit cards from our partners Tomorrow, Vivid Money and Bitwala. Offline I use the corresponding Visa cards. And online I also use PayPal.

Jochen Werne: Of course with cash and cashless.

Dr. Harald Olschok: In food retailing and gastronomy regularly with cash. For larger expenses, including refuelling, with credit cards.

Unlimited availability of our money and its ability to be used as a medium of exchange create certainty and lead to personal freedom. But which payment method is proving to be the most robust in any crisis? A reflection on the value of cash in a free society.

By Jochen Werne, Management Board member, Chief Development & Chief Visionary Officer (CDO/CVO) of Prosegur Cash Services Germany GmbH

In times when our life is being affected significantly by the effects of the situations like the COVID-19 pandemic, we become more aware of the basic needs in our lives. However, the COVID-19 crisis, which hits us globally so hard that we are even prepared to give up some of our civil rights and liberties guaranteed by the constitution, also reveals what certainty means and gives us and what we rely on in order to overcome a crisis and regain our freedom. We live in a world of exponential leaps in technology – and the technological progress has traditionally always resulted in a global improvement in living standards. The international community can be rightly proud of its achievement of reducing the percentage of people who have to live in absolute poverty from 35% to 8% in the last 30 years thanks to global trade. However, it is in times of crisis that we see just how sustainable the goals that have been achieved are. Here prudent and decisive action from political and business leaders is called for. Confidence gained in people and instruments is the greatest asset in times of uncertainty.

Cash: always available

The same applies for payments. While the independent good work over decades of many central banks such as the Deutsche Bundesbank, the European Central Bank and the US Federal Reserve is making itself noticeable in the crisis and the citizens rely on the stability of the euro and US dollar, cash is also showing itself to be an anchor of confidence in uncertain times. With growing concerns due to the coronavirus, in the USA for example the volume of physical cash in circulation has increased. In the week before 25 March this increased by 1.8% to 1.86 trillion dollars in absolute figures. This represents the biggest weekly increase since December 1999, when the fear of the so-called Millennium Bug was the reason for the rise. As we see today, the technological meltdown did not happen. However, 20 years later we are now more aware than ever of the vulnerability of technology and that in times of crisis the value of certainty is always the greatest asset. The increase in demand for cash, including in Germany, at the start of the corona crisis is probably attributable to this legitimate need of citizens for certainty and their great confidence in cash. According to the Bundesbank, the volume on Monday 16 March alone, the first day upon which schools and nurseries were closed, was 0.7 billion euros above the average.

Electronic payment methods, which are essential in so many areas such as online trading for example, repeatedly risk a loss of confidence due to technical failures. One of the most recent of these incidents occurred during of all times the Christmas shopping period on 23 December 2019, when EC card payments were no longer accepted at many terminals. It is a little like the situation described by the Roman poet Ovid: “People are slow to claim confidence in undertakings of magnitude.” Most certainly our savings – the fruit of our labour – are of this magnitude for us. It is for this reason that the availability of our money is so important. If this availability were restricted, we would start to feel that we might no longer be able to access our money, and a bank run would most likely be the result. It is not without reason that the “supply of cash” is expressly defined as a “critical service” in Section 7 of the Regulation on the Identification of Critical Infrastructures (BSI-Kritisverordnung – BSI-KritisV) of the Federal Office for Information Security (BSI). That is to say a “service to supply the general public […], the loss or impairment of which would result in significant supply shortages or risks to public security.”

Certainty in uncertain times

In the COVID-19 crisis, anxiety about health and the economic consequences of any crisis dominate our daily life. While fear is clearly caused by an external threat, anxiety is indeterminate. As the Greek stoic philosopher Epictetus wrote in his Enchiridion of stoic morals: “People are not disturbed by things, but by the view they take of them.” It was therefore also absolutely consistent that the World Health Organization (WHO), the European Central Bank, the Bundesbank and the Robert Koch Institute have been stressing repeatedly in the corona crisis that there is no documented case that would suggest there would be an increased virus risk due to the use of cash as opposed to card payment. They refer here to corresponding scientific studies and underline repeatedly that no information on such a risk has been documented.

Freedom established by the constitution

John Stuart Mill, one of the most successful liberal thinkers of the 19th century, defined freedom as the “first and strongest desire of human nature.” Accordingly, all governmental and social action must be directed towards granting the individual free development, while his freedom, as Mill formulates it in a principle known as the “principle of freedom,” may be limited under one condition: to protect himself or another person. Now, during a serious crisis, all citizens are forgoing some of their fundamental constitutional rights of freedom. This massive intervention is certainly consistent with Mills’ theory in this time of corona. In his novel The House of the Dead, Fyodor Mikhailovich Dostoevsky describes his own experiences of life in a Siberian prison camp and writes the subsequently oft-quoted sentence: “Money is coined liberty,” whereby he describes the vital relevance of a free exchange of goods in an environment where people are deprived of freedom – with cash in the form of coins. Although not in the same way as Dostoevsky, we are also living in a time of extreme change: on a social, economic and political level. We are living in a time when, due to exponential technological developments, whole industries and business models are changing radically and countries are competing for supremacy in areas such as Artificial Intelligence (AI). It is a time in which transformation is the new norm and an agile corporate culture has to be the key to success. It is currently the case in many traditional industries that “anything that can be digitised, will be digitised.” And inevitably this also raises the question of whether this is also the case for the first “instant payment” solution, one of the earliest and longest-lasting achievements of human civilisation – for our cash? Our current free choice of payment method is certainly good, as long as we can choose freely as consumers the payment method appropriate for the respective situation. Discussions about the possible restriction of the freedom of choice of citizens regularly prompt intellectuals to issue warnings. For example, the poet Hans Magnus Enzensberger is of the opinion regarding the issue of “restriction”: “Those who abolish cash, abolish freedom.” This opinion is also shared by Carl-Ludwig Thiele, a former member of the Executive Board of the Deutsche Bundesbank: “Abolishing cash would hurt consumer sovereignty — the free choice of citizens about their payment instruments […] Government agencies do not have the right to tell citizens how they should pay.“

Technological vulnerability, fall-back option and data protection

Particularly in extreme scenarios such as disasters, failures of a digital infrastructure due to cyber attacks, natural events or simply due to technical failure, it is made clear that cash, by its nature, is currently the most robust payment method. The fact that the contactless payment limit has been increased without further ado, for example in supermarkets, at first sounds harmless. However, as a result, anyone can pay for higher-priced goods using a card, and it does not have to be their own card, without any further security checks such as entering a PIN. Everyone has to examine and question critically for themselves the possible consequences of such a payment method. Also not to be disregarded is the issue of data protection. More cashless payments also mean more personal information disclosed by everyone. Data which numerous companies use for commercial purposes. At the latest since the introduction of the EU General Data Protection Regulation (EU GDPR), the sensitivity of the population of Europe with regard to data protection and privacy has been rising gradually. Klaus Müller, Germany’s top consumer protector and Executive Director of the Federation of German Consumer Organisations (vzbv), describes cash as “data protection in practice”. Anyone who pays with cash does not leave any traces to create a consumer profile, purchasing and payment behaviour cannot be manipulated. Cash also helps to protect financial privacy. This was emphasised by Udo Di Fabio, who was a judge of the Federal Constitutional Court for twelve years, at the Cash Symposium 2018 hosted by Deutsche Bundesbank. He explained that every citizen can dispose freely of their money. In his view this freedom would be restricted if financial management were completely digitised.

Smart cash management alleviates the workload of banks

Crises such as the current corona pandemic always bring to light new approaches and act as accelerators of transformation processes that have already been set in motion. With regard to cash-related industries, the banking world has already been in a transformation process for some time. A company such as Prosegur, which, with over 4,000 employees and 31 branches, is a market leader in Germany in the transportation of cash and valuables, is increasingly becoming a full payment-platform provider. Several banks have already taken the path of fully outsourcing their cash management for synergy and cost-saving reasons. Here, cash processes are becoming not only much leaner, but also more cost-effective. This is the case not only for banks, but also for retail customers. With smart machines installed by Prosegur at its customers, cash can be disposed of directly and credited to the customer account on the same day. The smart infrastructure, including dynamic monitoring and forecasting, optimises the logistics and reduces costs in cash logistics. This is the next step towards an efficient, digital and integrated cash management.

Coined Liberty 2.0 and the justification for and rightfulness of cash

In view of the technological progress and the associated social changes, it can be seen that key values from the human perspective are still valid. Based on an intellectual, serious discussion, the relevance to today of the theories of for example Dostoevsky with his experiences in an unfree society is clear: The discussion about the civil rights and liberties of citizens is always very closely related to their ability to use cash freely, to their freedom of choice of payment method and ultimately to the rightfulness of their actions with regards also to effiency and impact. Our open and liberal society is characterised by the fact that we are discussing and most certainly will continue to discuss “Coined Liberty 2.0” at this level.

It has been a great pleasure giving the keynote at the CashCon2020 together with Mirko Siepmann, member of the board at Bankhaus August Lenz and long term business partner of Prosegur Germany.

We reflected with the expert auditorium, topics as Cash versus Crypto, The rise and fall of cash through the ages; Why we Germans, of all people, stick so closely to cash and if ATMs – will soon be a thing of the past or will they withstand digital disruption?