Cyber crime has become a serious threat to business, politics and private individuals since a long time. New technologies based on the use of artificial intelligence might offer more security.

The fight against cyber threats has become significantly more complex for global government organisations, businesses, and individuals in recent years. Technical protection of IT systems and infrastructures and thus data security in the narrower sense are no longer the only issues. Companies, for example, need to address the much broader concept of information security.

Solutions based on artificial intelligence could prove helpful in the fight against cybercrime. According to a study by the IBM Institute for Business Value, the spread of intelligent, AI-based security solutions will increase significantly in the coming years.

Technical protective measures have long since been based on machine learning, for example, to identify spam or phishing e-mails or to record trends and anomalies in large amounts of data – both in data traffic within the corporate network and in its external connections.

Jochen Werne

AI systems for the identification of cyber attacks

In future, for example, systems might also be able to identify hidden channels in the corporate network through which cyber criminals attempt to acquire data. AI’s greatest strength, pattern recognition, enables automated detection of a wide range of anomalies and security incidents. For this purpose, however, AI-based systems must also learn to distinguish between common IT failures and cyber attacks. In addition, self-learning algorithms need to take internal corporate processes into account to come up with precise results.

In the near future, according to a forecast by Christian Nern, former Head of Security Software DACH at IBM Germany and today Partner at the Consulting firm KPMG, AI-based security analysis systems will be able to detect and fend off attacks proactively. Then, according to the former IBM security software chief, the confrontation between cyber criminals and security officers could possibly take place directly between the AI systems they use.

Germany as a pioneer country

Germany, which considers itself a pioneer country in the fields of learning systems and artificial intelligence, has already launched a platform for artificial intelligence on this topic initiated by the Federal Ministry of Education and Research (BMBF): “Learning Systems”. The platform with its 200 members brings together leading experts from science, business and society and deals with technological, economic and social issues relating to the development and introduction of learning systems on an interdisciplinary and cross-sector basis.

As often in cyber security topics, there is no patent solution for the numerous questions and challenges. A company-wide risk management system, which establishes appropriate technical and organisational measures and also takes into account findings from psychology and cultural studies, seems to be a sensible way forward.

The right balance between security awareness and security, individual freedom paired with increased personal responsibility as well as support through technology and organisational structure is probably the most promising approach in the current state of research and technology to effectively meet the challenges for information and IT security.

Artificial intelligence is finding its way into the highly regulated world of banking. And not only GAFA Silicon Valley high-tech companies see it as the technology of the future, but also FinTechs and established banks. How it came to this, what possibilities and limits there are at the moment and why humans will remain irreplaceable not only when it comes to money – the commentary

by Jochen Werne, innovation and transformation expert Munich private bank Bankhaus August Lenz

Original published in German in the IT-Finanzmagazin (31 July 2018). Translation by DeepL

After “FinTech”, “Blockchain” and “Crypto”, “AI” is the new buzzword in the banking world. Whether chatbots in the digital customer center or self-learning algorithms for highly complex investment strategies are being discussed – the omnipresence of the term suggests that the integration of artificial intelligence into one’s own business model seems to be virtually vital.

Artificial intelligence and big data are currently the strongest and most vibrant innovation trends in the financial sector …

… was also one of the guiding principles of Prof. Joachim Wuermeling, board member of the Deutsche Bundesbank, in his speech on “Artificial Intelligence” at the second annual FinTech and Digital Innovation Conference in February 2018 in Brussels.

The choice of the conference venue, which like rarely any other city combines both a belief in progress and a deeply rooted European tradition, can hardly be more symbolic of the forthcoming change. In fact, the topic is by no means new: the development towards an increased use of so-called non-human intelligence is based on approaches from the 1940s – with the invention of the first computers

Artificial intelligence: revolution as a reaction to mountains of data?

But what is now possible in times of exponential technologies is in fact nothing less than a revolution. The financial industry is sitting on a valuable mountain of data, the extent of which is currently difficult to estimate. The maturing AI systems would not only make the preparation and processing of this data easier, but also much more cost-effective, faster and more targeted. Data already collected could become the most valuable raw material and a resource due to the technological leaps in the field of AI, which, in combination with the enrichment of external, non-structured data, must be “usable” in a meaningful way.

The industry is asked to use private data in a sensitive way for the benefit of the customer, – a goal that should certainly apply to all AI-based approaches.

To find meaningful regulations for the handling and the effects of the use of AI on society, economy and thus on our life and the work of tomorrow is the task of politics. The fact that this topic is taken very seriously is evident not only in national initiatives such as the German Platform for Artificial Intelligence “Learning Systems”, but also in the European Artifical Intelligence shoulder-to-shoulder approach, which is being pushed forward by France and Germany.

“Digital hand holding” in the event of a financial crash is not enough

At present, it is still too early to say which operational areas of the financial world will sooner or later be supported – in part or even entirely – by the use of AI systems. However, the financial crises of the past have shown this time and again:

Trust is crucial when it comes to money. Trust in the markets, the banking system and the human contact as an intermediary in a complex issue”.

However, the banking industry knows very well from its own experience how easy it is to loose customer’s trust. An experience that Mark Zuckerberg and Facebook recently also had to make in connection with the Cambridge-Analytica scandal. As with every new technology and every new approach, the same applies to the topic of “intelligent” systems: a lot of trust, coupled with half-knowledge and a big dash of emotionality results in a popular trend cocktail, which, however, bears a certain risk of headaches on the following day.

Jochen Werne

Jochen Werne is the authorized signatory responsible for Marketing, Business Development, Product Management, Treasury and Payment Services at Bankhaus August Lenz & Co. After two years as navigator of the sailing training ship ‘Gorch Fock’, the international marketing and banking specialist completed his studies as client coverage analyst at Bankers Trust Alex. Brown International and in Global Investment Banking at Deutsche Bank AG, he has worked on numerous projects in other European and American countries. In 2001, he joined Accenture as a Customer Relationship Management Expert in the Financial Services Division before joining Bankhaus August Lenz & Co. AG in Munich, where he has since been responsible for various areas of the institute. As part of the Innovation Leadership Team of the Mediolanum Banking Group, a member of the expert council of Management Circle and the IBM Banking Innovation Council, Jochen Werne is a keynote speaker at numerous banking and innovation conferences.

Bankhaus August Lenz im Gespräch: mit Jochen Werne, Direktor, Mitglied der BMBF Blattform für Künstliche Intelligenz „Lernende Systeme“ & des Royal Institutes of International Affairs Chatham House

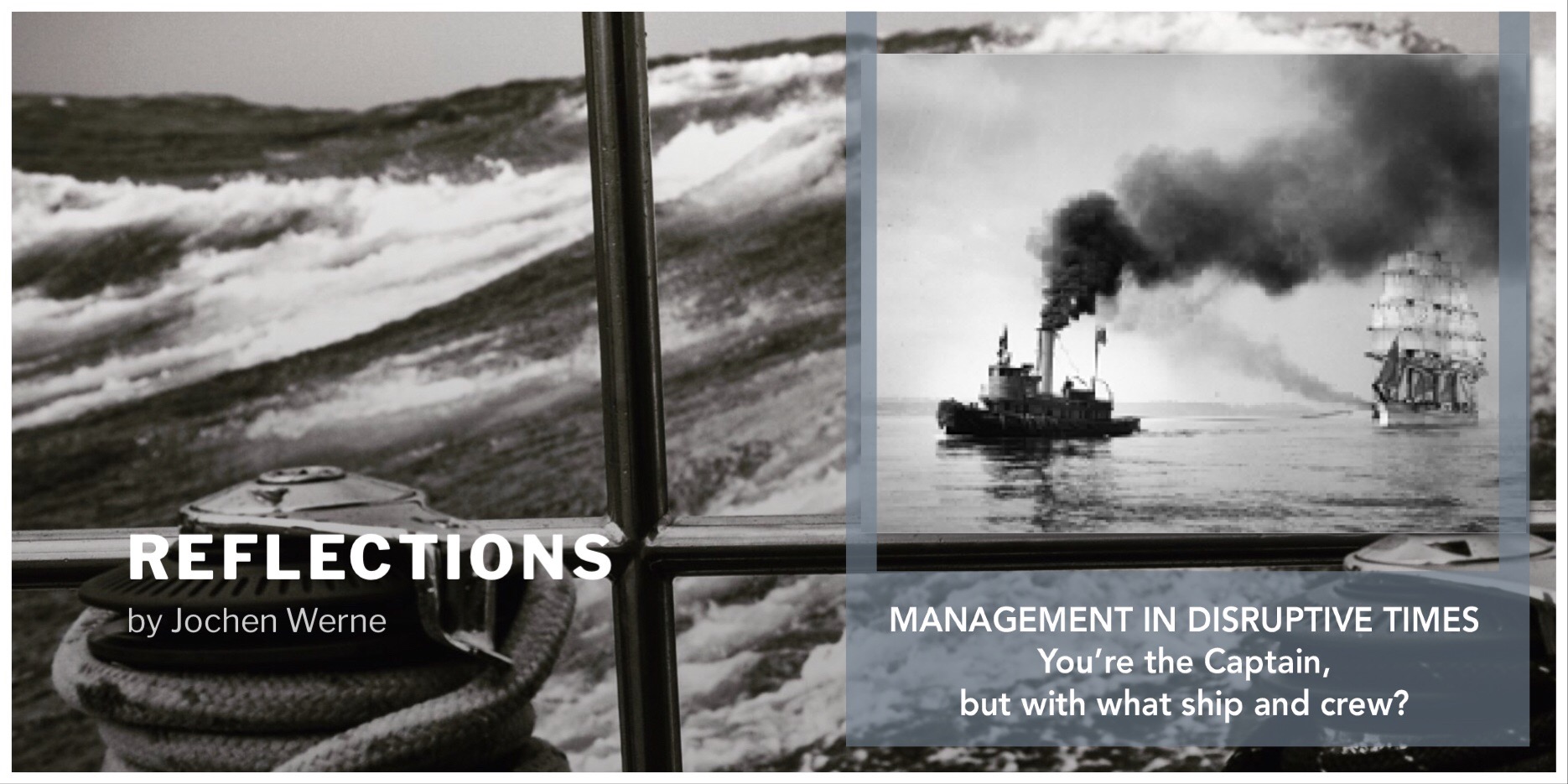

“An analogy for business leaders in the financial industry that compares the challenging times of today’s technological enterprise transformation with the changes during the time of the industrial revolution when steam ships ended the centuries-long era of sailing ships.”

In 1971, the BBC began broadcasting a series on the history of James Onedin, who, as captain and later as shipowner, lived through the stormy times of industrialisation and the conversion of the entire industry from sailing to steam navigation. The series, which takes place in Victorian England in the second half of the 19th century, describes in a special way the subtleties of the interplay of a changing market. New technologies, new skills of market participants, increased conflict potential between entrepreneurs and managers and reorientation in an environment of shrinking margins – special challenges for those who tried to continue their business as before: with sailing ships.

The documentation shows impressively how highly hierarchical organisations like the Royal Navy react and often struggle in times of major technological changes

The captain is responsible for bringing his ship, crew and cargo safely and within a specified time and financial framework to the port of destination. But what if the ship is no longer able to do this and the competition suddenly moves across the blue oceans with completely different ships? What if the shipowner does not have the capacity to trust the new technologies or simply does not have the financial resources to re-equip his fleet? And what about the crew? Does the crew has the necessary skills to sail on the new ships?

Many captains of banks and financial institutions seem to have this scenario all too present. E.g. due to declining customer traffic in bank branches, the high costs for a broad branch network are hardly to be paid today. Germany as a financial centre is “overbanked”, interest rates in the basement – the conditions in Germany for successful banking have never been as challenging as they are now. To this end, customers are continuing to drive change in the industry with their changing demands on digital tools.

Outwaiting a problem or tackling it

The complexity of economic changes has been enormous in every epoch, the difference to current upheavals lies in the temporal component. If companies do not react immediate to market changes today, they might loose their customers faster than ever before. In such disruptive times, all those involved want an “efficient” change process. The only problem is that the term “change” is so omnipresent that it is often perceived as stress and overload. As a result, many levels of management fall into one of the following situations: either they try to sit out the situation and leave change to their successors, or they push many, often less effective measures in an attack of blind actionism. Active, thoughtful and vital change management is often neglected.

More entrepreneurial thinking

Processes of change require both superiors and employees. If the existing situation cannot be improved or adapted at any vertical level, it must be questioned. Concluding, this means for all those involved that situations must always be reflected and corrective measures initiated at an early stage.

Understanding the corporate culture is vital for a successful transformation

In many companies, however, this need for action, which has a high potential for conflict, is often insufficiently communicated. In some places there is a lack of interest for employee issues, a lack of error and conflict culture and a minimal willingness to change. If banks neglect these issues, change processes threaten to fail on a broad basis. This means that managers in a disruptive environment have a natural need for action. The implementation of new strategies, systems and structures and early adaptation to changing market situations are vital factors for survival. A well-known quote by former US President Wodrow Wilson (1913-1921) is particularly valid for today’s highly competitive financial sector: “If you want to make enemies, try to change something.”

Those companies that create the change will share the large financial services market with the new market players and use instruments that did not exist in the classic banking of the past.

Just like James Onedin, who for the longest time was an advocate of classic sailing ships, finally added a modern steamship to his fleet. And to facilitate the change for himself personally, he named the ship after someone he loved.

The number of cyber attacks on businesses, governments and individuals is increasing worldwide. The human being in his cultural environment is an important element. Different cultures seem to be associated with different susceptibilities.

In its annual management report “The Situation of IT Security in Germany 2018”, the Federal Office for Information Security records a threatening scenario: The number of cyber attacks on the federal government, German industry and private individuals is increasing at an alarming rate. Germany, in particular, is being massively targeted by criminal hackers.

One thing is certain: almost 90 percent of all cyber attacks have a criminal background. Approximately ten percent of all cyber attacks are caused by state cyber warriors. The goal of criminals is either personal data (account connections, credit card numbers, passwords, etc.) or capturing the computer for new attacks via bot network or to extort ransom money for the renewed release of the computer. The ransomware “Wannacry” is an equally prominent and frightening example of this. If state systems become the target of hackers, this usually results in sabotage, espionage and the spying out of trade secrets. The BSI discovered 800 million malicious programs for computer systems last year. In the previous year, the figure was 600 million – around 400,000 malware variants are added daily.

Cyber Security and the Human-Cultural Factor

The view must be directed to an important dimension of the human factor: The influence of different cultures on the handling of technology and in particular on the behaviour of individuals in the context of cyber security. Cultural peculiarities influence preferences, prejudices and behaviours. In his renowned book “The Culture Code”, anthropologist and marketing expert Dr. Clotaire Rapaille explores how members of different nationalities have developed very different codes for the image of products, companies or countries.

These findings come from client assignments in which Dr Rapaille conducted extensive interviews with focus groups to identify cultural preferences, prejudices, idiosyncrasies and behaviors. In more in-depth analyses, a piece of generalized psycho-cultural characteristics is then derived from representatives of the countries studied.

Country-specific aspects of cybercrime

Questions arise as to what protective concepts and guidelines might look like that take this background into account appropriately? And what role do cultural and country-specific aspects play here, such as the famous “German Angst” and corporate cultural aspects, such as the comparison of a classical hierarchical system versus Holacracy models, which have become increasingly en vogue in times of digital transformation?

Some concise examples from the findings of Dr. Rapaille: Americans define themselves strongly through their work. In this culture, professional activity largely determines the image of one’s own identity. The importance of money in this culture is proof of diligence and success.

The author sees completely different meanings in European countries. In France, for example, work and money are regarded more as “necessary means to an end” – those who can afford it expect at least a certain amount of entertainment and comfort from their job there. According to Dr. Rapaille, quality and technical perfection play an important and in some cases even absolute role in Germany or Japan, while US-Americans, according to his analyses, in many cases content themselves with “It just works” and are even sceptical about excessive perfection.

The author recognizes the Germans’ tendency towards perfectionism, which is partly exaggerated from a foreign point of view, as decisive for the quality of “German Engineering” and the global economic success of the Germans in this field. Dr. Rapaille is convinced that US culture, on the other hand, is characterized by a widespread refusal to grow up, which in turn leads to a great competitive advantage in the field of innovation.

Conclusions for more cyber security

This raises the question what are the appropriate protection concepts in an increasingly complex threat situation. A classic approach is the definition and enforcement of policies, both on a technical and organizational level, which are intended to guarantee compliance with security measures. The more hierarchically and authoritatively a corporate culture is aligned, the more restrictive the corresponding guidelines usually become.

However, the approach of establishing security primarily through bans and restrictions on user freedoms has proven to be double-edged in practice. The more the possibilities of an individual user are restricted, the more this encourages the tendency to escape the corset of safety-related rules.

A typical consequence is the “Bring Your Own Device” (BYOD) problem with which many company IT departments have been confronted for years – if the functions and authorizations of their work equipment are too limited, users bring private end devices with them to the workplace. These are then often not integrated at all into the protection and security concepts of the company. If the BYOD escape route is also suppressed, such measures often result in a refusal attitude à la “The desired is not possible with the means available – if the IT department wants it that way, then this task cannot be solved”.

Flat hierarchies and personal responsibility as a solution?

Is the better way, then, in holacracy models, in flat hierarchies, or in “loose reins” in terms of security and a strengthening of employees’ personal responsibility?

For the reasons derived in the preceding sections, this approach is by no means a guarantee for higher IT and information security. A healthy middle course could lie in adequate risk management. Technical and organisational security measures take into account the hazard level of specific data and applications. Sensitive areas and particularly sensitive data are subject to more stringent security measures, business areas or processes with less sensitivity are also protected, but assign employees a higher degree of personal responsibility. All protective measures take into account the above-mentioned psychological and cultural-historical findings.

Almost every day, experts in the media try to create a historical analogy for us in order to explain the dynamics and speed with which changes are taking place today at all levels of our lives – from private consumption and our working world to international politics. Often analogies are drawn to different decades of the 20th century. The prominent British historian and Harvard professor Niall Ferguson contradicts these comparisons and sees an analogy rather in the effects that the invention of the printing press in the 15th century had on our lives and on our society. Only that today the changes due to exponential technologies and the Internet take place much faster.

For us as the HUMAN Factor, these comparisons are incredibly important. In times of uncertainty, they help us to better assess the changes and thus at least maintain a certain reassuring feeling of security and explainability. However, if we do not succeed in setting the right filters in times of social media and “information overload”, we run the risk that this feeling of understanding does not materialize and that we all too easily become victims of supposedly simple explanations and “fake news”. Ferguson uses a striking example to illustrate that this is not a new phenomenon and that serious technological changes have also brought major and often turbulent changes to society. In times of the invention of book printing, knowledge was spread more cheaply and a broad part of the population gained access to higher education. One of the first books to be printed in large numbers was the Bible. But also other writings, like “Malleus Maleficarum” or in English the “Hammer of Witches” became famous. The “Fake News” book served to justify the persecution of witches, appeared in 29 editions and has been second place on the book bestseller list for 200 years.

At the latest since the end of the 1990s, since the mass “democratization” of the Internet, our lives have been shaped by the exponential progress of modern technologies. The associated digitalization – the DIGITAL Factor – is not only a technical and economic challenge, but also a societal one. However, the enlightened man began, not to accept everything that a “Beautiful New World”, sometimes reminiscent of Aldous Huxley’s novel, promises. This is shown by citizen projects such as the so-called “Charter of Digital Fundamental Rights” of the European Union.

The word “exponential” automatically hides the logical conclusion that change will take place even faster in the future. These changes affect almost every industry and what is seen today as a billion-dollar future market can quickly become a basic business with significantly lower costs and thus significantly lower profit margins tomorrow. The camera chip of our smartphones costs today only about two to three Euros, a Spotify subscription, and thus the access to an incredible amount of music, only a few Euros a month.

The conclusion for companies in the 21st century is simple: Those who do not understand these exponential dynamics of technical development or do not take them sufficiently into account in their business model can quickly lose touch – not only with customers but also with potential business partners. But why is it so difficult for us to correctly assess the development potential of the technologies? The answer: People think linearly. This is why technologies are usually overestimated at the beginning of their development, but tend to be underestimated in the long run. This was first described in 1965 by the Intel engineer Gordon Moore – later known as Moore´s Law, one of the essential theoretical foundations of the “digital revolution”. In times of exponential technologies, our society risks a split between the group of people with an affinity for digital and digital natives and a group of people who have growing difficulties with the speed of change of our time. The latter have not learnt to keep pace with fast-moving digital innovations due to their low affinity, age or lack of points of contact in everyday life.

Throughout history, new technological possibilities have always come with threatening concepts that have been published and discussed on all media channels available during this period. Today it is: “total transparency”, “transparent consumer”, “constant availability” or even job loss due to ongoing automation and artificial intelligence. At the social and state level, attempts are being made to counteract such fears, to increase competitiveness and to involve the population in the process of change. Two of the many good examples referring to Germany are the strategy on artificial intelligence put in place by the Federal Government and the Platform for Learning Systems initiated by the Federal Ministry of Education and Research.

It is important never to forget, that every change – even if the trigger is a rapidly developing technology – requires a certain time horizon to be implemented and to create broad acceptance. Here the “CULTURE Factor” often comes into play. One example is cash. While the Scandinavian countries, above all Sweden, are about to digitalize their payment systems to a large extent, in Germany currently about 80 percent of all transactions are carried out with cash.

In every business model, global trends need to be identified, changes need to be driven, and local conditions need to be taken into account in order to be successful in this market. The same formula applies to societal change. Especially when it comes to creating an agenda for the use of new technologies for the benefit of our society.

Fast täglich wird von Experten in den Medien versucht für uns eine geschichtliche Analogie herzustellen, um die Dynamik und Geschwindigkeit zu erklären, mit der sich heute Veränderungen auf allen Ebenen unseres Lebens – vom privaten Konsum, unserer Arbeitswelt bis hin zu internationaler Politik – vollziehen. Oftmals werden hierfür Vergleiche zu den 1930ern oder 70ern gezogen. Der bekannte britische Historiker und Harvard Professor Niall Ferguson widerspricht diesen Vergleichen und sieht eine Analogie vielmehr in den Effekten, die die Erfindung der Druckerpresse im 15. Jahrhundert auf unser Leben und auf unsere Gesellschaft hatte. Nur, dass sich heute die Veränderungen durch exponentielle Technologien und das Internet wesentlich schneller vollziehen. Für uns Menschen – also den HUMAN Factor – sind diese Vergleiche unglaublich wichtig. Sie helfen uns in Zeiten der Unsicherheit, die Veränderungen besser einschätzen zu können und somit zumindest ein gewisses beruhigendes Gefühl der Sicherheit und Erklärbarkeit zu erhalten. Wenn es uns jedoch nicht gelingt in Zeiten von Social Media und medialem „information overload“ die richtigen Filter zu setzen, laufen wir Gefahr, dass sich dieses Gefühl des Verständnisses nicht einstellt und wir allzu leicht Opfer vermeintlich einfacher Erklärungen und „Fake News“ werden. Dass dies kein neues Phänomen ist und gravierende technologische Veränderungen auch große und oftmals turbulente Veränderungen auf die Gesellschaft mit sich brachten, macht Ferguson an einem prägnanten Beispiel fest. In Zeiten der Erfindung des Buchdrucks kam es zu einer kostengünstigeren Verbreitung von Wissen und somit zur Möglichkeit, dass breite Bevölkerungsschichten Zugang zu höherer Bildung erlangten. Eines der ersten in großer Auflage gedruckten Werke war die Bibel. Doch erlangten auch andere Schriften, wie „Malleus Maleficarum“ oder zu deutsch der Hexenhammer Berühmtheit. Das eindeutige „Fake News Werk“ diente zur Rechtfertigung der Hexenverfolgung, erschien in 29 Auflagen und belegte für immerhin 200 Jahre den zweiten Platz der Bücherbestsellerliste.

Spätestens seit Ende der 90er Jahre, seit der massenhaften „Demokratisierung“ des Internets, ist unser aller Leben durch den exponentiellen Fortschritt moderner Technologien geprägt. Die damit einhergehende Digitalisierung – also der DIGITAL Factor – ist nicht nur eine technische und ökonomische Herausforderung, sondern vor allem auch eine gesellschaftliche. Dass der aufgeklärte Mensch jedoch beginnt, nicht alles einfach unreflektiert hinzunehmen, was eine an Aldous Huxley erinnernde „Schöne neue Welt“ zu versprechen scheint, zeigen Bürgerprojekte, wie die sogenannte „Charta der Digitalen Grundrechte“ der Europäischen Union.

Bereits im Wort „exponentiell“ verbirgt sich automatisch die logische Schlussfolgerung, dass sich Veränderungen in Zukunft noch schneller vollziehen werden. Diese Veränderungen betreffen nahezu jede Branche und was heute ein milliardenschwerer Zukunftsmarkt ist,kann morgen schnell zu einem Basisgeschäft mit deutlich geringeren Kosten und somit auch deutlich geringeren Gewinnmargen werden. Der Kamera-Chip unserer Smartphones kostet heute nur noch rund zwei bis drei Euro, ein Spotify-Abo, und somit der Zugriff auf eine unfassbar große Menge an Musik, nur wenige Euro im Monat.

Die Schlussfolgerung für Unternehmen im 21. Jahrhundert ist sichtlich einfach: Wer diese exponentiellen Dynamiken von technischer Entwicklung nicht versteht oder nicht ausreichend in seinem Geschäftsmodell berücksichtigt, kann schnell den Anschluss verlieren – Anschluss an Kunden aber auch an potenzielle Geschäftspartner.

Doch warum fällt es uns so schwer, das Entwicklungspotenzial der Technologien richtig einzuschätzen? Die Antwort: Menschen denken linear. Deswegen werden Technologien zu Beginn der Entwicklung meist überschätzt, langfristig aber tendenziell unterschätzt. Dies wurde 1965 durch den Intel Ingenieur Gordon Moore erstmals beschrieben – später bekannt als Moore´s Law, einer der wesentlichen Theoriegrundlagen der „digitalen Revolution“.

Unsere Gesellschaft lebt in Zeiten exponentieller Technologien natürlich auch mit der Gefahr einer Spaltung zwischen der Gruppe digital affiner Bevölkerungsschichten und Digital Natives sowie einer Gruppe von Menschen, die wachsende Schwierigkeiten mit der Veränderungsgeschwindigkeit unserer Zeit hat. Letztere haben aufgrund geringer Affinität, teilweise des Alters oder fehlender Berührungspunkte im Alltag nicht gelernt, mit den schnelllebigen digitalen Innovationen Schritt zu halten. Mit allen technischen Möglichkeiten geistern zudem Begrifflichkeiten durch die Medien, die vielen Sorgen bereiten und Ängste schüren: „Totale Transparenz“, „gläserner Konsument“, „ständige Verfügbarkeit“ oder gar Arbeitsplatzverlust aufgrund anhaltender Automatisierung und Artificial Intelligence. Auf gesellschaftlicher und staatlicher Ebene wird versucht solchen Ängsten entgegenzuwirken, Konkurrenzfähigkeit zu steigern und die eigene Bevölkerung in den Veränderungsprozess miteinzubeziehen. Zwei der vielen guten Beispiele in Deutschland hierfür sind, die von der Bundesregierung verabschiedete Strategie zu Künstlicher Intelligenz oder die vom BMBF initiierte Plattform für Lernende Systeme.

Es gilt bei jeder Veränderung – sei der Auslöser auch eine sich schnell entwickelnde Technologie – nie zu vergessen, dass es einem zeitlichen Horizont bedarf um Neues zu implementieren und eine breite Akzeptanz zu schaffen. Hier kommt der „CULTURE Factor“ oftmals ins Spiel. Ein Beispiel ist Bargeld. Während die skandinavischen Länder, allen voran Schweden, davor stehen ihre Bezahlsysteme weitgehend zu digitalisieren, werden in Deutschland aktuell noch rund 80 Prozent aller Transaktionen mit Bargeld durchgeführt. Es gilt also in jedem Geschäftsmodell globale Trends zu erkennen, Veränderungen zu treiben, jedoch auch lokale Gegebenheiten zu berücksichtigen, um in diesem Markt erfolgreich zu sein. Dieselbe Formel gilt für unsere gesellschaftlichen Veränderungen und das Ziel neue Technologien zum Guten für unsere Gesellschaft einsetzen zu können.

Author: Angelika Breinich-Schilly interviewed Jochen Werne, Director Marketing, Business Development, Treasury & Payment Services at Bankhaus August Lenz.

Banks need to do a lot to keep pace in an increasingly digital world. In an interview with Springer Professional, Jochen Werne from Bankhaus August Lenz talks about the challenges they have to face and the right strategies.

(c) Bankhaus August Lenz

Springer Professional: Mr. Werne, what do you see as the most important driver of change in banks that is being invoked everywhere? Is it just the ongoing digitalization or do you see other reasons that require a strategic change process of the institutes?

Jochen Werne: The industry is undergoing what is probably a historic upheaval. We live in times of exponential technologies and in addition to the cost-side necessity of digitizing a large part of the processes of the institutes, the rapid change in customer expectations associated with technology, poses great challenges to an industry which is not known for being greatly agile. This disruption will eclipse many things and later perhaps be judged as revolutionary as the invention of the steam engine. In recent weeks, this has hardly made anything as clear as the rise of the online payment processor Wirecard. Wirecard was not only able to outperform Commerzbank in the DAX in September. Founded in 1999, the company has already overtaken Deutsche Bank in terms of market capitalization. In addition to the ongoing digitalization, there are also other current challenges: The low interest rate phase, which has now already lasted for a long time, is putting massive pressure on the margins of traditional houses. Political crises, trade disputes, currency problems such as in Turkey and Brexit naturally also have a direct effect on the classic business models of banks: In the future, they will have to adapt more than ever and increasingly prove their agility. The exponential leaps in technology and ever shorter product cycles are forcing the global economy as a whole to change and adapt to changing circumstances more than ever before. Kodak is a good example. For the sake of simplification, the company has often been accused of not being far-sighted, but it has failed because of a culture that has allowed little change. Two letters are currently electrifying the economy: AI. After decades of disinterest, artificial intelligence is suddenly once again regarded as the decisive guarantor of a company’s future viability. The immediate integration of AI into one’s own business model seems indispensable, even vital for survival. Without smart software, you’d think you were dedicated to meaninglessness. Similar to Facebook, the financial industry holds very valuable data. The preparation and processing of this data will not only become easier with maturing AI systems, but also much faster, cheaper and more targeted. It is nevertheless private and sensitive data. In order to make this resource usable in conjunction with external data, the industry must at the same time ensure its long-term security. Data may only be used in the sense of the customer, the human being – an objective that certainly has to apply to all AI-based approaches. Artificial intelligence offers an enormous range of opportunities for companies to be closer to their customers. But it also has its limits and here we are not only talking about technical limits, but also about limits that arise when the customer’s mindset does not go hand in hand with what is technically possible. Technology will only prevail if people accept it. Too radical a step, without consideration for all three areas Human, Digital and Culture, is always counterproductive.

Springer Professional: You describe that many decision-makers in the banks are well aware of the necessary changes in the business model. At the same time, however, top management often does not seem to set a concrete course and have corresponding visions. Why do you think that is?

Jochen Werne:Digitization, technological advances and the acceleration of product cycles are forcing executives to reposition their businesses. The question is no longer whether and why companies should change and introduce a more flexible organizational form, but only: How quickly and sustainably can they do it? The need for successful Change Management is not new and digitization was not an unforeseeable event. What is new, however, is the sum of the technical innovations, the possibilities offered by the technological leaps and the resulting need for extremely high implementation speeds. This circumstance has far-reaching effects on the entire management of the company. This often leads to different change processes overlaying each other, individual change processes being interrupted, modified or restarted and the organization being in a state of continuous change. And this also applies to the manager.

Springer Professional: In order to become a driver of innovation as a bank, it is necessary to anticipate not only upcoming technological but also social changes, some of which still vary greatly from region to region. One example is the payment behaviour of customers, which looks different in Germany than in other European countries or even in Asia. Many financial service providers now have think tanks or innovation labs to take on this task. But does some good ideas go up in smoke due to poorly thought-out change management?

Jochen Werne:Every new innovative offering must be easy for the customer to understand, intuitive to use and as a bank, absolutely trustworthy in terms of data security. The customer relies on the security of the communication channels as well as the careful handling of his private data. The challenge is to ensure data protection while at the same time providing the highest possible level of customer convenience. The resources of traditional banks offer enormous advantages here. An established bank is perceived as a brand by its clients, who at best associate it with important values such as trustworthiness, competence, industry knowledge and personal service. This trust is enormously important to us and should definitely be used.

Springer Professional:Companies in other industries sometimes find it easier to cope with change processes because they are not subject to additional strict regulations, as is the case with banks. Nevertheless, financial service providers such as Wirecard have succeeded in clearly differentiating themselves from traditional banks with their business model. Recently, the share value of this Fintech has even overtaken Deutsche Bank, the industry leader, as the most valuable institution. What can the industry learn from this?

Jochen Werne:Laws and guidelines have a strong influence on the competitive situation. MIFID II and PSD II are prime examples of this. In the second case, industry experts predicted that the mere opening of the banking infrastructure to third parties would lead to a major shift in competition. This is a big advantage for FinTechs, but also the FinTech industry, which is already in the process of market consolidation, has to make considerable investments and adjustments, even if the new regulations now also open up new market opportunities. Non-adaptable service providers without sustainable and a viable business models will be driven out of the market, as will banks whose offerings do not meet the needs of customers in a digital world. The example shows not only the usefulness of cooperation, but also its necessity. The advantages of banks, such as routine handling of regulatory issues or cross-selling opportunities due to the existing customer base, will continue to exist even after the market consolidation of the FinTech industry and the introduction of new technological standards.

Springer Professional: In order to be a driver of innovation, a bank does not necessarily have to handle all tasks alone. Where and when do cooperations with Fintechs make sense from your point of view?

Jochen Werne: What some have, others lack. Banks have a solid customer base, greater financial resources and, most importantly, a banking licence and the necessary know-how to deal with the relevant regulatory authorities. In addition, traditional financial institutions with many years of market experience, expertise in customer business and their trust can score points. Fintechs, on the other hand, have business models that are geared precisely to bringing innovative, customer-centric digital tools to market in a short space of time. Strategic alliances make sense, because ultimately everyone benefits – especially the customers. Not only the young generation today has very high demands on innovative mobile banking, but all age groups have discovered the new mobile possibilities in a very short time. Personal access to customers, which has persisted despite all the financial crises to date, is a sign that banks have preserved their most important asset – the trust of their customers. In an increasingly transparent and open financial world, however, the extent to which the customer’s loyalty to his bank will remain, is open.

McKinsey Quarterly recently released an inspiring podcast entitled “Tapping into the business value of design” in which Simon London talks to McKinsey partners Benedict Sheppard and Hyo Yeon. It is very satisfying to see that the interview reflects many of the thoughts that led Bankhaus August Lenz & Co. AG, Mediolanum Banking Group to decide to launch a portrait card package to its German clients. This is the first time that a portrait cards have been launched for German private customers. The cards question the current design status of credit cards and offer not only a classic payment function, but also a 360° customer service experience combining digital, telephone and personal exchange options.

It has been a great experience challenging again the status quo, together with dedicated and highly experienced and motivated teams within the bank as well as with technology and card industry partners supporting the project.

Author Jochen Werne – Original in German at Bank-Blog – Translation by DeepL

Banks have to become guides for investors

Financial blogs, online communities & Co.: The ubiquitous flood of information can be both a curse and a blessing for bank customers and investors. Today more than ever, banks and savings banks must be “guides” for their customers.

Anyone who wants to invest money today gets a flood of information about the net. Dedicated private investors worldwide can be almost as well informed as professionals, in case of interest and sufficient know-how and time. Never before in the history of mankind have so many people worldwide had so much information at their disposal. Whether prices in real time, the latest assessments by analysts or experts, key figures on a security in an industry comparison, the diversity of opinion in a community – all this is available around the clock.

How intensively and purposefully this offer is used is another question. It can be assumed that only a minority is so urgently concerned with their investment or can be so concerned at all. In addition, the situation of the decision-maker is adversely affected by two factors: the excessive amount of unfiltered information and the classic behavioral finance problem.

Coping with the abundance of data and big data

Alvin Toffler, who brought the term “information overload” to prominence in his bestseller “Future Shock” in 1970, described the phenomenon and its consequences as follows:

“Information overload occurs when the input quantity of a system exceeds its processing capacity. Decision makers have a fairly limited cognitive processing capacity. Therefore, if information overload occurs, it is likely that a decrease in decision quality will occur.”

Consequently, it can be concluded that the wealth of information that accumulates every day can hardly be processed by a classic investor alone, let alone placed in the right context. In addition, there is an almost unmanageable and constantly growing mass of financial products for private customers. In short, a large proportion of investment decisions are therefore not made analytically correct, but spontaneously subjectively and emotionally, as the studies by Nobel Prize winners Kahneman and Tversky show.

Banks as a guide only for wealthy clients?

Clay Shirky, writer and consultant for Social and Economic Effects of Internet technologies and well-known in New Media circles, presented an interesting reflection on the problem of information overload:

„It’s not information overload. It’s filter failure.“

This provides a great opportunity for traditional banks to position themselves as problem solvers for the investor. The alternative – at least for wealthy private clients – apart from filtering their own information mass, is dialogue with a competent expert. A person they trust – and trust to not only filter out from the wealth of data what is relevant to their needs, but also to protect them from the classic emotional mistakes of financial decisions in volatile markets.

Development of a new, adequate support concept for all bank customers

All those who do not belong to this clientele, and this is mostly the classic retail customer, have little more than to accept the zero interest rate on their accounts and short-term securities. According to Bundesbank statistics, the majority of Germans have invested their assets in these forms of investment. This makes the Federal Republic a leading nation in financial matters when it comes to missed opportunities, as can be read again and again in the Sunday editions of the major national daily newspapers.

Today more than ever, the function of bank and financial advisors must be to act as filters and guides for customers in the jungle, providing them with a flood of information. Because no algorithm, no digital advisory service can protect the investor from an ill-considered, intuitive and possibly wrong decision. For modern bank management, this means setting up a completely different support concept with cost-efficient consulting structures, a powerful and highly flexible team and the appropriate digital and mobile equipment.