A plea for trust in a time of mistrust. Trust is the foundation on which monetary systems are built. Trust forms the basis of international diplomatic relations and is the foundation for all progress.

But what happens once trust is shaken?

The diplomatic dispute over a multibillion-dollar submarine treaty – which took place three months before the Russian – Ukrainian war, concerns about a new cold war, and the collapse of the Bretton Woods system exactly 50 years ago are the manuscript for this maritime-themed French-American story about money and trust. It is an object lesson for our times, where we are witnessing the emergence of crypto-financial markets and thus stand on the threshold of a new form of money.

TIME OF MISTRUST

by Jochen Werne

After the traditional long summer vacation, France awakens in September from its brief self-created slumber, as it does every year. Life begins to take its usual course, even if some are still reminiscing, perhaps enjoying the first harbingers of post-Covid worry-free life. Not so Philippe Étienne. For him, on the other side of the Atlantic, in Washington, which is actually picturesque at this time of year, autumn begins with a diplomatic thunderstorm. A storm that must have been new even for the 65-year-old gray-haired eloquent ambassador of France. 6160 kilometers away, at the Élysée Palace, Président de la République Emmanuel Macron decides to call his top diplomat in the United States, along with his Australian counterpart Jean-Pierre Thebault, to Paris for consultations. The unprecedented act in Franco-American history is justified by Foreign Minister Jean-Yves Le Drian with the “exceptional gravity” of an Australian-British-American announcement, and impressively underlined with the words “lie,” “duplicity,” “disrespect” and “serious crisis.”

At the heart of this crisis is the surprise announcement by the aforementioned countries to enter into a strategic trilateral security alliance (AUKUS) with immediate effect. An alliance that also provides for the procurement of nuclear-powered submarines for Australia, effectively putting to rest a 56-billion-euro French-Australian submarine order already initiated in 2016. The conclusion of the agreement comes at a time when U.S. President Joe Biden has asserted to the UN General Assembly, “We do not seek – I repeat, we do not seek – a new cold war or a world divided into rigid blocs.” However, experts, such as renowned historian Niall Ferguson, have been talking about this so-called “new cold war” between the U.S. and China since 2019, and it is not about nuclear arms races, but rather about technology supremacy in cyber security, artificial intelligence and quantum computing. Even though nuclear-powered submarines are at the center of the diplomatic dispute, one is quick to note in the AUKUS agreement that cooperation in the aforementioned fields is one of the most important components of the treaty. An objective that is perhaps also congruent with French interests. But the dispute between the old friends is less about the “what” than about the diplomatic “how” – that is, about the breach of trust that is triggered when close allies are simply presented with a fait accompli. Facts that also affect them financially and personally.

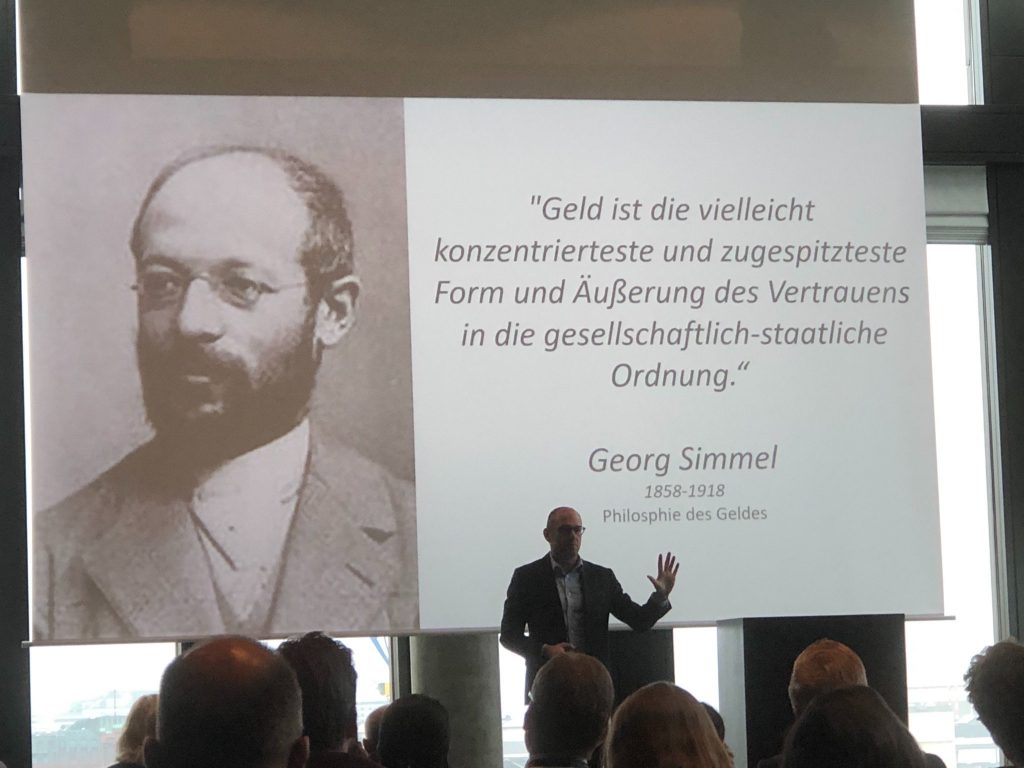

Because money and trust are closely interwoven. The trust of a bank that the creditor will repay its debts. A citizen’s trust that the currency in which he or she is paid their salaries is stable. A state’s trust in a currency system that the agreements made there will be honored by all. Georg Simmel, in his “Philosophy of Money,” sums it up this way: “Money is perhaps the most concentrated and pointed form and expression of trust in the social-state order.”

Last year marked the 50th anniversary of another French-American trust-busting melodrama with a maritime backdrop. Benn Steil, senior fellow at the Council on Foreign Relations, describes the moving events of August 6, 1971, in his book, The Battle of Bretton Woods, as follows: “…a congressional subcommittee issued a report entitled ‘Action Now to Strengthen the U.S. Dollar` that concluded, paradoxically, that the dollar needed to be weakened. Dollar dumping accelerated and France sent a warship to pick up French gold from the vaults of the New York Fed.”

At first glance, this dramatic gesture by then French President Georges Pompidou in the final act of the collapse of the Bretton Woods system seems as strange as the withdrawal of ambassadors today. The basis, however, is similar and lay then as now in an equally shaken trust between the great nations that were nevertheless so closely intertwined. Without going deeper into the new monetary order created after World War II, with the U.S. dollar as the anchor currency, it is important to understand the reason for the French revolt evident in the “White Plan.” The plan provided that the U.S. guaranteed the Bretton Woods participating countries the right to buy and sell gold indefinitely at the fixed rate of $35 per ounce. The dilemma of this arrangement became apparent early on. For by the end of the 1950s, dollar holdings at foreign central banks already exceeded U.S. gold reserves. When French President Charles de Gaulle asked the U.S. to exchange French dollar reserves for gold in 1966, the FED’s gold reserves were only enough for about half that amount. The ever more deeply anchored loss of confidence forced the American president Richard Nixon on August 15, 1971 to cancel the nominal gold peg and the so-called “Nixon shock” ended the system as it was.

And where something ends something new can or will inevitably begin.

Today we live in a world where the stability of our currency is based on our confidence in government fiscal policy, the economic strength of our country, and the good work of an independent central bank. However, we also live in a time when new currency systems are already looming on the dense horizon. The basis for this was laid in 2008, not surprisingly, by one of the most serious crises of confidence in the international banking system that modern times have seen. And the new systems are being implemented with the help of cutting-edge distributed ledger blockchain technology. The new, with its decentralized nature, is challenging the old. While many of the new currencies in the crypto world, such as bitcoin, are subject to large fluctuations, stablecoins promise a link and fixed exchangeability to an existing value, such as the US dollar or even gold. However, the old Bretton Woods challenge of being able to keep this promise at all times remains in the new world. Millions of dollars in penalties imposed by the New York Attorney General’s Office on the largest U.S. dollar stablecoin, Tether, for not being fully verifiable do little to help trust, especially when less than 3 percent of the market capitalization is actually deposited in U.S. dollar cash. As always with new ones, trust has to be built up. This can be done privately, perhaps with a stablecoin backed 100% by central bank money, or by the state, with well thought-out central bank digital currencies, such as the digital euro planned by the European Central Bank.

We live in a world of perpetual rapid change and trust is, as Osterloh describes it, “the will to be vulnerable.” Without trust, there are no alliances, no togetherness, no progress.

Philippe Étienne was back in autumnal Washington after just a few days and has since been working again on what diplomats are best trained for – building trust.

Sources

Billon-Gallan, A., Kundnani, H. (2021): The UK must cooperate with France in the Indo-Pacific. A Chatham House expert comment. https://www.chathamhouse.org/2021/09/uk-must-cooperate-france-indo-pacific (Retrieved 24.9.2021)

Brien, J. (2021): “Stablecoin without stability”: Tether and Bitfinex pay $18.5 million fine. URL: https://t3n.de/news/stablecoin-tether-bitfinex-strafe-1358197/?utm_source=rss&utm_medium=feed&utm_campaign=news (Retrieved: 9/30/2021).

Corbet, S. (2021): France recalls ambassadors to U.S., Australia over submarine deal. URL: https://www.pressherald.com/2021/09/17/france-recalls-ambassadors-to-u-s-australia-over-submarine-deal/ (Retrieved 9/25/2021).

Ferguson N. (2019): The New Cold War? It’s With China. And It Has Already Begun. URL: https://www.nytimes.com/2019/12/02/opinion/china-cold-war.html (Retrieved: 9/30/2021).

Graetz, M., Briffault, O. (2016): A “Barbarous Relic”: The French, Gold , and the Demise of Bretton Woods. URL: https://scholarship.law.columbia.edu/cgi/viewcontent.cgi?article=3545&context=faculty_scholarship p. 17 (Retrieved 9/25/2021).

Osterloh, M., Weibel, A. (2006): Investing trust. Processes of trust development in organizations, Gabler: Wiesbaden.

Steil, B. (2020): The Battle of Bretton Woods: John Maynard Keynes, Harry Dexter White, and the new world, p. 377.

Stolze, D. (1966): Does de Gaulle defeat the dollar? In ZEIT No. 36/1966. URL: (https://www.zeit.de/1966/36/besiegt-de-gaulle-den-dollar/komplettansicht (Retrieved: 9/26/2021)

The Guardian Editorial (2021): The Guardian view on Biden’s UN speech: cooperation not competition URL: https://www.theguardian.com/commentisfree/2021/sep/22/the-guardian-view-on-bidens-un-speech-cooperation-not-competition(Retrieved: 9/29/2021)

Unal, B., Brown, K., Lewis, P., Jie, Y. (2021): Is the AUKUS alliance meaningful or merely a provocation – A Chatham House expert comment. URL: https://www.chathamhouse.org/2021/09/aukus-alliance-meaningful-or-merely-provocation (Retrieved: 9/24/2021).

Time Online (2021): France sees relationship in NATO strained. URL: https://www.zeit.de/politik/ausland/2021-09/u-boot-deal-frankreich-australien-usa-streit-nato-jean-yves-le-drian?utm_referrer=https%3A%2F%2Fmeine.zeit.de%2F (Retrieved: 9/25/2021)